HOW TO TRADE GEOPOLITICAL RISKS, JAPANESE YEN, US DOLLAR, EURO, BRAZILIAN REAL, INDIAN RUPEE, 2016 ELECTION – TALKING POINTSThe w

HOW TO TRADE GEOPOLITICAL RISKS, JAPANESE YEN, US DOLLAR, EURO, BRAZILIAN REAL, INDIAN RUPEE, 2016 ELECTION – TALKING POINTS

- The worldwide financial system is displaying rising weak spot and fragility

- Eroding financial fortitude exposes markets to geopolitical dangers

- Examples of political threats in Asia, Latin America and Europe

See our free information to learn to use financial information in your buying and selling technique!

ANALYZING GEOPOLITICAL RISKS

In opposition to the backdrop of eroding fundamentals, markets change into more and more delicate to political dangers as their capability for inducing market-wide volatility is amplified. When liberal-oriented ideologies – that’s, these favoring free commerce and built-in capital markets – are being assaulted on a world scale by nationalist and populist actions, uncertainty-driven volatility is the frequent consequence.

What makes political danger so harmful and elusive is the restricted skill buyers have for pricing it in. Merchants could subsequently discover themselves scorching below the collar as the worldwide political panorama continues to develop unpredictably. Moreover, very similar to the unfold of the coronavirus in 2020, political pathogens can have an analogous contagion impact.

Usually talking, markets do not likely care about political categorizations however are extra involved with the financial insurance policies embedded within the agenda of whoever holds the reigns of the sovereign. Insurance policies that stimulate financial progress sometimes act as a magnet for buyers trying to park capital the place it’s going to garner the best yield.

These embrace the implementation of fiscal stimulus plans, fortifying property rights, permitting for items and capital to stream freely and dissolving growth-sapping rules. If these insurance policies create satisfactory inflationary strain, the central financial institution could elevate rates of interest in response. That reinforces the underlying return on native property, reeling in buyers and lifting the foreign money.

Conversely, a authorities whose underlying ideological predilections go towards the gradient of globalization could trigger capital flight. Regimes that search to tear out the threads which have sown financial and political integration normally create a moat of uncertainty that buyers don’t wish to traverse. Themes of ultra-nationalism, protectionism and populism have been steadily proven to have market-disrupting results.

If a state undergoes an ideological realignment,merchants will assess the state of affairs to see if it radically alters their risk-reward arrange. If that’s the case, they might then reallocate their capital and re-formulate their buying and selling methods to tilt the stability of danger to reward of their favor. Volatility is stoked in doing so nonetheless as reformulated buying and selling methods are mirrored within the market-wide redistribution of capital throughout numerous property.

Open a Free Foreign exchange Demo account with IG and commerce currencies that transfer with politics and elections.

EUROPE: EUROSCEPTIC POPULISM IN ITALY

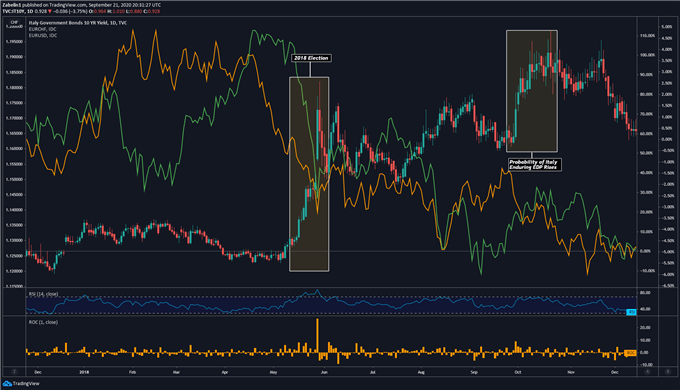

In Italy, the 2018 election roiled regional markets and finally rippled via nearly your complete monetary system. The ascendancy of the anti-establishment right-wing Lega Nord and ideologically-ambivalent 5 Star Motion was based on a marketing campaign of populism with a built-in rejection of the established order. The uncertainty accompanying this new regime was then promptly priced in and resulted in considerably volatility.

