DOW JONES, NIKKEI 225, ASX 200 INDEX OUTLOOK:Dow Jones, S&P 500 and Nasdaq 100 indexes closed -0.27%, -0.20% and -0.69% respectivelyShares pul

DOW JONES, NIKKEI 225, ASX 200 INDEX OUTLOOK:

- Dow Jones, S&P 500 and Nasdaq 100 indexes closed -0.27%, -0.20% and -0.69% respectively

- Shares pulled again broadly as retail gross sales figures disillusioned. 70% of Dow Jones constituents fell

- Asia-Pacific markets are positioned to commerce decrease. Traders awaited the FOMC assembly for clues in regards to the tapering timeline

Retail Gross sales, PPI, FOMC, Oil, Asia-Pacific Week-Forward:

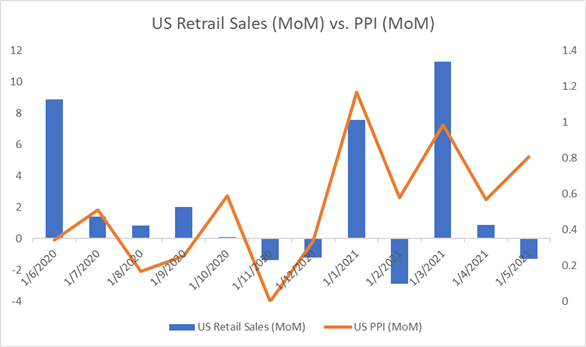

The Dow Jones Industrial Common pulled again for a second day as market weighed a lower-than-expected US retail gross sales determine alongside greater PPI (chart under). Client spending on autos, furnishings, electronics and supplies fell in Might, leading to a 1.3% MoM decline in retail gross sales. This can be attributed to a shift in spending habits as extra persons are going outside because the pandemic eases.

In the meantime, the producer value index (PPI) climbed 0.8% MoM, greater than a baseline forecast of 0.6%. This displays that costs of products at manufacturing facility doorways are rising at a faster-than-expected tempo, echoing readings from China and Japan earlier this months. PPI is broadly perceived as a number one indicator for CPI, as producers could intend to switch greater enter prices to completed merchandise, In consequence, inflationary pressures could also be seen within the months to return.

Market sentiment tilted to the cautious aspect as buyers awaited clues in regards to the Fed’s tapering timeline in a two-day FOMC assembly. Though the central financial institution is essentially anticipated to maintain its coverage charge unchanged till 2023, the chance of a gradual scaling again of its month-to-month bond buy program has risen not too long ago. This got here towards the backdrop of mounting inflationary pressures, ample liquidity circumstances and a strong financial restoration. The DXY US Greenback index traded steadily at 90.50, and the 10-year Treasury yield was hovering at across the 1.50% mark.

US Retail Gross sales vs PPI – Previous 12 Months

Supply: Bloomberg, DailyFX

On the commodities entrance,WTI crude oil costs surged 1.79% to a contemporary two-and-half 12 months excessive of $72.44. The underlying demand for vitality stays sturdy whereas provide stays constrained. US day by day air travellers surpassed 2 million for the primary time for the reason that pandemic, underscoring sturdy demand for gas as the height of the summer season journey season arrives. Larger oil costs could bolster commodity-linked currencies such because the Canadian Greenback and Norwegian Krone. A gathering between US and Russian leaders in the present day will likely be carefully watched by oil merchants.

Asia-Pacific markets are positioned to open on the again foot. Futures in Japan, mainland China, Hong Kong, Australia, Taiwan, Thailand and Singapore are within the purple, whereas these in South Korea are within the inexperienced. Wanting forward, China’s retail gross sales and industrial manufacturing information dominate the financial docket in the present day alongside Canadian inflation figures. Discover out extra from DailyFX financial calendar.

Japan’s Nikkei 225 index seems set to retreat from Tuesday’s excessive following a bitter lead from Wall Road. The expertise sector could also be susceptible to a pullback, whereas cyclical-oriented industrial and vitality sectors could present resilience. Japan’s day by day Covid-19 instances have fallen over the previous weeks, paving the best way for eradicating the state-of-emergency measures within the Tokyo and Osaka space. The index could also be positioned for additional positive aspects if Covid-related restrictions are eased.

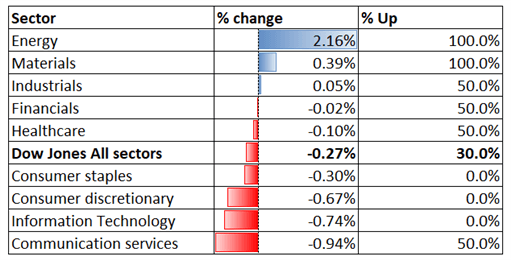

Wanting again to Tuesday’s shut, 6 out of 9 Dow Jones sectors ended decrease, with70% of the index’s constituents closing within the purple. Vitality (+2.16%) and supplies (+0.39%) outperformed, whereas communication companies (-0.94%) and data expertise (-0.74%) trailed behind.

