FX Week Forward Overview:The final week of February brings a broad however shallow financial calendar, prime heavy with ‘excessi

FX Week Forward Overview:

- The final week of February brings a broad however shallow financial calendar, prime heavy with ‘excessive’ rated occasions and never a lot else.

- The Reserve Financial institution of New Zealand meets for the primary time in 2021, and like the opposite commodity forex central banks, it too might shrug off unfavourable rate of interest discuss whereas on the similar time complain about FX markets.

- Adjustments in retail dealer positioning recommend that almost all USD-pairs are on blended footing.

Begins in:

Dwell now:

Mar 01

( 11:03 GMT )

Advisable by Christopher Vecchio, CFA

FX Week Forward: Technique for Main Occasion Danger

For the complete week forward, please go to the DailyFX Financial Calendar.

02/23 TUESDAY | 10:00 GMT | EUR Inflation Fee (JAN)

The last January Euroarea inflation price (CPI) report, the highest merchandise of curiosity for the Euro this week, is due out on Tuesday. Based on Bloomberg Information, the headline Euroarea inflation studying is due in at +0.9% from -0.3% (y/y), whereas the core studying is due in at +1.4% from +0.2% (y/y). The sharp rise might be attributed to the statistical base impact because of the coronavirus pandemic. With inflation expectations falling precipitously prior to now few weeks – since February 3, the 5y5y inflation swap forwards have declined by -9-bps from 1.383% to 1.296% – it looks like the European Central Financial institution, just like the Federal Reserve, will look previous any uptick in value pressures.

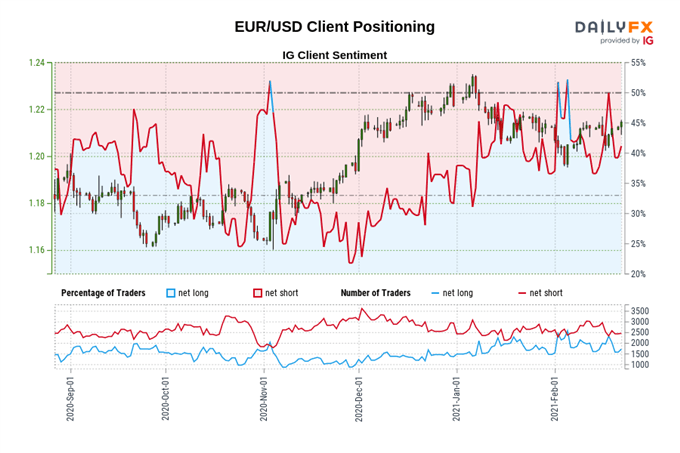

IG Shopper Sentiment Index: EUR/USD Fee Forecast (February 22, 2021) (Chart 1)

EUR/USD: Retail dealer knowledge reveals 41.83% of merchants are net-long with the ratio of merchants quick to lengthy at 1.39 to 1. The variety of merchants net-long is 21.99% greater than yesterday and 5.73% decrease from final week, whereas the variety of merchants net-short is 9.36% greater than yesterday and 12.27% decrease from final week.

We sometimes take a contrarian view to crowd sentiment, and the actual fact merchants are net-short suggests EUR/USD costs might proceed to rise.

But merchants are much less net-short than yesterday and in contrast with final week. Latest adjustments in sentiment warn that the present EUR/USD value development might quickly reverse decrease regardless of the actual fact merchants stay net-short.

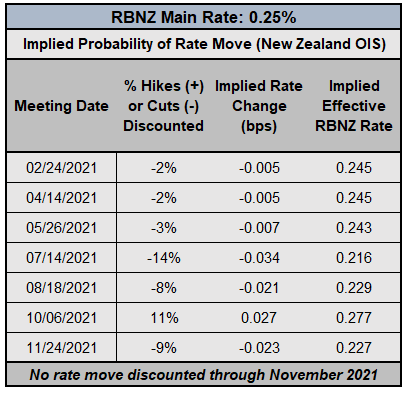

02/24 WEDNESDAY | 01:00 GMT | NZD Reserve Financial institution of New Zealand Fee Determination

The RBNZ will meet for the primary time this yr this week. Our finish of 2020 expectations for the RBNZ stays legitimate, because it was made with the understanding that policymakers wouldn’t be assembly till the final week of February 2021: “RBNZ Governor Adrian Orr has needed to rebuff a authorities request to incorporate housing costs within the formal coverage setting course of, which whereas seemingly benign, means that the economic system is experiencing a value bubble and thus wouldn’t be receptive to even decrease (e.g. unfavourable) rates of interest.”

