Of the “identified identified” dangers in monetary markets immediately, we view tightening financial coverage as one of many high considerations, if not the highest concern. Lately, inflation-related fears have catapulted to the highest of traders’ minds, however tightening financial coverage, which is the first software to combat inflation, is the actual danger for asset costs. Amidst the COVID-19 pandemic, the U.S. Federal Reserve Financial institution (“the Fed”) created an accommodative financial coverage setting by slicing short-term rates of interest to zero and increasing the scale and scope of its asset buy plans (a.okay.a. quantitative easing). If the financial system or inflation reaccelerates, the Fed will possible must shift to tightening financial coverage. Throughout the latest Fed assembly, the Fed acknowledged that inflation was turning into a much bigger danger than beforehand anticipated and that they could improve short-term rates of interest sooner than beforehand anticipated. The large query for monetary markets will probably be whether or not the underlying macroeconomic setting can assist asset costs if the Fed strikes away from an accomodative financial coverage.

[wce_code id=192]

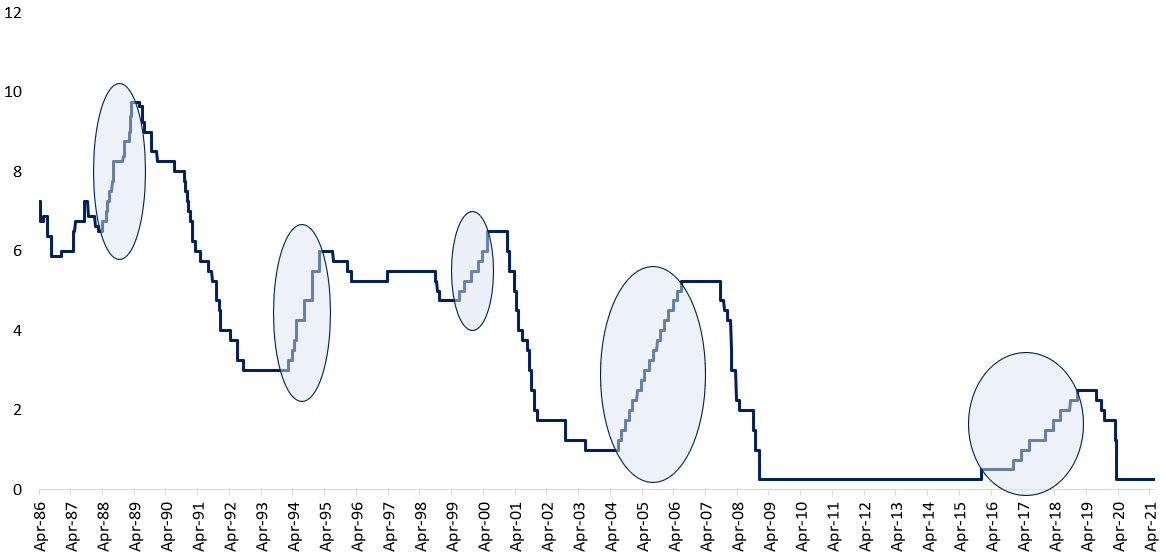

Determine 1. U.S. Federal Reserve Curiosity Price Hikes

Supply: Innealta Capital. Timeframe 03/31/1986 to 05/31/2021. Shaded areas characterize time intervals of substained Fed Fund Price will increase.

The knee-jerk response to tightening financial coverage is to promote belongings, notably riskier belongings, akin to equities and commodities. But, if we evaluation asset class efficiency throughout the previous 5 intervals of short-term rate of interest hikes, proven in Determine 2, equities have carried out exceptionally effectively. Developed Market equities exhibited a mean annualized return between eight to 10%, whereas Rising Market equities exhibited a mean annualized return of over 14%. Inside mounted revenue, shorter-dated U.S. Treasuries tended to outperform longer-dated U.S. Treasuries. On common, commodities tended to outperform all different asset lessons on an absolute foundation. At present, mounted revenue yields are decrease, and fairness market valuations are greater than at the start line of the 5 intervals analyzed aboved. Low yields and elevated valuations characterize vital headwinds to anticipated returns. Though historical past might repeat itself, we anticipate decrease fairness market mounted revenue market returns throughout the subsequent tightening financial coverage setting than what has occurred over the 5 intervals analyzed.

Determine 2. Multi-Asset Efficiency throughout FED Curiosity Price Mountain climbing Durations

Supply: Innealta Capital. Frequency month-to-month. Timeframe 04/30/1987 to 01/31/2019. Notice that EM fairness information began on 12/31/1987. Returns have been calculated on an annualized foundation. Danger was calculated as the usual deviation of month-to-month returns. Return to Danger ratio refers back to the Returns divided by the Danger. The “Common Return” and the “Common Return to Danger” refers back to the easy common throughout the next time frames: Please see disclosures for class descriptions. Previous efficiency just isn’t indicative of future outcomes. The 5 time frames below remark are 4/30/1987 – 12/31/1988, 1/31/1994 – 3/31/1995, 5/31/1999 – 6/30/2000, 5/31/2004 – 07/31/2006, and 11/30/2016 – 1/31/2019.

