Central Financial institution Watch Overview:

- April is simply over one week outdated, however Fed policymakers have been lively within the intermeeting interval – and are prone to stay so within the run-up to the April 28 FOMC assembly.

- Fed officers have been fastidiously towing the road as to not spook markets that tapering is coming anytime quickly.

- Fed fund futures see better than a 90% likelihood that charges markets shall be on maintain by way of early-2022.

Preserve Calm and Carry On

On this version of Central Financial institution Watch, we’ll evaluation the speeches remodeled the previous week by numerous Federal Reserve policymakers, together with the Fed Chair himself. Within the prolonged interval forward of the April 28 assembly, Fed policymakers are prone to be extra current within the day-to-day machinations of monetary markets.

For extra data on central banks, please go to the DailyFX Central Financial institution Launch Calendar.

Really helpful by Christopher Vecchio, CFA

Get Your Free USD Forecast

Federal Reserve Resolute with Easing Stance

Because the Fed’s March 17 assembly, and even after the blowout US jobs market report, US Treasury yields have eased again. The drumbeat by policymakers that in any other case elevated US Treasury yields are an indication of the market’s confidence within the restoration, not an indication of persistent inflation, has continued in earnest. As famous within the March 30 iteration of this word, it stays the case that “it could be the Fed’s resolute insistence on not bucking to bond vigilantes that finally caps bond market volatility.”

April 1 – Bullard (St. Louis Fed president) says “given that inflation has usually been under the two% goal for a few years, an inflation end result modestly above 2% for a while can be a welcome growth for the FOMC.”

Daly (San Francisco Fed president) notes that “we know there’s an anticipated and importantly, underline, short-term rise in inflation that’s coming this yr as a result of we had low readings of inflation in the course of the worst months of Covid in 2020.” But she additionally cautioned in opposition to anticipating any change in coverage quickly, saying “we actually aren’t projecting reaching both aspect of our twin mandate in 2021. That’s the reason coverage is remaining accommodative so we will completely ship on these objectives.”

April 5 – Mester (Cleveland Fed president) calls the current March US jobs report “nice,” however says that current jobs development doesn’t imply the financial system is within the place the Fed sees a necessity to boost charges, noting “we’re nonetheless nearly 8.5 million jobs under the place we had been earlier than the pandemic so we want extra of these sorts of jobs experiences popping out.”

April 6 – Barkin (Richmond Fed president) outlined his expectations on development, saying “You’ve received extrafinancial savings. You’ve received fiscalstimulus funding pent-up demand from customers like me who’reexhausted from isolation and freed up by vaccines and hotterclimate.” He summarized his place by saying that he “anticipate[s] to see a very sturdy spring and summer time,” and “more jobs are coming because the financial system absolutely reopens.”

April 7 – Kaplan (Dallas Fed president) says that the Fed will proceed to accommodate aggressively to assist the financial system, but additionally notes that because the financial system improves, it will be “more healthy” to maneuver away from huge financial assist.

Evans (Chicago Fed president) says that “we’re going to need to go months and months into the higher-inflation expertise earlier than I’m going to even have an opinion on whether or not that is sustainable or not. And that’s going to be uncomfortable.”

Brainard (Fed governor) says that “our financial coverage ahead steerage is premised onoutcomes, not the outlook…and so it’ll be a while earlier than each employmentand inflation have achieved the sorts of outcomes which might be inthat ahead steerage”

The March FOMC minutes had been launched, and the Fed’s resolute stance in the direction of persevering with lodging remained as famous by two feedback specifically. First, that “participants famous that it will probably be a while till substantial additional progress towards the Committee’s maximum-employment and price-stability objectives can be realized.” Second, that “a variety of members highlighted the significance of the Committee clearly speaking its evaluation of progress towards its longer-run objectives properly upfront of the time when it may very well be judged substantial sufficient to warrant a change within the tempo of asset purchases.”

April 8 – Powell (Fed Chair), talking at a digital panel, says that the Fed “will present help to the financial system till it now not wants it,” and that they are going to “end the job and get again to an excellent financial system,” noting that “we should put money into lifting financial potential and inclusivity.” Whereas saying that “thousands and thousands of individuals can have a tough time discovering their method again into the workforce,” he was inspired by the truth that the “US financial system has up to now averted the worst case situation.”

Bullard (St. Louis Fed president) says that “full employment can occur inside the subsequent yr,” however now we have a “clearer” finish to the coronavirus pandemic previous to even start discussing tapering the Fed’s accommodative insurance policies.

Uncover what sort of foreign exchange dealer you’re

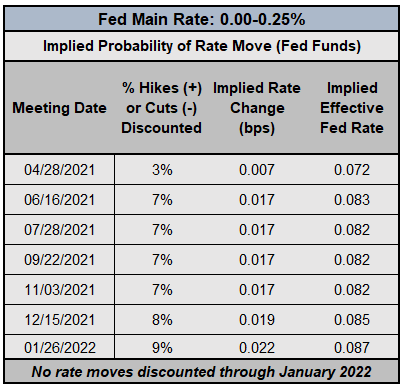

Federal Reserve Curiosity Charge Expectations (April 8, 2021) (Desk 1)

Because the sand passes by way of the hourglass, charges markets are taking the Fed’s resolute place at face worth: the primary price isn’t going anyplace anytime quickly. Fed funds futures are pricing in a 91% likelihood of no change in Fed charges by way of January 2022. There nonetheless hasn’t been sufficient of a shift to warrant a change in outlook, nor will we anticipate a change in outlook for the foreseeable future.

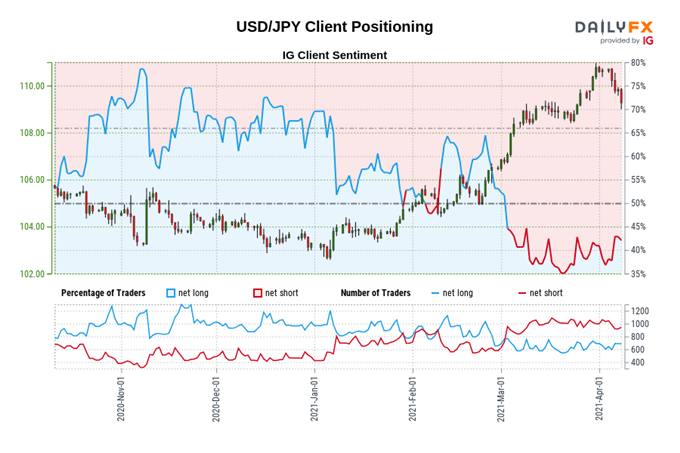

IG Consumer Sentiment Index: USD/JPY Charge Forecast (April 8, 2021) (Chart 1)

USD/JPY: Retail dealer information reveals 42.14% of merchants are net-long with the ratio of merchants quick to lengthy at 1.37 to 1. The variety of merchants net-long is 13.11% decrease than yesterday and 6.68% decrease from final week, whereas the variety of merchants net-short is 7.44% decrease than yesterday and 16.70% decrease from final week.

We sometimes take a contrarian view to crowd sentiment, and the very fact merchants are net-short suggests USD/JPY costs could proceed to rise.

Positioning is extra net-short than yesterday however much less net-short from final week. The mix of present sentiment and up to date adjustments offers us an extra combined USD/JPY buying and selling bias.

Really helpful by Christopher Vecchio, CFA

Traits of Profitable Merchants

— Written by Christopher Vecchio, CFA, Senior Foreign money Strategist

aspect contained in the

aspect. That is in all probability not what you meant to do!nn Load your utility’s JavaScript bundle contained in the aspect as an alternative.www.dailyfx.com