The chance premium for holding Italy’s property rose and was mirrored in an over-100 p.c spike in Italian 10-year bond yields. That confirmed buyers demanding the next return for tolerating what they perceived to be the next degree of danger. This was additionally mirrored within the dramatic widening of the unfold on credit score default swaps on Italian sovereign debt amid elevated fears that Italy may very well be the epicenter of one other EU debt disaster.

EUR/USD, EUR/CHF Plummeted as Mediterranean Sovereign Bond Yields Spiked Amid Fears of One other Eurozone Debt Disaster

Supply: TradingView

The US Greenback, Japanese Yen and Swiss Franc all gained on the expense of the Euro as buyers redirected their capital to anti-risk property. The Euro’s struggling was extended by a dispute between Rome and Brussels over the previous’s budgetary ambitions. The federal government’s fiscal exceptionalism was a characteristic of their anti-establishment nature that in flip launched larger uncertainty and was then mirrored in a weaker Euro.

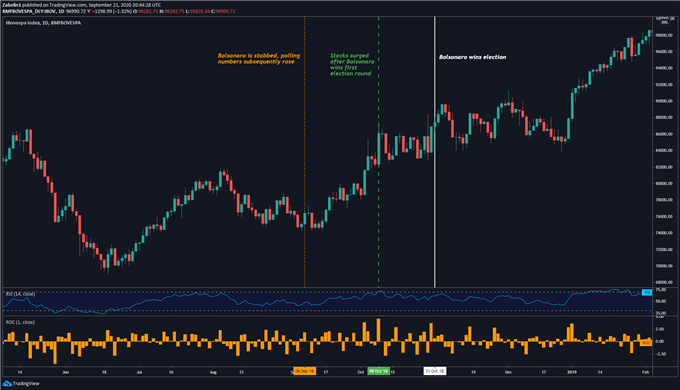

LATIN AMERICA: Nationalist-Populism in Brazil

Whereas President Jair Bolsonaro is usually characterised as a fire-brand nationalist with populist underpinnings, the market response to his ascendency was met with open arms by buyers. His appointment of Paulo Guedes – a College of Chicago-trained economist with a penchant for privatization and regulatory restructuring – boosted sentiment and buyers’ confidence in Brazilian property.

Ibovespa Index – Day by day Chart

Supply: TradingView

From June 2018 to the Covid-19 international markets rout in early 2020, the benchmark Ibovespa fairness index rose over 58 p.c in contrast with somewhat over 17 p.c within the S&P 500 over the identical time interval. Throughout the election in October, the Brazilian index rose over 12 p.c in simply one month as polls revealed that Bolsonaro was going to conquer his left-wing opponent Fernando Haddad.

Since Bolsonaro’s ascent to the presidency, the ups and downs in Brazilian markets have mirrored the extent of progress on his market-disrupting pension reforms. Buyers speculated that these structural changes will likely be sturdy sufficient to drag Brazil’s financial system away from the precipice of a recession and towards a powerful progress trajectory, unburdened by unsustainable public spending.

ASIA: Hindu Nationalism in India

The re-election of Prime Minister Narendra Modi was broadly welcome by markets, although lingering considerations had been raised in regards to the impact of Hindu nationalism on regional stability. Nevertheless, Modi has a fame for being a business-friendly politician. His election lured buyers into allocating a major quantity of capital to Indian property.

