By The BCM Funding Group

With apologies to Admiral Farragut…

The S&P 500® Index’s 8.5% third-quarter acquire was a welcome response to the primary half of the yr’s histrionics. The quarter had its personal volatility because the markets flirted with a 10% correction, however then resolutely continued climbing the proverbial wall of fear. Finally, the traits that have been in place initially of the quarter continued and little modified:

- Fairness markets rose, led by the mega-cap U.S. know-how and client discretionary firms

- Small-cap, mid-cap and worth shares went up, however underperformed

- Worldwide markets largely went up, however underperformed

- Commodities typically went up, however underperformed

- Rates of interest stayed low… virtually in all places

- The U.S. greenback went up… er no, it really went down, breaking under its ten-year trendline

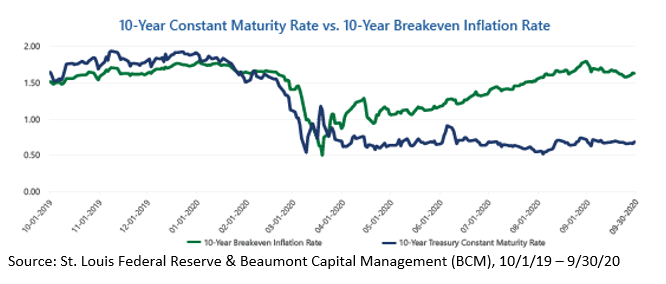

There have been necessary nuances. The Federal Reserve (Fed) prolonged its coverage of near-zero rates of interest at the least by 2023 and—maybe extra importantly—modified its inflation concentrating on coverage. Previously, the Fed’s coverage was a symmetrical 2% inflation goal the place the committee would work to nudge inflation up if it fell under 2% and stamp it out if it rose above 2%. This coverage was usually criticized as prematurely restrictive, choking off financial development earlier than massive swaths of society are in a position to profit. Beneath the brand new coverage, the Fed is now not pursuing a symmetrical strategy; as a substitute, it has moved its focus in direction of the long-term common price of inflation. The Fed will now enable inflation to rise reasonably above 2% for a while following intervals the place inflation has been persistently under its 2% goal. To translate, the Fed has dedicated to permitting the financial system to totally recuperate from the pandemic—after which some—earlier than tightening financial coverage.

[wce_code id=192]

In our opinion, that is excellent news! At the least in the intervening time, we don’t have to fret in regards to the Fed “getting in the way in which” of the restoration, nor will it impede any subsequent financial development. Main as much as this announcement, market inflation expectations had risen steadily for the reason that low in March with none corresponding rise in rates of interest. This mix has resulted in an extremely stimulative setting, with actual rates of interest at historic lows. Whereas this stimulus is a constructive for the financial system, contemplating the recession we discover ourselves in, it creates fairly a quandary for traders. First, if the market’s inflation expectation over the subsequent 10 years is approaching 2%, why aren’t charges rising? Second, in a world the place the risk-free actual rate of interest is sharply damaging and nominal charges are close to zero, how will traders meet their monetary objectives?

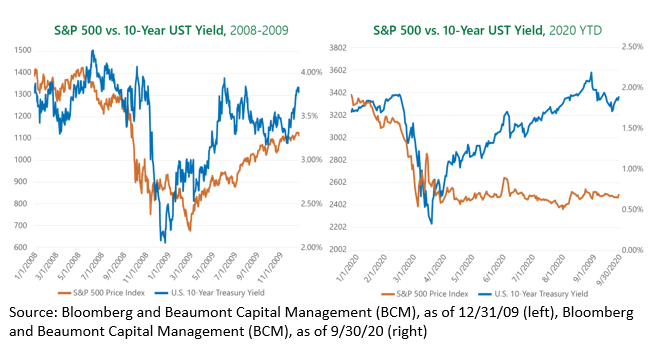

To offer some context for our first query, the dichotomy between nominal and actual rates of interest comes as one other distinction between this recession and previous recessions, most notably 2008. Sometimes, because the financial system turns the nook in direction of restoration, the market, inflation expectations, and rates of interest start to rise in lockstep—signaling “danger on” and a basic enhance in financial exercise. This has not been the case to this point because the Fed’s ~$three trillion of QE and different measures have saved rates of interest low. Nevertheless, at the moment traders seemingly maintain opposing views concurrently: the outlook for the financial system is constructive, however it is usually price paying a premium for risk-free securities.