Over the previous 12 months, the U.S. financial system has recovered tremendously, given the impression of the COVID-19 pandemic. If the FED have been to start mountain climbing rates of interest immediately, we really feel that the present U.S. financial system is stronger than the U.S. financial system firstly of 4 of earlier 5 FED price hikes. Determine 3 exhibits that the Progress, Housing, and Client metrics usually display higher immediately. Employment information is combined; nonetheless, we anticipate that the employment information will enhance over the following few months. The numerous distinction immediately versus the opposite 5 time intervals is inflation. The latest Client Value Index announcement exhibits a +5.0% year-over-year change, a price considerably greater than CPI values firstly of the previous 5 Fed price hikes. In our opinion, a few of the CPI change is because of base results, whereas the stock drawdowns have created inflationary pressures. On the one hand, the U.S. financial system is at the moment very sturdy, whereas however, rising inflation is a comparatively new behavioral dynamic for each the Fed and traders.

Determine 3. Macroeconomic Snapshot

Supply: Innealta Capital. Timeframe 04/30/1987 to 05/31/2021.

Of the previous 5 Fed rate of interest mountain climbing intervals, the interval between April 1987 to December 1988 seems probably the most much like immediately from a macroeconomic perspective. What’s totally different about that timeframe in comparison with immediately is the intentions of the Fed. In 1987 and within the spirit of the Louvre Accord, the Fed tightened financial coverage to halt a depreciating greenback. At present, rising inflation not declining greenback is the danger. Primarily based on immediately’s macroeconomic setting, asset class historic efficiency, and present valuations, if the Fed have been to start elevating short-term rates of interest, we’d anticipate the next:

- Fastened Earnings markets would supply low returns. This primarily attributable to the low all-in yields at the moment accessible within the mounted revenue markets.

- Dangerous belongings would supply greater absolute returns than mounted revenue markets; nonetheless, the risk-adjusted returns could be decrease than the risk-adjusted returns over the previous 5 years.

- Bond-to-equity market correlation experiences a sustained shift from damaging correlation to constructive correlation. On this constructive correlation setting, mounted revenue doesn’t act as a portfolio volatility dampener and plenty of traders might want to rethink their portfolio building.

This materials is for informational functions and is meant for use for academic and illustrative functions solely. It’s not designed to cowl each facet of the related markets and isn’t meant for use as a common information to investing or as a supply of any particular funding advice. It’s not meant as a suggestion or solicitation for the acquisition or sale of any monetary instrument, funding services or products. This materials doesn’t represent funding recommendation, neither is it an alternative choice to such skilled recommendation or providers, nor ought to it’s used as a foundation for any choice or motion which will have an effect on your small business. Earlier than making any choice or taking any motion which will have an effect on your small business, it is best to seek the advice of a certified skilled adviser. In getting ready this materials we now have relied upon information equipped to us by third events. The knowledge has been compiled from sources believed to be dependable, however no illustration or guarantee, specific or implied, is made by Innealta Capital, LLC as to its accuracy, completeness or correctness. Innealta Capital, LLC doesn’t assure that the knowledge equipped is correct, full, or well timed, or make any warranties with regard to the outcomes obtained from its use. Innealta Capital, LLC has no obligations to replace any such info.

“U.S. Equities” refers back to the S&P 500 Whole Return Index, a diversified massive cap U.S. index that holds corporations throughout all eleven GICS sectors. “DM ex-U.S. Equities” refers back to the MSCI EAFE Internet Whole Return Index, is an fairness index which captures massive and mid cap illustration throughout 21 Developed Markets nations together with nations in Europe, Australasia and the Far East, excluding the U.S. and Canada. With 844 constituents, the index covers roughly 85% of the free float-adjusted market capitalization in every nation. “EM Equities” refers the MSCI Rising Market Internet Whole Return Index, which captures massive and mid cap illustration throughout 27 Rising Markets (EM) nations. With 1,424 constituents, the index covers roughly 85% of the free float-adjusted market capitalization in every nation. “Greenback” refers back to the U.S. Greenback Index, which is a measure of the worth of the US greenback relative to a basket of foreign exchange. “Commodities” refers back to the GSCI Commodity Whole Return Index, is a composite index of commodities that measures the efficiency of the commodity market. “UST 2y” refers back to the Bloomberg Barclays U.S. Treasury Bellwethers 2 Yr Whole Return Index. “UST 5y” refers back to the Bloomberg Barclays U.S. Treasury Bellwethers 5 Yr Whole Return Index. “UST 10y” refers back to the Bloomberg Barclays U.S. Treasury Bellwethers 10 Yr Whole Return Index. “UST 30y” refers back to the Bloomberg Barclays U.S. Treasury Bellwethers 30 Yr Whole Return Index.

787-INN-06/23/2021

Learn extra on ETFtrends.com.

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.