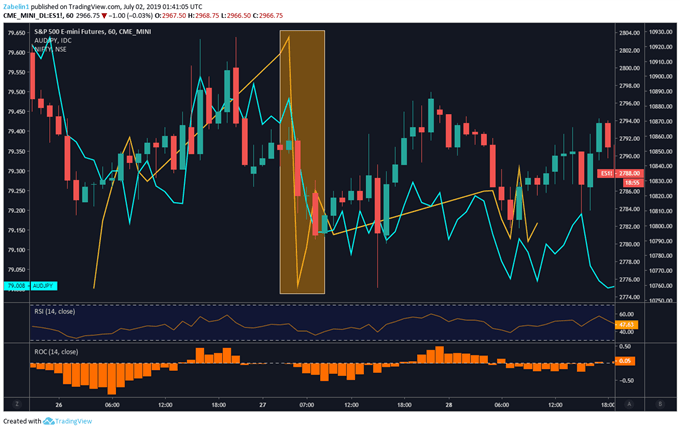

Nevertheless, buyers’ optimistic outlook is periodically undermined by periodic clashes between India and its neighbors over territorial disputes. Within the first breaths of 2019, India-Pakistan relations soured drastically amid a skirmish over the disputed Kashmir area. For the reason that 1947 partition, the hostility between the 2 nuclear powers has been an ever-present regional danger.

India Nifty 50 Index, S&P 500 Futures, AUD/JPY Fall After Information Broke of India-Pakistan Skirmish

Supply: TradingView

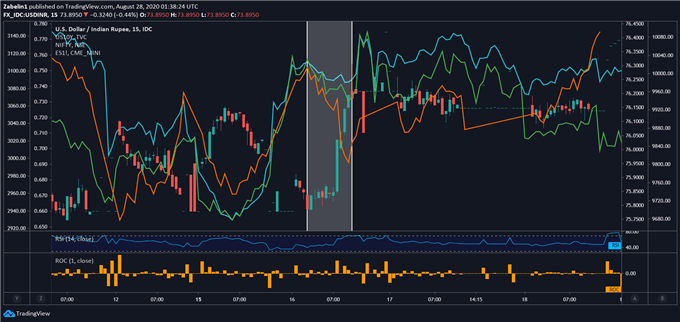

Rigidity between India and China, notably over the disputed border referred to as the Line of Precise Management (LAC) within the Himalayan Mountains additionally rattled Asian monetary markets. In June 2020, information of a skirmish between Chinese language and Indian troops leading to over 20 deaths raised considerations about what additional escalation may imply for regional safety and monetary stability. Learn the complete report right here.

India Nifty 50 Index, S&P 500 Futures, US 10-12 months Treasury Yield, USD/INR After Information Broke of India-China Skirmish

Supply: TradingView

Nationalist campaigns and governments are embedded with political danger as a result of the very nature of such a regime depends on displaying power and steadily equates compromise with capitulation. In occasions of political volatility and financial fragility, the monetary impression of a diplomatic breakdown is amplified by the truth that a decision to a dispute will doubtless be extended because of the inherently cussed nature of nationalist regimes.

US President Donald Trump and Modi employed an analogous model of sturdy rhetoric each on the marketing campaign path and inside their respective administrations. In a slightly ironic means, their ideological similarity could in truth be a drive that causes a rift in diplomatic relations. Tensions between the 2 have escalated in 2019, with markets worrying that Washington could begin one other commerce conflict in Asia, opening a second entrance in India having already engaged China.

HOW FX REACTS AS GOVERNMENTS, CENTRAL BANKS RESPOND TO GEOPOLITICAL & ECONOMIC STRESS

For economies with a excessive diploma of capital mobility, there are basically 4 completely different units of coverage-mix options that may provoke a response in FX markets following an financial or geopolitical shock:

- Situation 1: Fiscal coverage is already expansionary + financial coverage turns into extra restrictive (“tightening”) = Bullish for the native foreign money

- Situation 2: Fiscal coverage is already restrictive + financial coverage turns into extra expansionary (“loosening”) = Bearish for the native foreign money

- Situation 3: Financial coverage already expansionary (“loosening”) + fiscal coverage turns into extra restrictive = Bearish for the native foreign money

- Situation 4: Financial coverage is already restrictive (“tightening”) + fiscal coverage turns into extra expansionary = Bullish for the native foreign money

You will need to word that for an financial system like the US and a foreign money just like the US Greenback, every time fiscal coverage and financial coverage begin trending in the identical course, there’s typically an ambiguous impression on the foreign money. Beneath we are going to study how numerous fiscal and financial coverage treatments for geopolitical and financial shocks impression foreign money markets.

