btc-usd Global markets opened with renewed attention on econom

Quick overview

- Global markets are focused on economic indicators and central bank policies, with key data from Australia, the U.S., and Canada influencing trading.

- The U.S. dollar rebounded as geopolitical tensions eased and optimism around U.S.-China trade relations improved.

- The Bank of Canada is expected to maintain its interest rate, while the U.S. ISM Services PMI is forecasted to show steady expansion.

- In the cryptocurrency market, Bitcoin and Ethereum have seen significant gains, driven by concerns over fiscal sustainability and successful upgrades.

Live BTC/USD Chart

BTC/USD

Global markets opened with renewed attention on economic indicators and central bank policy moves, with key data releases from Australia, the U.S., and Canada steering the day’s trading narrative.

U.S. Dollar Rebounds as Market Nerves Settle and Trade Talks Regain Momentum

The U.S. dollar strengthened broadly today, rebounding from Monday’s losses as geopolitical tensions appeared to ease and optimism around U.S.-China trade relations resurfaced. The move was largely a technical retracement of the prior session’s decline, but it also reflected a more stable tone across risk assets and macroeconomic signals.

Geopolitical Calm Aids Dollar Recovery

Monday’s market jitters were driven by fears of Russian retaliation after drone attacks linked to Ukraine, with worst-case scenarios briefly priced in. However, with no escalation materializing—particularly no movement on nuclear threats—those concerns faded quickly. That relief helped the dollar find support as investor sentiment shifted back toward cautious optimism.

U.S.-China Trade Dialogue Revives Risk Appetite

Another tailwind for the greenback came from progress in trade diplomacy. Diplomatic channels between the U.S. and China were reportedly active today, and the White House hinted at the possibility of a direct phone call between President Trump and President Xi. While no breakthroughs have emerged yet, the renewed communication itself calmed fears of further deterioration in trade relations.

Domestic Data Also Offers Support

The U.S. economic backdrop offered some reassurance as well. The latest JOLTS report for April showed job openings ticking higher, signaling ongoing resilience in the labor market despite global uncertainty. Though it was not a market-moving release, it contributed to the broader narrative that the U.S. economy remains on solid footing.

Currency Market Highlights

USD/JPY was the standout performer, surging 135 pips to 144.05, recovering nearly all of Monday’s losses. The pair bottomed during early European trading and moved steadily higher throughout the session, closing near its intraday highs.

EUR/USD weakened in parallel, reversing Monday’s modest gains and leaving the euro little changed for the week. Traders remain cautious ahead of upcoming trade headlines, the European Central Bank (ECB) meeting, and Friday’s non-farm payrolls report, which could set the tone for near-term euro direction.

The U.S. dollar’s strength against commodity-linked currencies was more modest. That’s partly because improving sentiment on trade also lifted commodity prices and equity markets, especially in energy and metals. As a result, those currencies found some underlying support.

Stocks Edge Higher, Led by Tech

In equity markets, European futures remained hesitant throughout the day, but U.S. indices gained traction in afternoon trade. Tech stocks—particularly semiconductor names—led the advance, reflecting revived investor confidence in growth sectors after a choppy start to the week.

Today’s Forex Events

Australia’s Q1 GDP Sets the Tone as Markets Await U.S. and Canadian Policy Signals

Australia’s release of first-quarter GDP data provided an early pulse check on Asia-Pacific economic health, but global attention is quickly shifting to North America. Investors are bracing for a series of closely watched releases: the ADP non-farm employment change and ISM Services PMI in the U.S., along with the Bank of Canada’s latest monetary policy decision.

Bank of Canada Poised to Hold Steady—for Now

Markets widely expect the Bank of Canada to keep its key interest rate unchanged at this week’s meeting. This follows a sharp 225 basis-point easing cycle over the past year, which the central bank paused during its most recent decision.

Still, speculation remains that further rate cuts may be on the horizon. RBC analysts point to weakening housing activity and softer labor market signals as potential justification for renewed policy easing. Even if the BoC stands pat, it is likely to retain a dovish bias, keeping the door open for more cuts later in the year. Wells Fargo sees a return to rate reductions as early as July, forecasting two additional 25 basis point cuts—one in the summer and another in October—as inflation continues to drift toward the bank’s 2% target and external trade pressures weigh on domestic growth.

