By Nottingham Advisors Asset Administration

By Nottingham Advisors Asset Administration

Financial Overview

The most recent studying for Q2 GDP confirmed a -31.4% annualized decline in financial exercise throughout the quarter. With the shut of the third quarter upon us, the New York Fed Nowcast report suggests a +14.1% rebound in Q3, whereas the Atlanta Fed GDPNow forecast estimates a extra strong +32.0% surge in items and companies. This may be extra suggestive of a standard V-shaped restoration, a subject presently being debated amongst politicians as we head into the November elections.

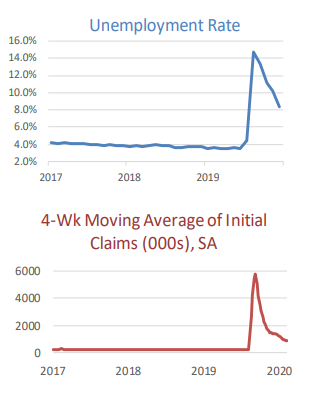

The Unemployment Price for August dipped to eight.4%, topping estimates of 9.8%, as 1.Four million jobs have been recovered. Common Hourly Earnings edged up +0.4% MoM and +4.7% YoY, whereas Common Weekly Hours got here in at 34.6. The JOLTS Job Openings quantity for July rose to six.6 million and weekly Preliminary Jobless Claims for August averaged 863okay.

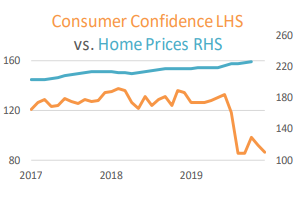

Housing remained a shiny spot in lots of areas of the nation – main city facilities being the exception – as folks seemed to the suburbs for aid from inhabitants density of enormous cities. New Dwelling Gross sales rose +4.8% MoM in August, whereas Present Dwelling Gross sales met expectations at +2.4% MoM and Pending Dwelling Gross sales surged +8.8% MoM (and a strong +20.5% YoY). The S&P CoreLogic CS US Dwelling Value Index was up +4.8% YoY by means of July.

From right here, the financial way forward for the US will likely be largely depending on whether or not Congress passes additional stimulus. The $2.2 trillion CARES Act saved folks and corporations afloat throughout the early days of Covid and now these advantages are waning. We’re seeing pickups in layoffs and furloughs at many firms within the journey and leisure area, together with theme parks, airways, hospitality and sports activities.

[wce_code id=192]

The Fed stays dedicated to low rates of interest till at the least 2023 and is prepared to let inflation run scorching ought to we see a pickup in financial exercise. Inflation hedges stay cheap as the availability of cash within the US continues to develop.

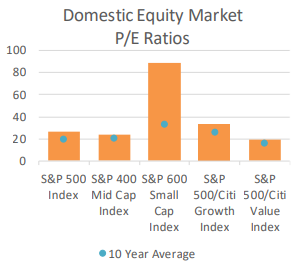

Home Fairness

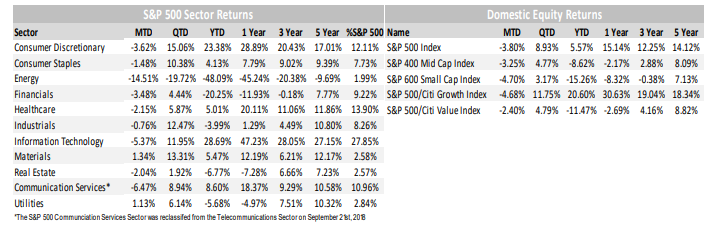

US Equities misplaced floor in September, with the benchmark S&P 500 index falling -3.8% to shut the month at 3,386. Regardless of September’s pullback, which noticed an intra-month peak to trough decline of greater than -10%, the

S&P 500 staged a fast rebound as traders purchased the dip. Broad financial knowledge continued to enhance all through the quarter, which helped buoy Massive-Caps by +8.93% throughout the third quarter, propelling the benchmark up +5.57% yr to this point.