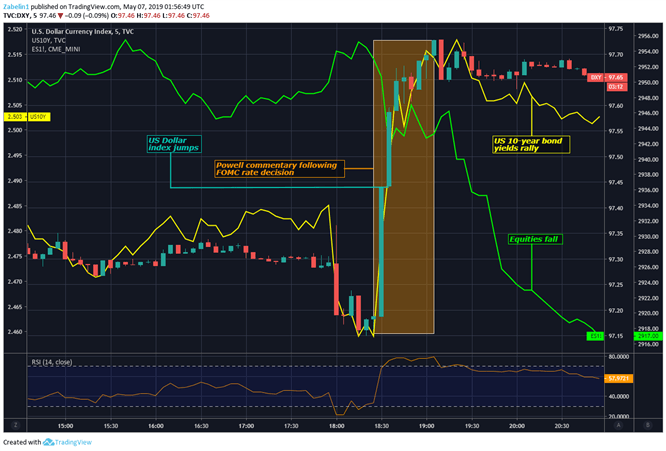

Situation 1 – FISCAL POLICY LOOSE; MONETARY POLICY BECOMES TIGHTER

On Could 2, 2019 – following the FOMC choice to carry charges in the two.25-2.50 p.c vary – Fed Chair Jerome Powell stated that comparatively tender inflationary strain famous on the time was “transitory”. The implication right here was that whereas worth progress was beneath what central financial institution officers had been hoping for, it might quickly speed up.The US-China commerce conflict performed a job in slowing financial exercise and muting inflation.

The implicit message was then a diminished likelihood of a charge reduce within the close to time period, on condition that the basic outlook was judged to be strong and the general trajectory of US financial exercise seen to be on a wholesome path. The impartial tone struck by the Fed was comparatively much less dovish than what markets had anticipated. This would possibly then clarify why the priced-in likelihood of a Fed charge reduce by the tip of the yr (as seen in in a single day index swaps) fell from 67.2 p.c to 50.9 p.c after Powell’s feedback.

In the meantime, the Congressional Funds Office (CBO) forecasted a rise within the fiscal deficit over a three–yr time horizon, overlapping the central financial institution’s would-be tightening cycle. What’s extra, this came towards the backdrop of hypothesis a couple of bipartisan fiscal stimulus plan. In late April, key policymakers introduced plans for a US$2 trillion infrastructure constructing program.

Really helpful by Dimitri Zabelin

Enhance your buying and selling with IG Consumer Sentiment Information

The mix of expansionary fiscal coverage and financial tightening made the case for a bullish US Greenbackoutlook. The fiscal package deal was anticipated to create jobs and increase inflation, thereby nudging the Fed to boost charges. Because it occurred, the Dollar added 6.2 p.c towards a mean of its main foreign money counterparts over the following 4 months.

Situation 1: DXY, 10-12 months Bond Yields Rise, S&P500 Futures Fall

Supply: TradingView

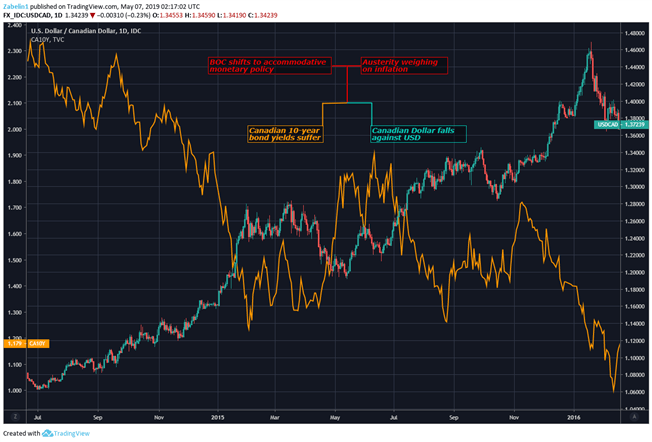

Situation 2 – FISCAL POLICY TIGHT; MONETARY POLICY BECOMES LOOSER

Theinternational monetary disaster in 2008 and the Nice Recession that adopted rippled out worldwide and destabilized Mediterranean economies. This stoked worries about a region-wide sovereign debt disaster as bond yields in Italy, Spain and Greece climbed to alarming ranges. Mandated austerity measures had been imposed in some circumstances which helped create the idea for Eurosceptic populism that therefore hang-outed the area.