RESERVE BANK OF NEW ZEALAND INTEREST RATE EXPECTATIONS (FEBRUARY 22, 2021) (Desk 1)

Accordingly, New Zealand in a single day index swaps (OIS) are discounting a 3% likelihood of a price reduce by mid-year, and a 9% likelihood total that rates of interest may dip to 0% by the final coverage assembly of the yr. The almost certainly state of affairs is that that the principle price will stay at its present stage into a minimum of February 2022. If something, the RBNZ is prone to comply with the trail set by its commodity forex central financial institution brethren, which has been to downplay discuss of unfavourable rates of interest whereas concurrently complaining about FX valuations.

02/25 THURSDAY | 12:00 GMT | MXN GDP Progress Fee (4Q’20)

The Mexican economic system is very reliant on its North American buying and selling companions, and surging coronavirus an infection charges in Canada and the USA crimped these economies, buying and selling exercise declined because the fourth quarter progressed (82% of Mexican exports go to Canada and the US, with the US accounting for 79% alone). However the knowledge obtained because the first launch don’t seem to have moved the needle: according to a Bloomberg Information survey, the Mexican economic system contracted by –4.5% (y/y) in 4Q’20, consistent with the prior replace. USD/MXN charges might shrug off the info as merchants pay extra consideration to the actions in US Treasury yields (which has underpinned the USD/MXN price rally).

02/25 THURSDAY | 13:30 GMT | USD Sturdy Items Orders (JAN)

The US economic system revolves round consumption tendencies, on condition that roughly 70% of GDP is accounted for by the spending habits of companies and customers. As such, the sturdy items orders reportmake for an vital barometer of the US economic system. Sturdy items are objects with lifespans of three-years or longer – from fridges and washing machines to automobiles and airplanes. This stuff typically require larger capital funding or financing to safe, that means that merchants can use the report as a proxy for enterprise’ and customers’ monetary confidence and well being. The preliminary January print is predicted to indicate a acquire of +1.1% after the +0.2% acquire in December. Just like the January US retail gross sales report, the January US sturdy items orders report might shock to the upside.

02/26 FRIDAY | 13:30 GMT | USD Inflation Fee (JAN)

The January US inflation price (PCE) report will probably be launched this Friday, and according to a Bloomberg Information survey, additional stabilization in value pressures is anticipated. Headline inflation (PCE) is due in at +1.3% (y/y) unchanged, whereas core inflation (Core PCE) is due in at +1.4% from +1.5% (y/y). The possible influence of a base impact may drive headline inflation greater to and thru +2% over the approaching months; regardless, the Fed appears content material to take a seat on its fingers for the foreseeable future.

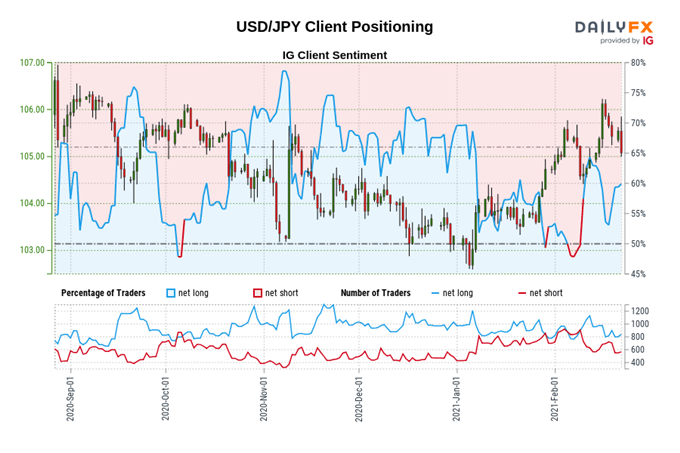

IG Shopper Sentiment Index: USD/JPY Fee Forecast (February 22, 2021) (Chart 2)

USD/JPY: Retail dealer knowledge reveals 59.02% of merchants are net-long with the ratio of merchants lengthy to quick at 1.44 to 1. The variety of merchants net-long is 7.04% greater than yesterday and 14.13% decrease from final week, whereas the variety of merchants net-short is 8.44% greater than yesterday and 6.93% decrease from final week.

We sometimes take a contrarian view to crowd sentiment, and the actual fact merchants are net-long suggests USD/JPY costs might proceed to fall.

But merchants are much less net-long than yesterday and in contrast with final week. Latest adjustments in sentiment warn that the present USD/JPY value development might quickly reverse greater regardless of the actual fact merchants stay net-long.

— Written by Christopher Vecchio, CFA, Senior Forex Strategist