Can this persist? In all probability not. Traders might consider that the outlook for the financial system has improved and that the Fed has sufficient instruments to maintain nominal rates of interest low for a time period. It’s additionally doable that traders aren’t anticipating a broad financial restoration and are as a substitute merely ascribing the next worth to the “winners” (i.e. large-cap tech) that comprise an ever-expanding proportion of the market indices. Solely time will inform, as we’re really in uncharted territory.

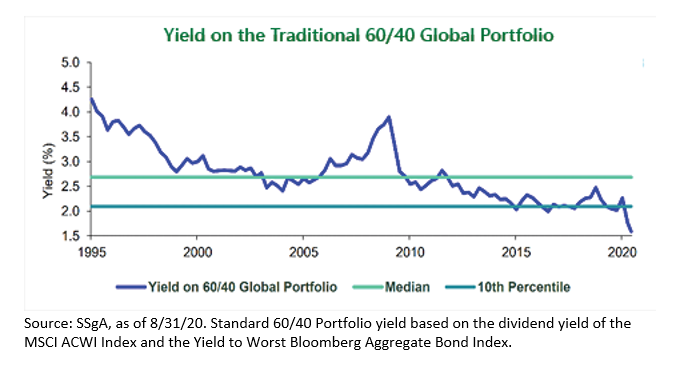

Regardless of the motive, traders must grapple with the results that low nominal and actual rates of interest can have on their portfolios. The ten-year U.S. Treasury’s yield-to-maturity—the presumed risk-free price of return—was 0.68% at quarter finish and the Bloomberg Barclays U.S. Mixture Bond Index’s (BBAB) was not significantly better with a yield-to-worst of 1.18%. With charges at or close to historic lows, large new provide of company and authorities debt, the Fed telegraphing the next inflation tolerance and company defaults surging because of the pandemic, we consider static bond allocations are poised to have a troublesome go within the months and years forward. Lengthy gone are the times when mounted earnings investments will comprise a sizeable element of a portfolio’s anticipated return. Lengthy gone are yields excessive sufficient to help the withdrawal assumptions in most monetary plans. Fastened earnings should still play the position of danger mitigation and supply shorter intervals of alternative, however historic 60/40 mannequin return expectations at the moment are solely achievable by accepting greater fairness or different funding danger.

Whereas “take extra danger” could also be a solution to assembly return expectations, we all know that it’s impractical for a lot of traders to take action given their danger tolerance and time horizons. Whereas not an all-encompassing resolution, we consider dynamic and tactical methods are extremely highly effective instruments for traders on this setting. The flexibility to mitigate danger in poor market environments is immensely invaluable, not just for the plain causes but in addition as a result of it could enable traders to take extra danger when in favorable market environments. Capitalizing on traits and alternative within the markets has all the time been an indicator of profitable investing, however the present market setting might necessitate it.

In closing, we’d be remiss to not acknowledge the 200,000+ American deaths and 1,000,000+ international deaths attributable to the pandemic. Our hearts and prayers exit to all those that have misplaced family members. Wanting forward, we’re within the midst of probably the most contentious elections in American historical past. Whereas it’s straightforward to make the case that the current circumstances are completely different than these in previous elections, historical past tells an interesting story. No matter who wins, the markets typically react effectively over the next yr. Whereas many/most/all of us can not look forward to 2020 to finish, we’re happy that our funding programs are poised to react to regardless of the pandemic, politics, economics or markets throw at us.

As all the time, we thanks for what you are promoting and confidence in BCM.

This text was contributed by Dave Haviland, Portfolio Supervisor and Managing Associate at Beaumont Capital Administration, a participant within the ETF Strategist Channel.

For extra insights like these, go to BCM’s weblog at weblog.investbcm.com.