Buyers started to lose confidence within the skill of those governments to service their debt and demanded the next yield for incurring what seemed to be a rising danger of default. The Euro was in ache amid the chaos as doubtsemerged about its very existence within the occasion that the disaster compelled the unprecedented departure of a member state from the Eurozone.

In what is taken into account to be some of the well-known moments in monetary historical past, European Central Financial institution (ECB) President Mario Draghi delivered a speech in London on July 26, 2012 which many would come to see as a pivotal second that saved the single foreign money. He stated that the ECB is “able to do no matter it takes to protect the Euro. And consider me,” he added,“it is going to be sufficient.” This speech calmed European bond markets and helped deliver yields again down.

Really helpful by Dimitri Zabelin

Prime Buying and selling Classes

The ECB additionallycreated a bond-buying program referred to as OMT (for “Outright Financial Transactions”). It was aimed at lowering stress in sovereign debt markets, providing aid to distressed Eurozone governments. Whereas OMT was by no means used, its mere availability helped becalm jittery buyers.On the similar time, lots of the troubled Euro space states adopted austerity measures to stabilize authorities funds.

Whereas the Euro initially rose as worries about its collapse receded, the foreign money would depreciate considerably towards the US Greenback over the course of the next three years. By March 2015, it had misplaced over 13 p.c of its worth. When analyzing the financial and financial arrange, it turns into fairly clear why.

Situation 2: Euro Sighs Reduction – Sovereign Bond Yields Fall as Insolvency Fears are Quelled

Supply: TradingView

Austerity measures in lots of Eurozone international locations restricted their authoritiess’ skill to present fiscal stimulus that may need assisted create jobs and increase inflation. On the similar time, the central financial institution was easing coverage as a technique to alleviate the disaster. Consequently, this mixture pressured the Euro decrease towards most of its main counterparts.

Situation 2: Euro, Sovereign Bond Yields Fall

Supply: TradingView

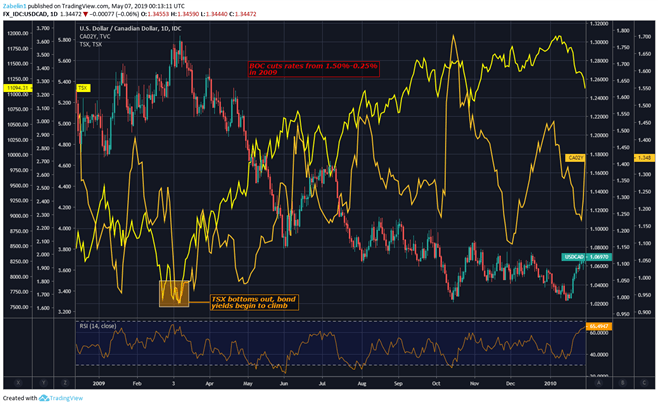

Situation 3 – MONETARY POLICY LOOSE; FISCAL POLICY BECOMES TIGHTER

On the early levels of the Nice Recession, the Financial institution of Canada (BOC) reduce its benchmark rate of interest from 1.50 to 0.25 p.c as a technique to ease credit score situations, restore confidence and revive financial progress. Counterintuitively, the yield on 10-year Canadian authorities bonds started to rise. This rally got here proper across the similar time as Canada’s benchmark TSX inventory index established a backside.