U.S. ISM Services PMI: Signs of Steady Expansion

The U.S. ISM Services PMI is forecast to climb modestly to 52.0, up from a prior reading of 51.6. While U.S. manufacturing has been more visibly affected by recent trade disputes and tariffs, the services sector—which includes a wide range of industries from healthcare to transportation—has proven more resilient.

Wells Fargo analysts anticipate a slight uptick in the services index, attributing the expected improvement to easing trade tensions and consistent consumer demand. The data could reinforce optimism about the broader U.S. economy’s ability to sustain growth, despite lingering inflationary challenges.

Last week, markets were slower than what we’ve seen in recent months, with gold retreating as a result, the EUR/USD falling below 1.12 but returned above 1.14 this week, and stock markets continued upward too. The moves weren’t too big, but we opened 37 trading signals in total, finishing the week with 25 winning signals and 12 losing ones.

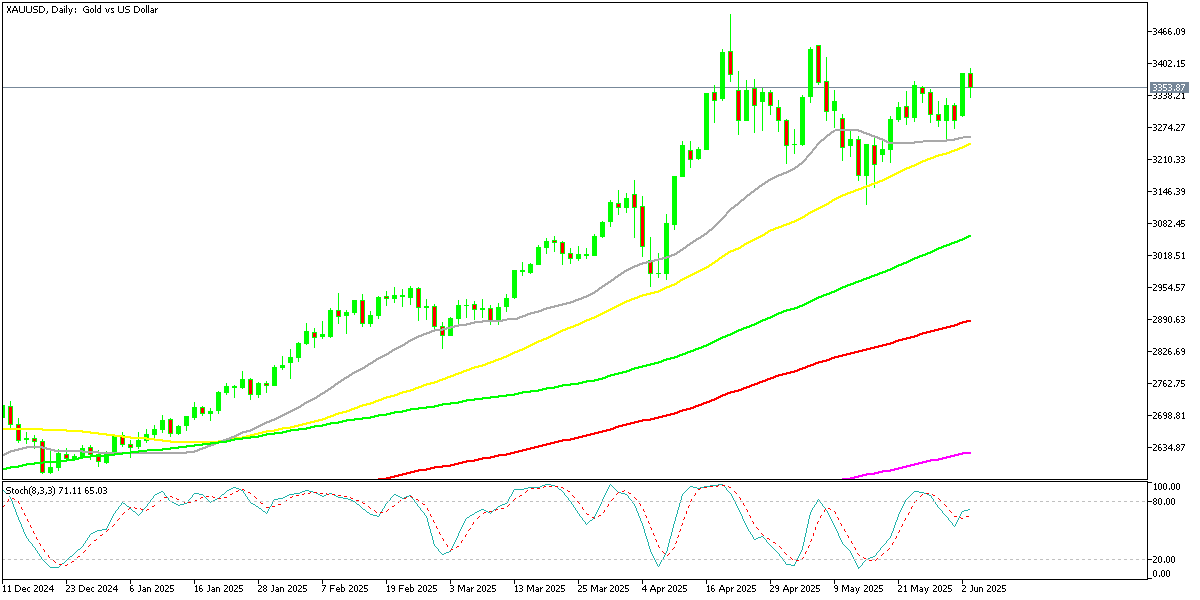

Gold Gives Some Back

Gold prices remain buoyant amid global uncertainty, with the precious metal trading close to the $3,500 mark—levels not seen since April. After recovering from lows around $3,200, gold’s appeal as a hedge has been reignited by ongoing geopolitical tensions, cautious investor sentiment, and shifting expectations around future Federal Reserve policy.

Despite some moments of consolidation between $3,120 and $3,500 earlier in May, gold continues to attract flows, particularly as inflation concerns and financial instability linger. However, resistance near the $3,500 level remains firm, and a decisive breakout has yet to occur.

