In spring 2020, the momentary closures {of professional} sports activities leagues through the preliminary coronavirus pandemic lockdown, coupled with the infusion of recent capital into monetary markets by the Federal Reserve and US Treasury, anointed a brand new class of retail merchants in monetary markets. This wave of recent market contributors brings with it a wave of liquidity that had been in any other case out of the attain of conventional monetary markets.

Click on right here to learn ‘Why a Rise in Retail Buying and selling Might Sign One other Mania’

Whereas the previous few months might have been exhilarating for retail merchants it’s a good time to look again into historical past for some informative cautionary tales from different retail manias in monetary historical past. Here’s a take a look at previous occasions, feelings and drama that led previous merchants to hunt fortune from comparable environments solely to go away many scuffling with the subsequent spoil.

Beneficial by Christopher Vecchio, CFA

Constructing Confidence in Buying and selling

Overflowing with Liquidity

In capital markets, liquidity will all the time discover its personal degree. Monetary capital will stream into the coffers of even probably the most bancrupt firms when there may be an abundance of liquidity. Take into account the instance of Hertz.

Chapter at its core is a state of affairs through which an organization’s belongings are value nothing. If belongings = liabilities + fairness, then it have to be the case that an organization in chapter has seen its fairness worn out, pushed to zero worth. And but, retail merchants continued to commerce into Hertz, pushing the agency’s shares increased.

In a way, that is what policymakers such because the Federal Reserve and US authorities meant: shore up the financial system towards the scourge of the pandemic so {that a} restoration can take root. In flip, there may be a lot extra liquidity in capital markets, that companies could be spared from illiquidity within the short-term and insolvency within the long-term. This may be summed in an analogy whereby regardless of ‘the holes within the backside of the cup, the highest would nonetheless overflow.’

Study from Others’ Errors

One other quote that carries weight with this introspection is one which my father would say to me once I was a toddler: “good individuals study from the errors of others.” The historical past of economic manias – not in contrast to the one we’ve witnessed for the reason that begin of March with the wave of recent retail merchants opening brokerage accounts – incessantly includes retail merchants who’ve loved a quick interval of success adopted by sustained discomfort.

Our hope right here is to focus on among the classes from monetary market historical past to different episodes of retail mania, when these with little expertise in hypothesis ventured into capital markets regardless. The lesson is obvious: sooner or later, the music stops. The punch bowl will get taken away.

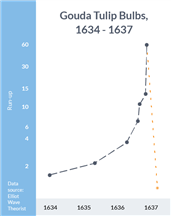

1637: DUTCH TULIP MANIA

The primary and maybe most well-known bubble in monetary historical past might be dated again to the 1600s. On the peak of the tulip mania, some single tulip bulbs, with no actual financial use, bought for greater than 10x the annual revenue of a talented craftworker (the ‘bubble ratio’). For reference, with Amazon shares buying and selling below $3,000, and the median American household revenue clocking in close to $60,000, this ‘bubble ratio’ remains to be simply 0.05).

It didn’t take lengthy till the bubble was unsustainable, with speculators unable to buy even the bottom high quality bulbs at their most cost-effective costs. When demand disappeared – there was nobody left to purchase – the tulip bubble burst nearly in a single day, driving many into lifelong money owed.

The Tulip mania happened from 1636-1637, and but practically 400 years later we discover ourselves discussing the pitfalls of what occurs when too many retail merchants speculate on belongings that don’t have any tangible financial use or worth. Why are new retail merchants, with a median age of 31, investing in a bankrupt firm like Hertz? Evidently human nature has not modified.

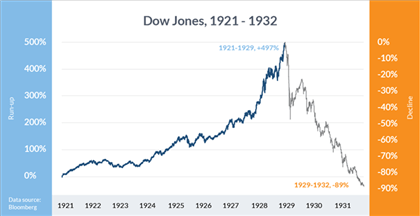

1929: WALL STREET CRASH

Probably the most well-known market crash in American historical past happened on the tail-end of the 1920s, capping an period of extra referred to as The Gilded Age. What was not so spectacular on this historic interval the tepid construct up. Whereas there wasn’t an acute bubble, it was nonetheless ended by a dramatic drop.

Certainly, the features through the previous decade had been comparatively tame by comparability to different main speculative bubbles. The plunge was spectacular, with the Dow Jones Industrial Common shedding practically 90% of its worth from September 1929 to July 1932. The following financial fallout from the inventory market crash grew to become what is called The Nice Despair.

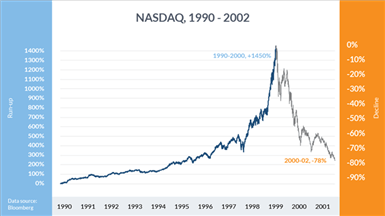

2000: NASDAQ/DOT COM BUBBLE

The period of deregulation beginning within the 1980s ultimately converged with the rise of expertise and web shares. The start of the ‘new financial system’ drove markets to dizzying heights by 2000. The NASDAQ rallied from 743 initially of 1995 to a excessive of 5048 on March 10, 2000. From October 1999 to March 2000 alone, the index doubled, creating the ‘dot com bubble.’

Thanks partially to the recession introduced on by the September 11 terrorist assaults, the dot com bubble burst and by late-2002, the NASDAQ had misplaced roughly 78% of its worth relative to its excessive in March 2000.

2007: US HOUSING MARKET CRASH

The housing market bubble is a novel bubble insofar because it was blown to assist reinflate the financial system after the 2000 NASDAQ/dot com bubble burst. To assist the financial system get better from the September 11 terrorist assaults and ensuing recession, the Federal Reserve lower rates of interest and flooded the market with liquidity – just like at the moment. Actual property costs and the valuations of homebuilders soared, drawing speculators into the housing market, referred to as “flippers”. At this time, we’ve got AirBNB hosts.

When the housing market bubble burst, the S&P 500 Homebuilding Complete Return Index fell by 90% from its peak in July 2005 to its low in November 2008. The results of the inventory and housing market crash was the worst monetary disaster since The Nice Despair, an period that we now referred to as The Nice Recession.

Beneficial by Christopher Vecchio, CFA

Prime Buying and selling Classes

Placing These Classes to Work

Mark Twain is understood for a lot of issues, however certainly one of his allegories with explicit software to present circumstances and that you just’re liable to listen to: “historical past doesn’t repeat itself however it typically rhymes.” The feelings that ruled our predecessors are the identical ones that we cope with at the moment when participating in monetary markets: greed, worry, pleasure, disappointment, amongst others.

In an age of world interconnected communications, info and knowledge travels world wide sooner than ever. Because of this the feelings we cope with when buying and selling can coalesce and snowball a lot sooner in a world market. Has this elevated the propensity for misinformation? Maybe. But when historical past is our information if solely by rhyme and never repetition, then we must be cautious of the truth that monetary bubbles, crises, and crashes are extra vulnerable to occurring than some other time in historical past.

Open an IG demo account at the moment.