Initially revealed by Beaumont Capital Administration

Disclosures:

Copyright © 2020 Beaumont Capital Administration LLC. All rights reserved. All supplies showing on this commentary are protected by copyright as a collective work or compilation beneath U.S. copyright legal guidelines and are the property of Beaumont Capital Administration. Chances are you’ll not copy, reproduce, publish, use, create by-product works, transmit, promote or in any approach exploit any content material, in complete or partially, on this commentary with out specific permission from Beaumont Capital Administration.

Previous efficiency is not any assure of future outcomes. Index efficiency is proven on a gross foundation and an funding can’t be made straight in an index. The efficiency of any ETFs, as contributors or detractors to the technique, are offered on a gross foundation. An Change Traded Fund (ETF) is a safety that tracks an index, a commodity or a basket of property like an index fund, however trades like a inventory on an change. ETFs expertise worth modifications all through the day as they’re purchased and offered. All BCM methods make investments solely in long-only ETFs.

This materials is offered for informational functions solely and doesn’t in any sense represent a solicitation or supply for the acquisition or sale of a particular safety or different funding choices, nor does it represent funding recommendation for any particular person. The fabric might comprise ahead or backward-looking statements relating to intent, beliefs relating to present or previous expectations. The views expressed are additionally topic to vary primarily based on market and different circumstances. The knowledge introduced on this report is predicated on knowledge obtained from third occasion sources. Though it’s believed to be correct, no illustration or guarantee is made as to its accuracy or completeness.

As with all investments, there are related inherent dangers together with lack of principal. Inventory markets, particularly international markets, are unstable and might decline considerably in response to opposed issuer, political, regulatory, market, or financial developments. Sector and issue investments focus in a specific trade or funding attribute, and the investments’ efficiency might rely closely on the efficiency of that trade or attribute and be extra unstable than the efficiency of much less concentrated funding choices and the market as a complete. Securities of firms with smaller market capitalizations are typically extra unstable and fewer liquid than bigger firm shares. International markets, significantly rising markets, will be extra unstable than U.S. markets as a result of elevated political, regulatory, social or financial uncertainties. Fastened Earnings investments have publicity to credit score, rate of interest, market, and inflation danger.

Diversification doesn’t guarantee a revenue or assure towards a loss.

The Customary & Poor’s (S&P) 500® Index is an unmanaged index that tracks the efficiency of 500 extensively held, large-capitalization U.S. shares. Indices are usually not managed and don’t incur charges or bills. The S&P Small Cap 600® Index is an unmanaged index that tracks the efficiency of 600 extensively held, small-capitalization U.S. shares. The MSCI World Index is a free float-adjusted market capitalization weighted index that’s designed to measure the fairness market efficiency of developed markets. The MSCI World ex-U.S. Index is a free float-adjusted market capitalization weighted index that’s designed to measure the fairness market efficiency of developed markets, excluding america. The MSCI ACWI Index captures massive and mid-cap illustration throughout 23 Developed Markets and 26 Rising Markets international locations. The MSCI ACWI Index ex-U.S. captures massive and mid-cap illustration throughout 22 Developed Markets and 26 Rising Markets international locations, excluding america. The Bloomberg Barclay’s U.S. Mixture Bond Index is a broad base index and is usually used to symbolize funding grade bonds being traded in america.

“S&P 500®”, and “S&P Small Cap 600®” are registered logos of Customary & Poor’s, Inc., a division of S&P International, Inc. MSCI® is the trademark of MSCI Inc. and/or its subsidiaries.

The BCM funding methods will not be applicable for everybody. As a result of periodic rebalancing nature of our methods, they will not be applicable for these traders who need common withdrawals or frequent deposits.

For Funding Skilled use with purchasers, not for unbiased distribution. Please contact your BCM Regional Marketing consultant for extra data or to deal with any questions that you will have.

Beaumont Capital Administration was initially created in 2009 as a separate division of Beaumont Monetary Companions, LLC. Beaumont Capital Administration LLC spun off as its personal entity as of half/2020. Beaumont Monetary Companions, LLC was initially registered as Beaumont Belief Associates in 1981 and was reorganized into Beaumont Monetary Companions, LLC in 1999.

Beaumont Capital Administration LLC

75 2nd Ave, Suite 700, Needham, MA 02494 (844-401-7699)

Learn extra on ETFtrends.com.

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.