Mid- and Small-Caps additionally fell throughout September, with the S&P 400 and 600 Indices falling -3.25% and -4.70%, respectively. Each posted positive aspects throughout the quarter, up +4.77% and three.17% apiece, however stay firmly within the crimson yr to this point, down -8.62% and -15.25%, respectively, highlighting the disparity between Massive- and Small-Caps and trepidation round nonFAAMG (Fb, Apple, Amazon, Microsoft, Google) threat property.

Progress shares underperformed throughout the quarter, with the S&P 500 Progress Index falling -4.68%, in comparison with the S&P 500 Worth Index which fell solely -2.80% throughout the interval as traders start to ponder the “re-opening commerce” which can be extra Worth pushed and economically delicate. Whereas this commerce has proven indicators of life earlier than, earlier months of Worth outperformance have been head fakes; nonetheless, with Progress outperforming Worth by greater than 32 proportion factors yr to this point (+20.61% vs. -11.90%), the case can clearly be made for a rotation out of what has labored into what has not.

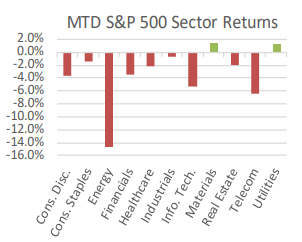

From a sector standpoint, solely 2 of 11 sectors completed the month in optimistic territory, with Supplies and Utilities posting positive aspects of +1.34% and +1.13%, respectively. Of the remaining sectors in adverse territory, Communication Providers, Know-how, and Shopper Discretionary posted losses of -6.47%, -5.34% and -3.62%, respectively. Know-how and Shopper Discretionary stay the yr’s greatest performers by a large margin, up +28.69% and +23.38%. Different notable decliners included the Power sector, which misplaced -14.51% on the month and has misplaced almost half its worth yr to this point. Power now represents a negligible 2% of the S&P 500 Index, and after Exxon’s elimination from the Dow Jones Industrial Common, represents the shift going down to Progress oriented sectors and a transition to renewable power sources.

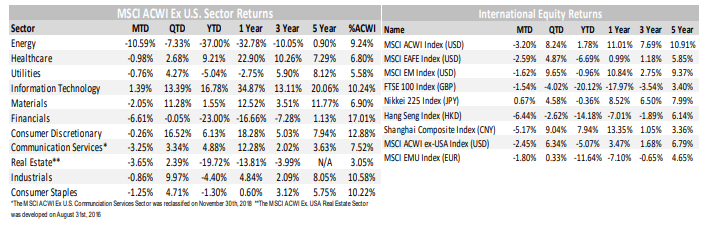

Worldwide Fairness

Worldwide Equities posted slight declines in September, with each Developed and Rising Markets (EM)equities faring higher than their US counterparts. Developed Markets (DM) as measured by the MSCI EAFE Index fell -2.59% on the month, whereas Rising Markets, as measured by the MSCI EM Index, fell -1.62%. Regardless of DM and EM equities outperforming US equities on the month, their efficiency was blended throughout the quarter. DM underperformed throughout the quarter, gaining solely +4.87%, whereas EM outperformed gaining +9.65%. Each have been helped by a weaker US Greenback – however, with Asian financial knowledge bettering at a speedy clip it shouldn’t come as a shock that EM outperformed DM throughout the interval. For the yr, DM has misplaced -6.69%, whereas EM has misplaced solely -0.96%, placing each DM and EM forward of US Mid- and Small-Caps, however trailing the Massive-Cap S&P 500 Index.

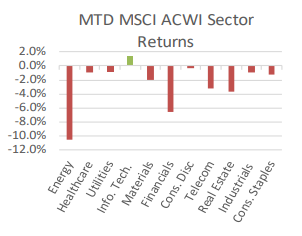

From a sector standpoint, only one of 11 sectors completed the month in optimistic territory, with the MSCI ACWI ex USA Know-how sector gaining +1.39% throughout the interval. Know-how shares exterior the US proceed to be high performers, with the sector up +16.78% yr to this point. Power was the worst performing sector on the month, down -10.59%, and is down -37.00% for the yr. Much like the US market, Worth shares proceed to underperform internationally; nonetheless, with Progress areas onerous to return by in DM areas corresponding to Europe, traders have turned their consideration to Asia to concentrate on behemoths corresponding to Tencent and Alibaba. Each firms dominate their respective markets, however have market caps which are dwarfed by their US equivalents, regardless of related platform primarily based enterprise fashions. With the a lot anticipated preliminary public providing of Ant, and the current inclusion of Alibaba within the Dangle Seng (Hong Kong) Index, potential catalysts are abound for EM Know-how to proceed to draw investor curiosity.

