S&P 500, HANG SENG, ASIA-PACIFIC MARKET OUTLOOK:

- US fairness indices commerce decrease on Monday, setting a bitter tone for the week forward

- Asia-Pacific shares are set for a pullback after registering robust good points in November

- The VIX volatility index rebounded from a nine-month low as sentiment soured

Asia-Pacific Shares Weekly Outlook:

Asia-Pacific shares look set to retrace from their current highs as revenue–taking ramped up on the final buying and selling day of the month. Shares within the area had been largely pushed by hopes for a quicker tempo of financial restoration with assistance from Covid-19 vaccines in addition to prospects for a gradual return of globalization underneath Biden’s presidency. The three main US indices are hovering close to their file highs, maybe taking a short pause earlier than making an attempt greater ranges. The VIX volatility index has fallen to its lowest stage seen since February earlier than bouncing again this morning.

Crude oil costs edged decrease as OPEC+ failed to succeed in an settlement to delay a manufacturing hike earlier than a proper assembly on Monday. Decrease oil costs additionally weighed on fairness market sentiment. The forex market is buying and selling blended, with haven-linked Swiss Franc and Japanese Yen rising alongside the risk-linked Australian and New Zealand {Dollars}, following the discharge of better-than-expected Chinese language NBS manufacturing PMI knowledge.

We’re most likely seeing mild on the finish of the tunnel, however the economic system is not out of the woods but in opposition to the backdrop of elevated unemployment charges, a bumpy street to restoration in addition to rising Chinese language company bond defaults. In addition to, the vaccines might not cease the virus from transmitting from one to a different, based on Moderna’s chief physician, which is including to uncertainties about pandemic management.

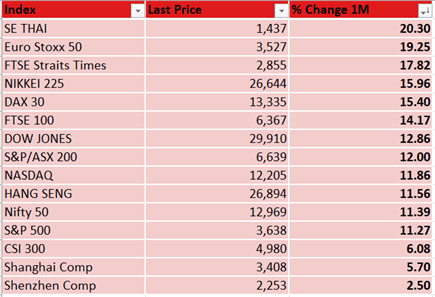

The month-to-month efficiency of main world indices is summarized beneath, which displays robust capital influx into Asia-Pacific and European shares in November. Mainland Chinese language shares had been lagging behind nevertheless after registering robust good points from March to September. A “catch-up” rally seems to be going down in markets that had been badly harm by the Covid-19 pandemic, like tourism-reliant Thailand for instance. This got here alongside a sectoral reshuffling in favor of cyclical sectors as buyers re-position for a post-Covid world.

Efficiency of Main World Indices – 1 Month

Supply: Bloomberg, DailyFX

Advisable by Margaret Yang, CFA

What’s the street forward for equities this quarter?

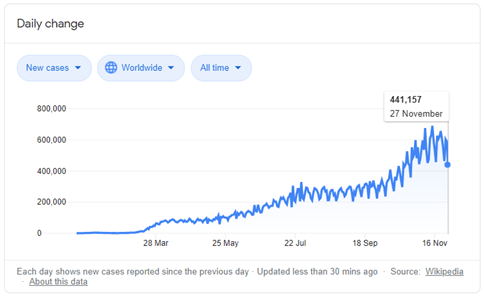

The pattern of Covid-19 circumstances globally has proven indicators of stabilizing (chart beneath), though the variety of every day new circumstances remains to be ranging at round half one million per day. The second main pandemic wave has to date had a a lot smaller influence on the monetary markets as in comparison with the primary wave seen in March-April. This is likely to be attributed to unprecedented stimulus around the globe, and that governments and enterprise homeowners are actually way more skilled in dealing with the pandemic state of affairs.

World Every day New Covid-19 Circumstances

Supply: Bloomberg

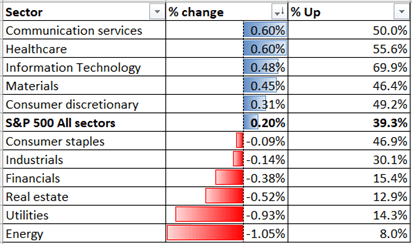

Sector-wise, buying and selling was fairly blended on Friday, with 39.3% of the index’s constituents ending greater. Communication providers (+0.60%), healthcare (+0.60%) and knowledge know-how (+0.48%) had been among the many greatest performers, whereas vitality (-1.05%), utilities (-0.93%) and actual property (-0.52%) had been lagging behind.