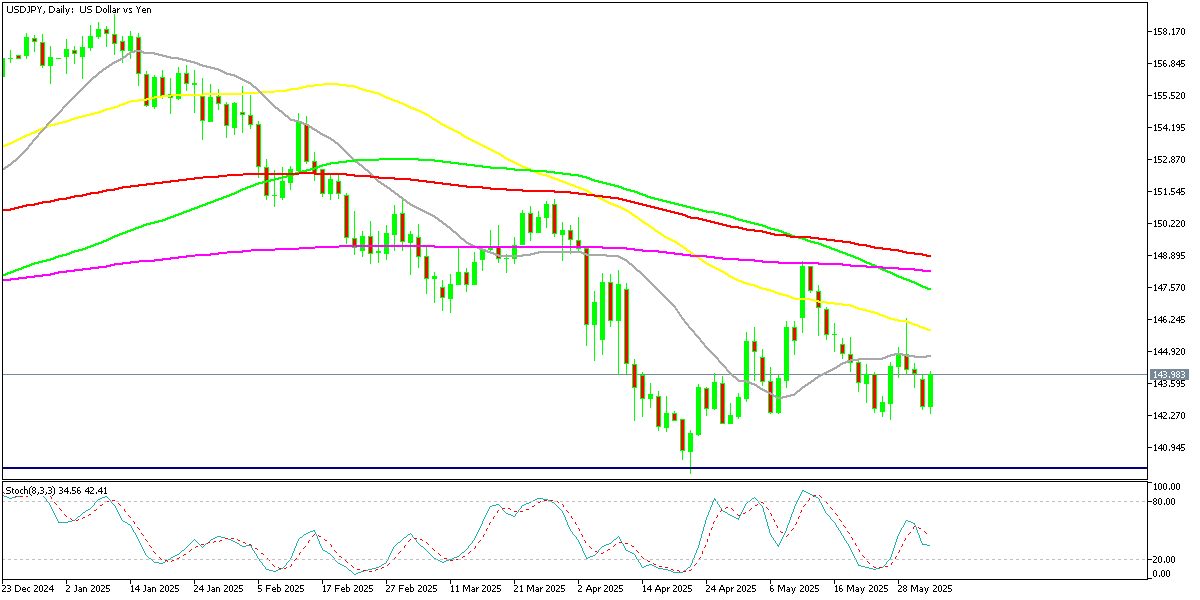

Yen Weakens, USD/JPY Returns to 144

Currency movements are also showing signs of deeper structural changes. The U.S. dollar strengthened against the Japanese yen, with USD/JPY rising from 143.40 to 144.31, even as U.S. Treasury yields declined. This counterintuitive move has been attributed to capital outflows from Japan and broader portfolio realignments, signaling that geopolitical dynamics and investor sentiment may be exerting more influence than traditional rate differentials.

USD/JPY – Daily Chart

Cryptocurrency Update

Bitcoin Finds Support at the 20 SMA

Digital assets are once again in focus. Bitcoin broke above the $110,000 threshold last week, rallying more than 6% over several sessions. The surge is being driven in part by rising concern over U.S. fiscal sustainability, ballooning national debt, and mounting geopolitical risks—all of which are reinforcing Bitcoin’s evolving role as a hedge against systemic uncertainty.

BTC/USD – Weekly chart

Ethereum Stuck MAs Again

Ethereum has also joined the rally, climbing over 20% from its April lows. The catalyst behind Ether’s resurgence is the successful launch of the Pectra upgrade, which improves wallet functionality and enhances staking mechanisms. These technical improvements have renewed enthusiasm for Ethereum among both institutional and retail investors, adding momentum to the broader crypto market.

ETH/USD – Weekly Chart

Skerdian Meta

Lead Analyst

Skerdian Meta Lead Analyst.

Skerdian is a professional Forex trader and a market analyst. He has been actively engaged in market analysis for the past 11 years. Before becoming our head analyst, Skerdian served as a trader and market analyst in Saxo Bank’s local branch, Aksioner. Skerdian specialized in experimenting with developing models and hands-on trading. Skerdian has a masters degree in finance and investment.

Related Articles

www.fxleaders.com