From a regional standpoint, China and Japan continued their management amongst main worldwide benchmarks. In Japan, the Nikkei 225 Index gained +0.67% in JPY phrases on the month and has outperformed DM on a yr to this point foundation returning -0.36%. China, as measured by the Shanghai Composite, misplaced -5.17% on the month in CNY phrases, regardless of the Yuan’s appreciation versus the US Greenback. The Shanghai Composite was a high performer throughout the quarter, gaining +9.04%, and is an outperformer yr to this point gaining +7.94%.

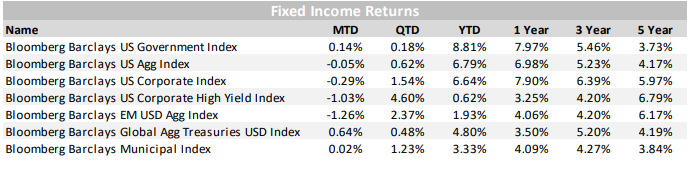

Fastened Earnings

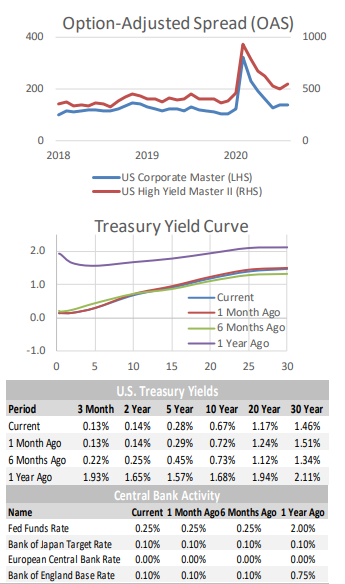

Over the previous month, Treasury yields have been comparatively secure, transferring only some foundation factors increased. In August, charges had additionally elevated. Even after two consecutive months of rising Treasury yields, we stay over 100 foundation factors decrease than the place most maturities started the yr, with solely the 30 yr Treasury having fallen barely lower than that.

With rates of interest having moved little in September, and credit score spreads trending wider, Funding Grade and Excessive Yield bonds gave again a few of their current positive aspects, underperforming Authorities bonds and the broad index (US Agg). US Greenback energy labored in opposition to Rising Market bond returns in September.

Municipal returns have been flat within the month, and their relative worth to Treasury bonds has been pretty secure since mid-year. Tax-free bonds have continued to see vital curiosity from traders and powerful inflows into funds providing tax-advantaged earnings. That is possible not unrelated to the approaching election.

The Federal Reserve want to let inflation run increased than it has prior to now, hoping to common 2% (that means it will be allowed to run above 2% for a time frame, as a result of the previous decade it has run under 2%). The European Central Financial institution is contemplating following go well with, with a “symmetric 2% inflation goal.” It was good of them to phrase it in another way, however the coverage that they’re contemplating is an identical to the Fed’s “common inflation concentrating on” (AIT) of two%.

There are presently examples of frictional inflation because of having shut down manufacturing throughout the Covid lock-down, adopted by demand recovering quicker than provide (lumber costs are a superb instance). Broad primarily based inflation usually presents itself when an financial system is operating scorching and at full employment. Presently, we appear removed from that situation, however these are uncommon occasions, which require diligent monitoring.

