By Patrick Watson

I attempt to not blame economists for being flawed. I feel most attempt to interpret the information pretty. It’s straightforward to overlook (or misunderstand) essential info.

So I’m shocked how so many in any other case considerate, data-driven analysts repeat the “unemployment advantages deter folks from working” narrative whereas citing no information in any respect.

Absolutely if they’d any supporting information, they might point out it… however no. They merely assert thousands and thousands of individuals don’t need to work as a result of the federal government pays a lot.

Is that taking place typically? In all probability, however these analysts say it’s regular. Additionally they don’t point out proof on the contrary—as an example, the information displaying on-line job searches haven’t elevated in states the place the governors are chopping off advantages.

Or the truth that some 9 million American staff had been denied unemployment advantages within the pandemic, usually attributable to bureaucratic snafus. None of them are being paid to not work.

In actuality, this labor scarcity predated the pandemic and can most likely outlast it, too. Larger issues are occurring… they usually might sign the type of modifications that solely occur each few a long time.

Or each few centuries.

Supply: Wikimedia Commons

Livid Development

For an financial system to develop, it has to provide extra items and companies. We now have an equation for that. It comes from the components of manufacturing.

All items and companies emerge from some mixture of:

- Land and pure assets

Because you want all 4 components as a way to produce something, modifications of their provide are essential.

Labor was plentiful for many of human historical past. Beginning charges had been excessive, and most work didn’t require numerous training. This modified because the Industrial Revolution made jobs extra technical and synthetic contraception lowered household sizes.

However countering that, we had a postwar Child Growth. Extra girls entered the labor power, and globalization let massive nations like China and India deploy their huge labor provide extra effectively.

Capital was traditionally extra scarce. However not too long ago, its provide grew as fashionable monetary markets let it stream extra freely. That mixture—plentiful labor and plentiful capital—explains a lot of the livid progress seen in the previous couple of a long time.

Each are needed… which is why a labor scarcity is an enormous drawback.

Supply: Kevin McGuire/Flickr

Lacking Labor

Now we have now a unique mixture. The financial system has extra capital than ever, due to the Federal Reserve and different central banks. Cash, and the issues it could purchase, are in every single place.

What’s not in every single place is labor, or no less than expert labor, as Child Boomers retire or die and youthful generations have fewer kids. The opposite labor progress components—girls working outdoors the house, China’s emergence, and many others.—had been one-time occasions. Nothing else like them is on the horizon.

That’s why wages are beginning to rise. It’s easy provide and demand. When employers have a number of candidates for each open place, they’ll select the one they take into account most cost-effective. That was the case for years. Now, in lots of industries, it’s not.

Equally, staff used to consider (usually appropriately) that employers had the higher hand. They had been reluctant to demand increased wages or higher working circumstances. That is additionally altering.

The scarcity might ease considerably as pandemic security considerations diminish, however I feel that is greater. Employers who hope to keep away from wage will increase will face rising strain as rivals take their income. And that’s not their solely drawback.

1960s Redux

Capital and labor don’t must be in battle. We may have an financial system the place entrepreneurs and traders are well-rewarded for the dangers they take whereas staff are paid pretty and handled properly. It’s not inconceivable. But it surely does appear uncommon.

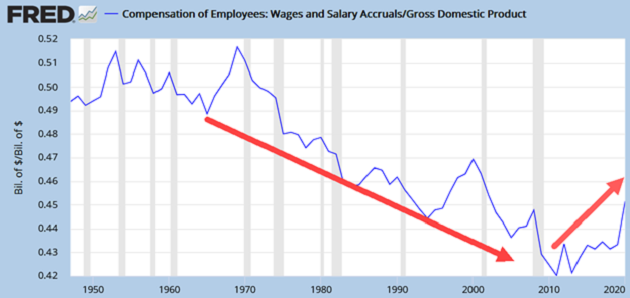

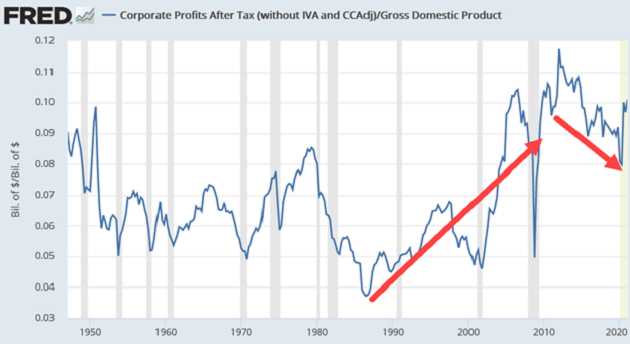

Take into account these two charts. The primary exhibits whole US wages as a proportion of Gross Home Product (GDP). The second is after-tax company income as a proportion of nominal GDP. I added arrows to spotlight the final course every has been transferring over time.

Supply: St. Louis Federal Reserve

You may see wages peaked (relative to GDP) within the late 1960s, then fell steadily (although with a short progress spurt within the 1990s). In the meantime, company income (notice that is all firms, not simply public ones) turned increased within the mid-1980s however actually took off within the early 2000s.

One thing appears to have occurred round 2010–2012. Employee compensation started taking a much bigger share of GDP whereas company income retreated.

What’s occurring right here? Many components contribute, however 2010 occurs to be when the oldest Child Boomers turned 65. The demographic modifications behind the present labor scarcity accelerated about that point.

So all this would possibly make excellent sense. Most employers want staff. If they need to pay increased wages to compete for a shrinking labor power, it should usually come out of income. That’s very true in industries the place competitors makes value will increase troublesome.

This mix—rising wages and falling company income—is uncommon in postwar US historical past. It occurred for a couple of years within the late 1960s.

Now we appear to be within the early levels of one other such interval. We’ll see a considerably totally different financial system if it persists.

Will probably be higher in some methods, worse in others… however positively totally different.

Initially printed by Mauldin Economics, 6/29/21

Learn extra on ETFtrends.com.

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.