Dear Editor,Following the announcement of the US tariff prospectively applicable to Guyana—and the foreign exchange (forex) intervention in the market

Dear Editor,

Following the announcement of the US tariff prospectively applicable to Guyana—and the foreign exchange (forex) intervention in the market by the Bank of Guyana (BoG), there has been a slew of letters in the mainstream media on the subject.

Reference is accordingly made to the following contributions: “It’s the real exchange rate that matters”, by Thomas B. Singh (Stabroek News edition dated April 9, 2025) … Singh contends that the injection of US$135 million into the market has raised eyebrows, intimating that this continued injection will erode the central bank’s forex reserves, and he questions why the domestic currency has not strengthened given the high inflows of petroleum revenues. Singh’s essay on the subject was notionally and theoretically correct in terms of the questions raised therein but was disappointingly lacking in a pragmatic empirical analysis to answer the very questions raised.

“Assessing Guyana’s real exchange rate may depend on how accurately its inflation data captures actual price fluctuations”, by Terrence Yhip (Stabroek News edition dated April 11, 2025) … Yhip endorses Thomas Singh’s contribution on the subject as summarized at number (1) above and has proceeded to draw reference to other case examples regionally for Guyana to pay attention to. Disappointingly, again, like Singh, Yhip did not perform any pragmatic empirical analysis on the subject in the case of Guyana.

“A drop in the value of the Guyana dollar”, by Jamil Changlee (Stabroek News edition of April 11, 2025) … The author contends that “the poor management of the tariffs during the current trade war has resulted in a drop in the value of the Guyanese dollar…”. Similar to the previous two essays highlighted above, Changlee failed to perform any empirical analysis to substantiate his assertion. Contrary to his view, there is no evidence at this point in time to suggest that the tariff was badly managed leading to a drop in the value of the domestic currency. In fact, the latest position on the tariff is that it is on pause for 90 days whereby during this period, a universal 10% baseline tariff shall apply to all countries trading with the US, and that includes Guyana. Therefore, this issue cannot be the causation of the depreciation / appreciation of the currency at this time.

It is worthwhile to note, in response to Thomas Singh’s notional argument that the US$135 million injection of forex by the BoG into the market that raised eyebrows, this form of intervention in the forex market is a normal operation by the central bank in the conduct of its monetary operations in keeping with the bank’s monetary policy targets as it relates to price stability (exchange rate stability). Hence, there is nothing unusual about this practice and/or the sum being injected relative to the size of the economy.

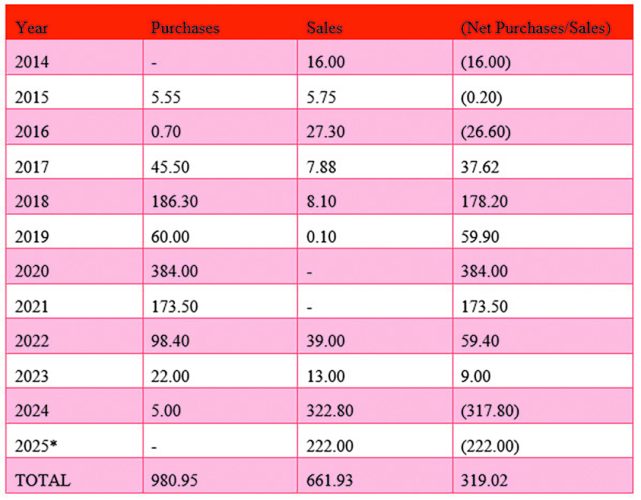

Table 1. Bank of Guyana Foreign Exchange Intervention (US$ Millions)

2025* (Jan-Feb data): Source: Author’s based on Bank of Guyana Statistical Abstracts

As shown in table (1), the BoG recorded a cumulative net purchase position with the commercial banks of US$319.02 million between 2014-2025*. Total purchases from commercial banks for this period, which represents excess forex in the system, amounted to US$980.95 million, while total sales amounted to US$661.93 million. In 2024, a net sales position of US$317.8 million was recorded and as of February, 2025, a net sales position of US$222 million to the commercial banks was observed.

Moreover, as depicted in chart (1), these forex interventions, more so the sales and net sales/purchases position by the BoG for the years under review accounted for ≤1% of GDP. Thus, from this standpoint, the recent injection of US$135 million into the market is not an unusually significant sum that would warrant any form of “eyebrow raising” or cause for concern. Conversely, the BoG has recorded purchases from the market for the years 2018, 2020, and 2021, which accounted for ≤5% of GDP.

In other words, over the last ten (10) years (2014-2024), the Bank of Guyana has mopped up more excess forex from the market (≈US$1b) than it has injected into the market (≈US$0.7b).

