Central Financial institution Watch Overview:After a robust July US nonfarm payrolls report and extra sizzling inflation readings, Fed price hike

Central Financial institution Watch Overview:

- After a robust July US nonfarm payrolls report and extra sizzling inflation readings, Fed price hike odds are creeping larger forward of the August gathering in Jackson Gap.

- Fed fund futures are closely favoring the primary price hike in December 2022; odds are being pulled ahead for the September and November 2022 conferences as properly.

- Eurodollar contract spreads have widened significantly over the previous week; a full price hike has been priced-in by means of the tip of 2023.

US Information Deluge Provokes Hike Hypothesis

On this version of Central Financial institution Watch, we’ll assessment the speeches made in August by over the previous week by varied Federal Reserve policymakers – nearly each single policymaker aside from the Fed Chair himself. Little question about it, taper speak is growing within the run-up to the Jackson Gap Financial Coverage Symposium, set to happen later this month from the 26th to the 28th.

For extra data on central banks, please go to the DailyFX Central Financial institution Launch Calendar.

Extra Taper Discuss

Within the wake of the July FOMC assembly, and in mild of the surge within the delta variant caseload within the US, merchants started decreasing their expectations for a extra hawkish Federal Reserve. Nonetheless, the mixed impression of the sturdy July US nonfarm payrolls report – the second in a row – plus the July US inflation price report (CPI) has sparked a shift in each market expectations and language utilized by FOMC policymakers up to now in August.

August 1 – Kashkari (Minnesota president) stated that he “he was very optimistic the autumn could be a robust labor market with a lot of these Individuals coming again to work…but if persons are nervous in regards to the delta variant, that would sluggish a few of that labor market restoration and due to this fact be a drag on our financial restoration.”

August 2 – Waller (Fed governor) commented on the potential timing of a taper announcement, noting that he believes that the financial system “might be able to do an announcement bySeptember….If the roles experiences are available as I feel they’re going to within the subsequent two experiences, then in my opinion with tapering we must always go early and go quick, in an effort to make certain we’re in place to lift charges in 2022 if we have now to.”

August 3 – Bowman (Fed governor) supplied a extra cautious tone on the labor market, having famous that “despite the encouraging tempo of latest hiring, employment remains to be far under the place it was. In June of this 12 months, there have been 6.eight million fewer jobs than there have been in February 2020.”

August 4 – Bullard (St. Louis president) tried to soothe-say markets concerning excessive inflation readings, having famous that “it’s going to be extra persistent than what most individuals count on….I’d count on one thing between 2.5 and three% in 2022. It’s going to come down, however not as quick as what many individuals take note of.”

Clarida (Fed Vice Chair) commented on the surge in delta variant circumstances, saying “the financial and financial insurance policies presently in place ought to proceed to assist the sturdy enlargement in financial exercise that’s anticipated to be realized this 12 months, though, clearly, the speedy unfold of the Delta variant among the many nonetheless appreciable fraction of the inhabitants that’s unvaccinated is clearly a draw back threat for the outlook.”

Kaplan (Dallas president) chimed in on the taper timeline, noting “as lengthy as we proceed to make progress in July (jobs) numbers and in August jobs numbers, I feel we’d be higher off to begin adjusting these purchases quickly.”

August 5 – Waller (Fed governor) took an optimistic tone, saying “the financial system has rebounded in a tremendous means, and I feel that’s going to proceed. I’ve very excessive hopes for very excessive jobs experiences popping out tomorrow and the next month.”

Kashkari additionally regarded for a silver lining, noting that he’s “optimistic that we must always have a robust labor market within the fall, however the wrinkle now, so to talk, is delta.”

August 9 – Bostic (Atlanta president) got here out with a hawkish tone hinting at a sooner taper timeline, saying that the US financial system is “properly on the street to substantial progress towards our aim.”

August 10 – Evans (Chicago president), a famous dove, stated that he does “count on that we’re going to be on the level the place we’ve seen substantial additional progress later this 12 months — most likely later this 12 months. I don’t assume it’s going to be into subsequent 12 months.”

August 11 – Barkin (Richmond president) hinted {that a} taper is on the horizon, saying “We’re closing in … I don’t know precisely when that shall be. After we do shut in on it I’m very supportive of tapering and transferring again towards a standard surroundings as shortly because the financial system permits us.”

Bostic instructed that the Fed’s dedication to most employment meant that charges wouldn’t rise “too shortly.”

George (Kansas Metropolis president) supplied a hawkish tone, saying “Now, with the restoration underway, a transition from extraordinary financial coverage lodging to extra impartialsettings should comply with.”

Daly (San Francisco president) likewise supplied a hawkish set of feedback, indicating that it could be time to scale-back the ultra-accommodative coverage stance of the Fed “by the tip of the 12 months.”