Situation 3: USD/CAD, TSX, Canadian 2-12 months Bond Yields

Supply: TradingView

The next restoration of confidence and restoration in share costs was mirrored inbuyers’ shifting desire for riskier, higher-returning investments (like shares)in lieu of comparatively safer options (like bonds). This reallocation of capital despatched yields greater regardless of the central financial institution’s financial easing. The BOC then started to boost its coverage curiosity charge anew and introduced it as much as 1p.c, the place it remained for the following 5 years.

Throughout this time, Prime Minister Stephen Harper carried out austerity measures to stabilize the federal government’s funds amid the international monetary disaster. The central financial institution then reversed course and reduce charges again to 0.50 p.c by July 2015.

Each CAD and native bond yields suffered as financial coverage was loosened whereas the capability for fiscal coverage assist was constrained. Because it occurs, reducing again authorities spending at this troublesome time ended up costing Mr Harper his job. Justin Trudeau replaced him as Prime Minister following a victory within the 2015 basic election.

Situation 3: USD/CAD, Canada 2-12 months Bond Yields

Supply: TradingView

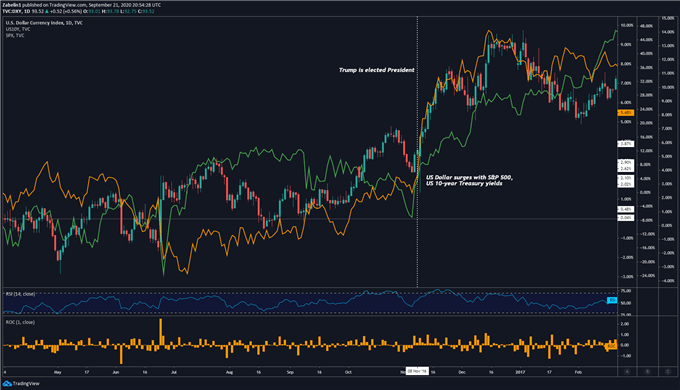

Situation 4 – MONETARY POLICY TIGHT; FISCAL POLICY BECOMES LOOSER

After Donald Trump was proclaimed the victor within the 2016 USpresidential election, the political panorama and financial backdrop favored a bullish outlook for the US Greenback. With the the Oval Workplace and each homes of Congress thus managed by the Republican Celebration, the markets appeared to conclude that scope for political volatility had been diminished.

This made the market-friendly fiscal measures proposed by candidate Trump through the electionseem extra more likely to be carried out. These included tax cuts, deregulation and infrastructure constructing. Buyers appeared to miss threats to launch commerce wars towards high buying and selling companions equivalent to China and the Eurozone, at the least for the time. On the financial aspect, central financial institution officers raised charges on the tail finish of 2016 and had been trying to hike once more by at the least 75 foundation factors via 2017.

With scope for fiscal enlargement and financial tightening in sight, the US Greenback rallied alongside native bond yields and equities. This got here as company earnings expectations strengthened alongside the outlook for broader financial efficiency. This stoked bets on firmer inflation and thereby on a hawkish response from the central financial institution.

Situation 4) US Greenback Index (DXY), S&P 500 Futures, 10-12 months Bond Yields (Chart 7)

Supply: TradingView

WHY POLITICAL RISKS MATTER FOR TRADING

Numerous research have proven {that a} important decline in residing requirements from conflict or a extreme recession improve the propensity for voters to take up radical positions on the political spectrum. As such, persons are extra more likely to deviate from market-friendly insurance policies – equivalent to capital integration and commerce liberalization – and as a substitute give attention to measures that flip away from globalization and are deleteriously inward-facing.

The trendy globalized financial system is interconnected each politically and economically and subsequently any systemic shock has a excessive likelihood of echoing out into the world. Throughout occasions of serious political volatility amid inter-continental ideological adjustments, it’s essential to observe these developments as a result of inside them are alternatives to arrange brief, medium and long-term buying and selling methods.

— Written by Dimitri Zabelin, Analyst for DailyFX.com

To contact Dimitri, use the feedback part beneath or @ZabelinDimitrion Twitter