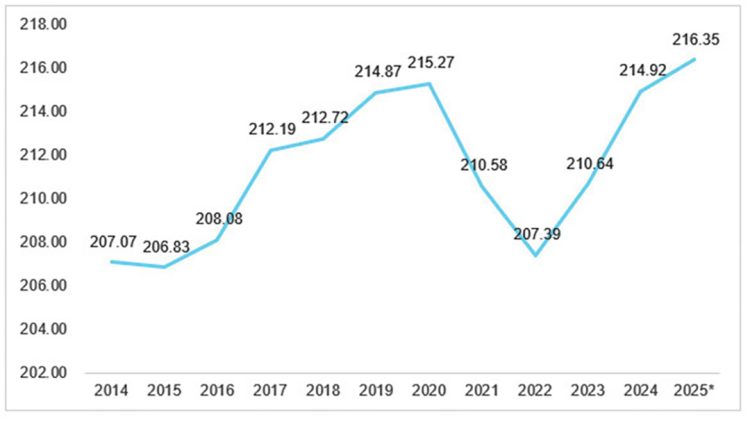

Chart 1: Annual Average Market Rate (Mid-Rate) has fluctuated within an acceptably flexible bandwidth of ±4%.

2025* (Jan-Feb data): Source: Author’s based on Bank of Guyana Statistical Abstracts

The exchange rate against the US dollar has remained relatively stable during the period under review (2014-2025*), fluctuating within an acceptable, flexible bandwidth of ±4%, using the Bank of Guyana average exchange rate as the central rate as the basis to calculate the bandwidth. With the US$135 million injection of forex made in April, 2025, which was not captured in the data reflected in chart (1), it is anticipated that the average exchange rate would have lowered from $216.35 observed in February 2025.

Of note, there are some countries, according to the IMF’s database, with flexible monetary policy frameworks that have exchange rate bandwidths as high as ±7% – ±12%.

Interestingly, the case was made for a more flexible exchange rate regime, vis-à-vis, an International Monetary Fund’s (IMF’s) working paper authored by Rina Bhattacharya, titled “Managing Guyana’s Oil Wealth: Monetary and Exchange Rate Policy Considerations”. The paper notes that the choice of an appropriate monetary policy framework and exchange rate regime serves to meet two key policy objectives: output stabilization/absorption of external shocks, and control of inflation (price stability).

As a general rule of thumb, central banks are required to maintain FX reserves covering a minimum of 3 months’ import cover, within which the macroeconomic stability framework is anchored. In this respect, the Total Net Foreign Sector Assets (TNFSA) exceeds the minimum threshold of 3 months import cover. The total net foreign sector assets and reserves, which stood at US$916 million in 2019, rose to US$4.6 billion at the end of 2024 and US$4.7 billion as of the end of February, 2025.

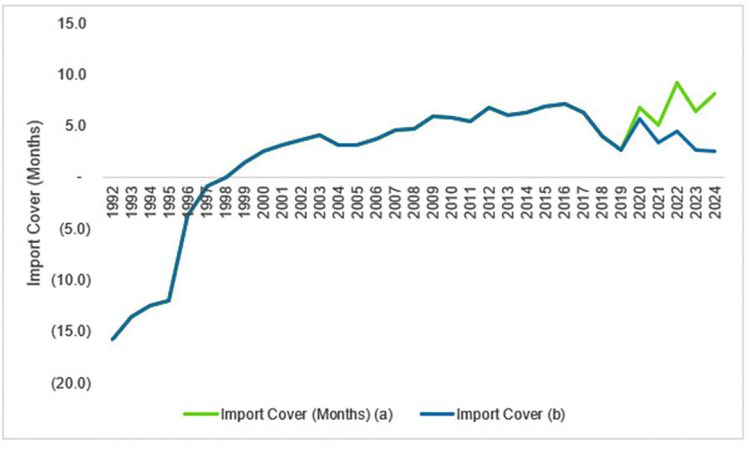

Chart 2 illustrates that in 1999, the FX reserves represented 1.4 months import cover, which rose to >3 months import cover in 2001 through 2018. The highest import cover recorded during that period was 7 months in 2016. In 2019, the import cover (a) fell to 3 months, which rose to ≥5 months during the period 2020-2024, to a record high of 9.2 months in 2022 and 8.1 months in 2024. Import cover (b), which excludes the NRF balance, averaged 3.6 months annually (2019-2024).

Chart 2: Import Cover (a) is calculated based on the Total Net Foreign Sector Assets (TNFSA), which include the Banking Sector Net Foreign Sector Assets & Reserves + the NRF Closing balance, whereas (b) excludes the NRF closing balance.

Source: Author’s based on Bank of Guyana Statistical Abstracts

Having considered all of the foregoing empirical evidence, the exchange rate against the US dollar has remained relatively stable during the period under review (2014-2025*), fluctuating within an acceptable, flexible bandwidth of ±4%. And finally, the Bank of Guyana’s foreign exchange intervention into the market is a normal operation in the conduct of the bank’s monetary operations in keeping with its monetary policy targets as it relates to price stability (exchange rate stability).

Sincerely,

Joel Bhagwandin

www.stabroeknews.com