Dow Jones Sector Efficiency 16-06-2021

Supply: Bloomberg, DailyFX

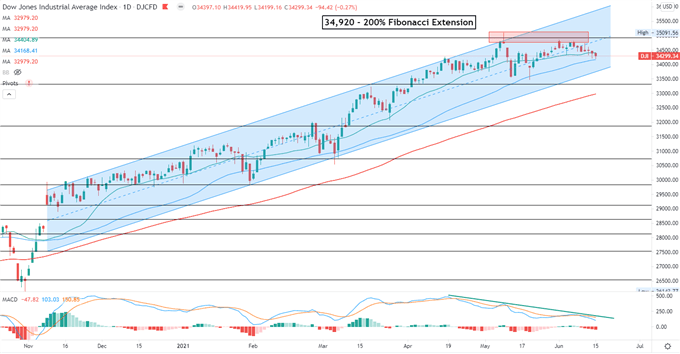

Dow Jones Index Technical Evaluation

The Dow Jones index did not breach the 200% Fibonacci extension degree (34,920) for a second time and has since entered a technical correction. This has possible resulted in a “Double Prime” sample, which can be seen as a bearish trend-reversal indicator. Costs stay inside an “Ascending Channel” fashioned since early November, the ceiling and the ground of which function key assist and resistance ranges respectively. Bearish MACD divergence means that bullish momentum is weakening.

Dow Jones Index – Each day Chart

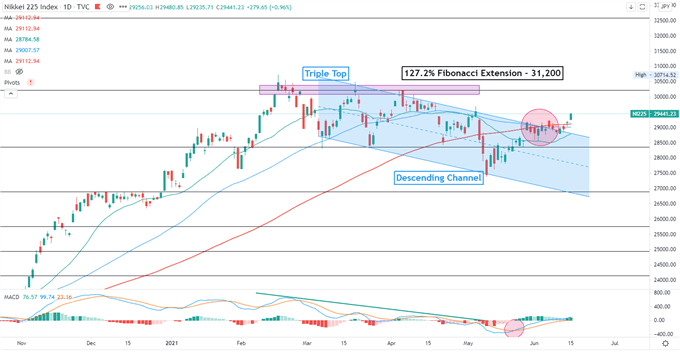

Nikkei 225 Index Technical Evaluation:

The Nikkei 225 index breached above the ceiling of the “Descending Channel” and has opened the door for additional positive aspects. A key resistance degree may be discovered at 31,200- the 127.2% Fibonacci extension. Costs have additionally breached above the 50- and 100-day SMA line, suggesting that near-term pattern has possible turned bullish The MACD oscillator is trending greater, underscoring bullish momentum.

Nikkei 225 Index – Each day Chart

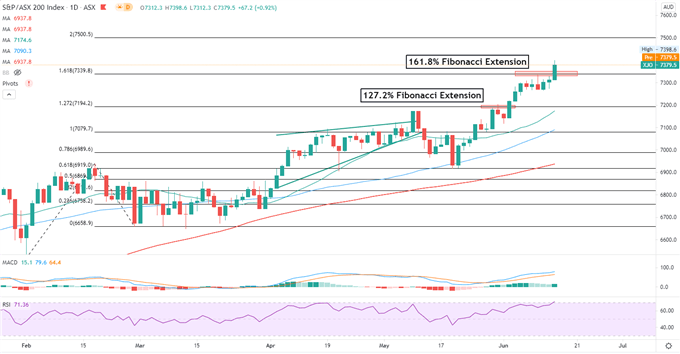

ASX 200 Index Technical Evaluation:

The ASX 200 index breached above a key resistance degree of seven,340 and closed at a contemporary file on Tuesday. Costs fashioned consecutive greater highs and better lows, marking a basic uptrend. The RSI oscillator has reached the overbought threshold of 70, hinting that the index could also be quickly overbought and should entice revenue taking. The MACD indicator fashioned a bullish crossover and trended greater, suggesting that upward momentum is dominating.

ASX 200 Index – Each day Chart

— Written by Margaret Yang, Strategist for DailyFX.com

To contact Margaret, use the Feedback part under or @margaretyjy on Twitter

factor contained in the

factor. That is most likely not what you meant to do!nn Load your software’s JavaScript bundle contained in the factor as an alternative.www.dailyfx.com