S&P 500 Sector Efficiency 27-11-2020

Supply: Bloomberg, DailyFX

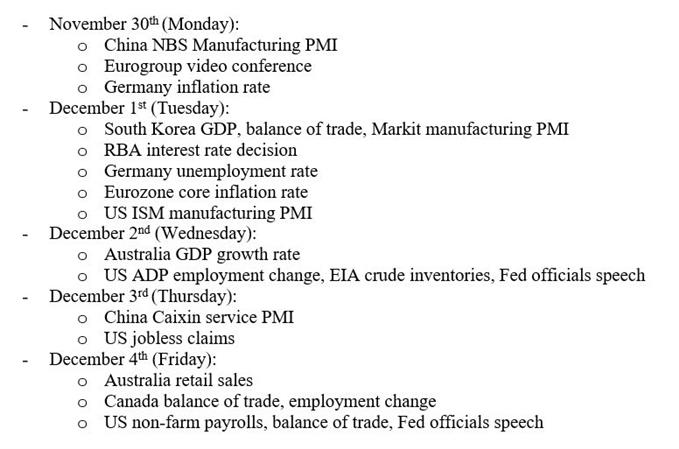

On the macro entrance, this Friday’s US non-farm payrolls knowledge and a number of other Fed officers’ speeches can be intently watched for any shift within the Fed’s coverage steerage. US ISM manufacturing PMI, ADP employment in addition to jobless claims knowledge are additionally extremely vital in assessing the influence of a second pandemic wave. For the week forward, listed here are the important thing market occasions:

Advisable by Margaret Yang, CFA

What does it take to commerce round knowledge?

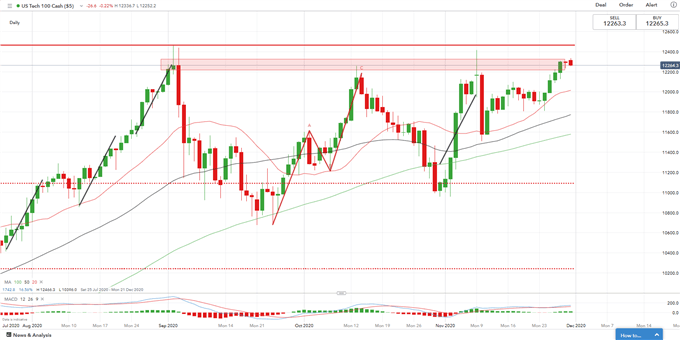

Technically, the Nasdaq 100 index seems to be hitting a resistance zone between 12,220-12,320 after failing three makes an attempt since September (chart beneath). Piercing by means of this resistance zone might open the door for additional upside potential in the direction of 12,460. The general pattern seems to be bullish-biased, as prompt by its 20-, 50- and 100-Day Easy Transferring Common (SMA) traces. A pullback from right here might result in additional consolidation at round 12,000.

Nasdaq 100 Index – Every day Chart

Hold Seng Index Outlook:

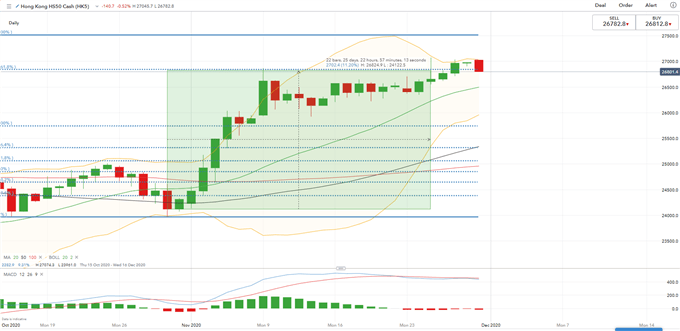

The Hold Seng Index (HSI) seems to be set to open decisively decrease immediately, getting into one other technical correction after pulling again from a current excessive of 27,000. Rapid resistance ranges could be discovered at 27,000 adopted by 27,520 – the 200% Fibonacci extension. The general pattern stays bullish-biased, as prompt by the upward-sloped Easy Transferring Averages (SMAs). The MACD indicator has doubtless diverged with value motion just lately, nevertheless, suggesting a short-term correction is feasible.

Hold Seng Index – Every day Chart

ASX 200 Index Outlook:

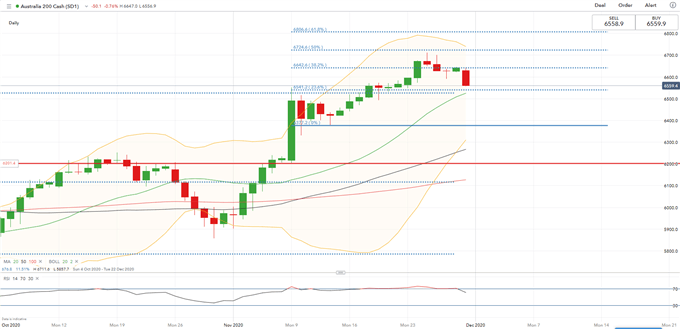

The ASX 200 index entered a short correction final week because the RSI indicator pierced into overbought territory. The general bullish pattern stays intact although, as prompt by upward-sloped SMAs and the breaking of a number of resistance ranges. Rapid resistance could be discovered at 6,720 – the 50.0% Fibonacci extension.

ASX 200 Index – Every day Chart

Advisable by Margaret Yang, CFA

Don’t give into despair, make a recreation plan

— Written by Margaret Yang, Strategist for DailyFX.com

To contact Margaret, use the Feedback part beneath or @margaretyjy on Twitter