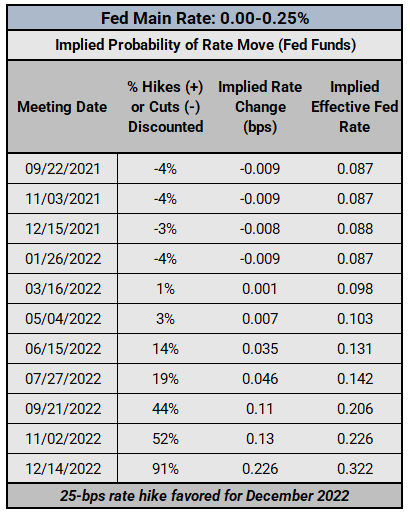

Federal Reserve Curiosity Charge Expectations: Fed Funds Futures (August 12, 2021) (Desk 1)

Forward of the July FOMC assembly, December 2022 was the favored month for the primary price transfer, clocking in with a 68% likelihood. Nonetheless, after the July US nonfarm payrolls report and the July US inflation price report (CPI), in addition to the litany of feedback by Fed policymakers, December 2022 now sees a 91% likelihood of a 25-bps price hike.

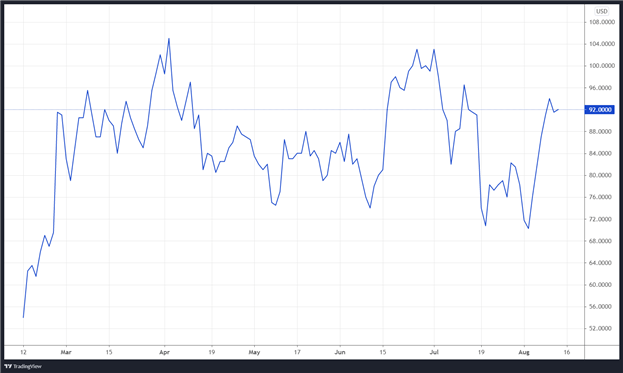

We will additionally measure whether or not a price hike is being priced-in utilizing Eurodollar contracts by inspecting the distinction in borrowing prices for business banks over a particular time horizon sooner or later. Chart 1 under showcases the distinction in borrowing prices – the unfold – for the August 2021 and December 2023 contracts, in an effort to gauge the place rates of interest are headed within the interim interval between August 2021 and December 2023.

EURODOLLAR FUTURES CONTRACT SPREAD (AUGUST 2021-DECEMBER 2023): DAILY RATE CHART (February to August 2021) (CHART 1)

Primarily based on the Eurodollar contract spreads, there 92-bps value of price hikes – collectively, three 25-bps price hikes, plus a 68% likelihood of a fourth hike – by December 2023. Over the previous week, we’ve seen the variety of basis-points priced-in improve from a low of 62-bps; in impact, a further full price hike has been discounted by means of the tip of 2023.

Traditionally talking, sharp upticks in price hike expectations vis-à-vis Eurodollar spreads have catered to a robust US Greenback surroundings. Certainly, technical advances by the DXY Index recommend a stronger buck could also be right here within the near-term.

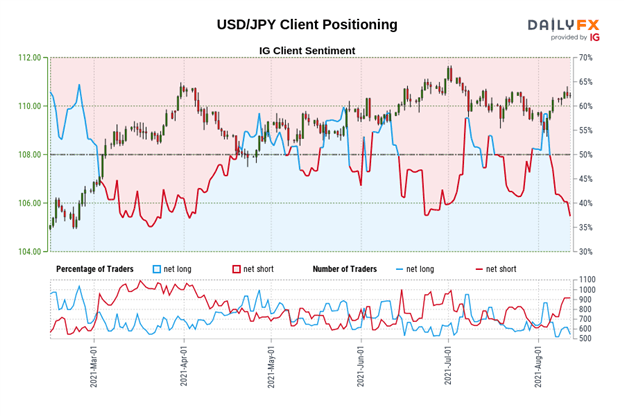

IG Shopper Sentiment Index: USD/JPY Charge Forecast (August 12, 2021) (Chart 2)

USD/JPY: Retail dealer knowledge exhibits 40.61% of merchants are net-long with the ratio of merchants brief to lengthy at 1.46 to 1. The variety of merchants net-long is 14.63% larger than yesterday and 6.42% decrease from final week, whereas the variety of merchants net-short is 3.38% larger than yesterday and 24.76% larger from final week.

We usually take a contrarian view to crowd sentiment, and the actual fact merchants are net-short suggests USD/JPY costs could proceed to rise.

Positioning is much less net-short than yesterday however extra net-short from final week. The mix of present sentiment and up to date adjustments provides us an additional combined USD/JPY buying and selling bias.

— Written by Christopher Vecchio, CFA, Senior Foreign money Strategist

component contained in the

component. That is most likely not what you meant to do!Load your software’s JavaScript bundle contained in the component as a substitute.

www.dailyfx.com