Different Investments

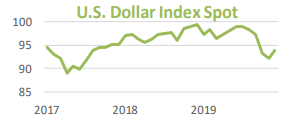

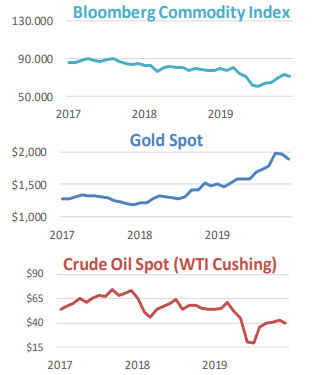

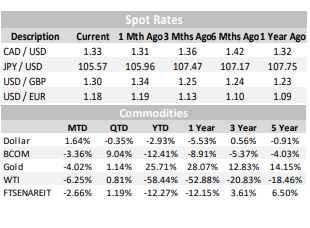

Different Investments have been principally adverse in September, hampered by a threat off atmosphere that noticed international fairness costs decline, in addition to a stronger US Greenback. The US Greenback, as measured by the DXY Index gained +1.9% in September after declining every of the earlier 4 months. The Greenback bounced again after falling -6.9% from its April highs, and stays down -5.2% over the previous 6 months.

The Greenback’s energy put strain on commodities broadly, as measured by the Bloomberg Commodities Index, which fell -3.4% on the month. West Texas Intermediate (WTI) crude oil fell -5.6%, or greater than $2/barrel to shut at $40/barrel on the NYMEX. Gold additionally declined in September, falling -4.2%, or $72/ounce, to shut at $1,885/ounce. The shiny metallic has been a beneficiary of low rates of interest, a weak greenback, and falling actual yields, which have pushed costs to new highs. Gold stays up +24.3% yr to this point, which places it forward of all main asset lessons. With the Federal Reserve pledging to carry charges at zero for the intermediate time period, in addition to let inflation exceed its 2% goal, Gold costs might have further tailwinds transferring ahead.

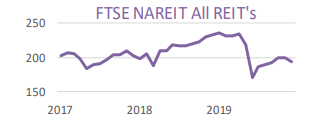

Actual Property, as measured by the FTSE NAREIT All REIT Index remained underneath strain as effectively, falling -3.1% on the month. Actual Property stays down greater than -17% from its January highs, and reveals few indicators of rebounding within the present atmosphere.

Volatility, as measured by the CBOE VIX Index, was largely unchanged on the month, falling -0.15% to shut at 26.37. Volatility has remained elevated as uncertainty round financial exercise, an increase in coronavirus circumstances, future stimulus, and November’s election (amongst others) persists. The VIX index has risen greater than +80% yr to this point, however stays effectively off its all-time excessive reached again in March.

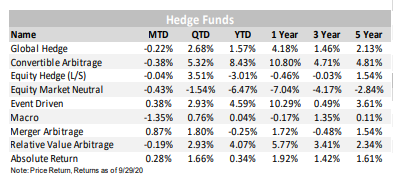

Hedge Fund methods posted blended outcomes throughout the month, with three of 9 methods tracked posting optimistic returns on common. Merger Arbitrage was the highest performer, up +0.87% on the month, whereas Macro methods have been the worst performer down -1.35% throughout the interval. For the yr, the vary of outcomes between methods continues to widen, with the perfect performer, Convertible Arbitrage up +8.43% and the worst performer, Fairness Market Impartial down -6.47%, highlighting the disparity amongst methods usually grouped collectively as liquid options.

ESG

This yr’s September Local weather Week introduced the main target again on the environmental facet of ESG. We noticed company bulletins for net-zero emission targets from AT&T, Walmart, Morgan Stanley, Google, Ford, Fb and extra. As help for ESG investing continues to develop, will probably be necessary for firms to observe by means of on these initiatives over the approaching many years to show their dedication to ESG.

Along with company pledges, on September 22nd, the World Financial Discussion board launched a set of common ESG measures and disclosures to assist firms report nonfinancial disclosures centered on 4 pillars; folks, planet, prosperity and ideas of governance. This can be a step towards making stakeholder capitalism measurable and continues to achieve help from firms; with some planning to start out incorporating instantly.

