US Greenback Outlook:US Treasury yields have been transferring sideways after the ‘taperless tantrum’ earlier within the 12 months, depriving the

US Greenback Outlook:

- US Treasury yields have been transferring sideways after the ‘taperless tantrum’ earlier within the 12 months, depriving the US Greenback of a wanted catalyst in latest weeks.

- Volumes throughout the Federal Reserve’s open markets desk counsel that extra liquidity is being drained from monetary markets. Is that this the beginning of the taper?

- In easy phrases, if the Fed makes use of repos to conduct its QE program, then reverse repos are the other – its tapering. However this time, it’s been a ‘tantrumless taper’.

‘To taper or to not taper? That’s the query!’ Or is it? Whereas there seems to be a nuanced, public debate occurring about whether or not or not the Federal Reserve ought to take away its stimulus and alongside what timeframe, it seems that the taper efforts have already begun.

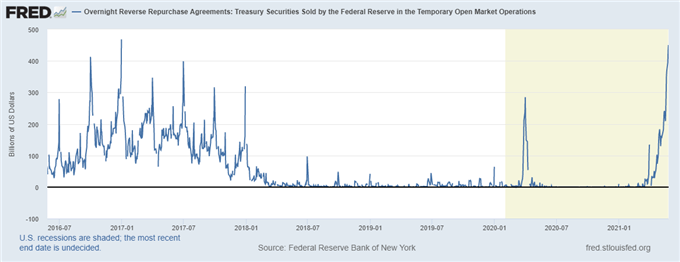

There’s been numerous chatter in latest days concerning the quantity of reverse repurchase agreements (RRP) on the Federal Reserve’s open market deck in latest days. In reality, simply yesterday, we noticed the best quantity of RRP on the Fed’s open market desk, simply north of $450 billion, since December 30, 2016 ($468.36 billion).

Even within the post-International Monetary Disaster period, these type of volumes are pretty uncommon contemplating it’s neither the final day of the month nor the final day of the quarter.

Ought to merchants be apprehensive? The reply may be each sure and no.

Federal Reserve In a single day Reverse Repurchase Agreements Chart (Might 2016 to Might 2021) (Chart 1)

What’s a Repo? What’s a Reverse Repo?

In easy phrases, the Fed’s open market desk conducts repo agreements to facilitate its QE program – so as to add liquidity to the system. Reverse repo agreements are the other of QE: the Fed is draining liquidity from the system.

Listed below are the technical definitions, per the New York Fed. “In a repo transaction, the Desk purchases Treasury, company debt, or company mortgage-backed securities (MBS) from a counterparty topic to an settlement to resell the securities at a later date…repo transactions briefly enhance the amount of reserve balances within the banking system.”

Reverse repos are the other: “In a reverse repo transaction…the Desk sells securities to a counterparty topic to an settlement to repurchase the securities at a later date at the next repurchase value. Reverse repo transactions briefly cut back the amount of reserve balances within the banking system.”

Perspective #1 – No Downside Right here

“Excessive reverse repo volumes? No drawback right here! As a easy heuristic, if the Fed makes use of repos to implement its QE program, thereby bringing liquidity to monetary markets, then excessive reverse repo volumes might be interpretated as a taper. And that’s factor! The system is well-capitalized, and excessive reverse repo volumes are proof that the US financial system has weathered the pandemic. This can be a function, not a bug, of the Fed’s pandemic period insurance policies, and must be anticipated as normalization comes. No belongings are mispriced.”

Perspective #2 – Trigger for Concern

“Excessive reverse repo volumes? That is trigger for concern! This implies prime brokers and sure different certified entities are flush with capital and want a spot to park it. The monetary system is drowning in liquidity – that is the explanation why commodities have been rallying so sharpy this 12 months. This liquidity has contributed to excessive inflation, which appears to be like greater than transitory. If we noticed a ‘taperless tantrum’ earlier this 12 months, now we’re seeing a ‘tantrumless taper’. US Treasury yields are mispriced and must be increased.”

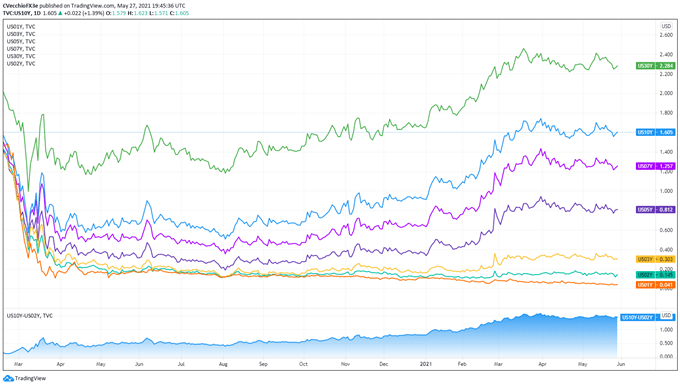

US Treasury Yield Curve (1-year to 30-years) (February 2020 to Might 2021) (Chart 2)

The Dealer’s Strategy

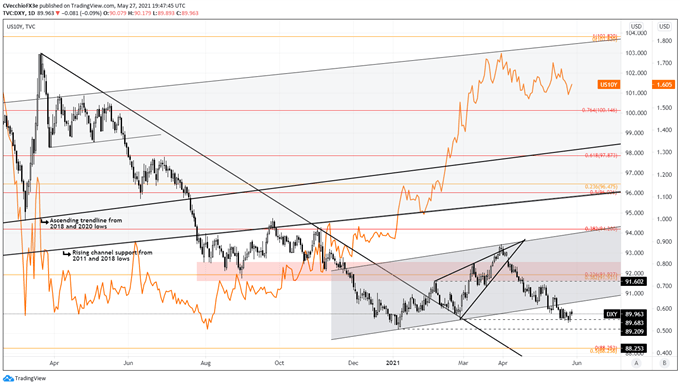

Contemplating varied Fed officers have been teasing a few timeline for taper discuss, the quantity of RRP is price monitoring heading into the June Fed assembly – however that’s about it. Monetary markets are barely reacting to the liquidity drain: the DXY Index is buying and selling on the identical ranges it was this time final week; the US Treasury 10-year yield has been bounding in the identical place for the previous two-months.

DXY PRICE INDEX TECHNICAL ANALYSIS: DAILY CHART (March 2020 to Might 2021) (CHART 3)

But when taper fears snowball, leading to a kick increased in US Treasury yields, we may enter an analogous buying and selling surroundings akin to March, when rising yields spooked fairness markets, serving to the US Greenback produce a counter-trend rally amidst long-term bearish technical issues.

— Written by Christopher Vecchio, CFA, Senior Forex Strategist

aspect contained in the

aspect. That is most likely not what you meant to do!nn Load your software’s JavaScript bundle contained in the aspect as an alternative.www.dailyfx.com