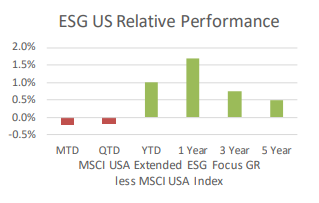

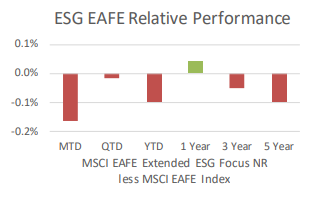

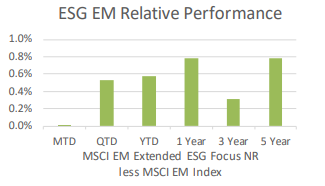

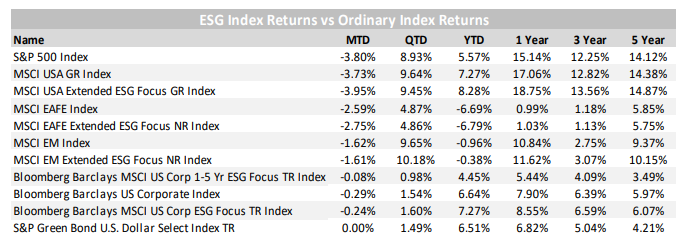

The MSCI USA Prolonged ESG Focus Index underperformed the MSCI USA Index by 22 bps for the month however nonetheless outperformed yr to this point by 102 bps. The MSCI EAFE ESG Centered Index returned 16 bps lower than the MSCI EAFE Index for the month and has now underperformed by 10 bps YTD. In the meantime, the MSCI EM ESG Centered Index outperformed on all time durations we monitor, up 1 bp for the month and 58 bps yr to this point.

The Bloomberg Barclays MSCI US Corp ESG Focus continues to carry out effectively, up +7.27% for the yr,

in comparison with the Bloomberg Barclays US Company Index which is up +6.64% YTD.

Nottingham Advisors, Inc. (“Nottingham”) is an SEC registered funding adviser with its principal place of work within the State of New York. Nottingham and its representatives are in compliance with the present registration necessities imposed upon registered funding advisers by these states by which Nottingham maintains shoppers. Nottingham might solely transact enterprise in these states by which it’s registered, or qualifies for an exemption or exclusion from registration necessities. This materials is proscribed to the dissemination of common data pertaining to Nottingham’s funding advisory/administration companies. Any subsequent, direct communication by Nottingham with a potential shopper shall be performed by a consultant that’s both registered or qualifies for an exemption or exclusion from registration within the state the place the possible shopper resides.

The knowledge contained herein shouldn’t be construed as personalised funding recommendation. Previous efficiency isn’t any assure of future outcomes. Data contained herein shouldn’t be thought of as a solicitation to purchase or promote any safety. Investing within the inventory market entails the chance of loss, together with lack of principal invested, and might not be appropriate for all traders. This materials comprises sure forward-looking statements which point out future potentialities. Precise outcomes might differ materially from the expectations portrayed in such forward-looking statements. As such, there isn’t a assure that any views and opinions expressed on this letter will come to move. Moreover, this materials comprises data derived from third occasion sources. Though we imagine these sources to be dependable, we make no representations as to the accuracy of any data ready by any unaffiliated third occasion included herein, and take no duty due to this fact. All expressions of opinion mirror the judgment of the authors as of the date of publication and are topic to alter with out prior discover. Previous efficiency isn’t a sign of future outcomes.

The indices referenced within the Nottingham Month-to-month Market Wrap are unmanaged and can’t be invested in instantly. The returns of those indices don’t mirror any funding administration charges or transaction bills. Had these further charges and bills been mirrored, the returns of those indices would have been decrease. Data herein has been obtained from third occasion sources which are believed to be dependable; nonetheless, the accuracy of the info isn’t assured by Nottingham Advisors. The content material of this report is as present as of the date indicated and is topic to alter with out discover.

For data pertaining to the registration standing of Nottingham, please contact Nottingham or confer with the Funding Adviser Public Disclosure website (www.adviserinfo.sec.gov). For added details about Nottingham, together with charges and companies, ship for our disclosure assertion as set forth on Type ADV from Nottingham utilizing the contact data herein. Please learn the disclosure assertion fastidiously earlier than you make investments or ship cash.

Learn extra on ETFtrends.com.

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.