US Greenback Forecast Overview:The US Greenback (through the DXY Index) has rapidly exited its multi-month consolidation to the d

US Greenback Forecast Overview:

- The US Greenback (through the DXY Index) has rapidly exited its multi-month consolidation to the draw back, however USD/JPY has not traded decrease.

- Why? Protected haven currencies are being jettisoned as developed economies are shifting in direction of re-opening after the coronavirus pandemic. Positive aspects by fairness markets and weak spot in gold costs is hurting the Japanese Yen.

- Retail dealer positioning means that USD/JPY should commerce greater, though the opposite main USD-pairs have much less rosy outlooks.

Beneficial by Christopher Vecchio, CFA

Get Your Free USD Forecast

US Greenback Underneath Siege as Euro’s Issues Dissolve

As protests and riots unfold throughout america following the homicide of George Floyd, a wierd feeling has unfold throughout monetary markets: perhaps the worst of the coronavirus pandemic is behind us. It might be the case that, with throngs of individuals pouring into the streets – in stark contradiction to the dire stay-at-home lockdowns – america has ‘ripped off the band-aid,’ serving as real-life petri dish for re-opening.

So we’re now counting down the clock for 2 weeks’ time, the incubation interval for COVID-19, to see if new instances and hospitalizations begin to rise anew. And this can be the curious silver lining to the latest unrest in america, from the monetary markets’ perspective: if we don’t see a soar in new coronavirus instances by mid-June, then the hope for a V-shaped restoration will likely be in full throttle.

For the US Greenback (through the DXY Index), it’s simple to assign the latest protests and riots as the rationale for its latest slide. But the developments round its largest part, the Euro, would dictate a weaker DXY Index anyhow: the transfer in direction of fiscal union is a bonafide gamechanger.

The combo of Europe backing away from an existential disaster coupled with recent causes to hope that the coronavirus pandemic is subsiding has let to a surge in danger urge for food in latest days, sending buyers fleeing from protected haven property into greater yielding, riskier alternatives. To this finish, whereas currencies just like the Japanese Yen and US Greenback have suffered, others just like the Australian and Canadian {Dollars} have surged.

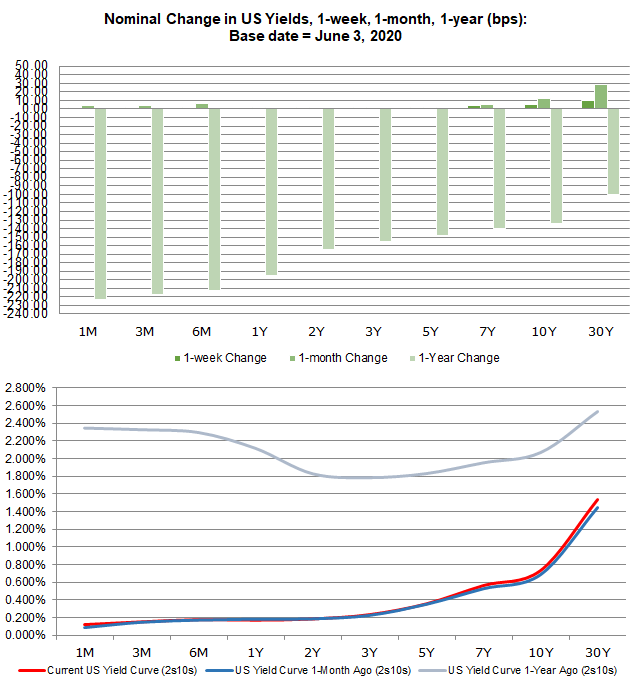

US Treasury Yield Curve Continues to Normalize

The US Treasury yield curve has certaintly normalized relative to the place it was in mid-March, little question because of the extraordinary coverage steps taken by the Federal Reserve. As we discovered from The Nice Recession, firms which can be dealing with liquidity points within the short-term can simply be swept up within the tides of insolvency if aggressive, heavy handed measures aren’t taken swiftly and upfront; the coverage response can’t be a sluggish drip. Thus, the normalization of the US Treasury yield curve is an intentional, if not synthetic final result.

US Treasury Yield Curve: 1-month to 30-years (June 3, 2020) (Chart 1)

That stated, there’s some slight twisting occuring on the short-end of the US yield curve, with the 1m12m unfold narrowing over the previous month. However the long-end of the yield curve is rising sooner than the short-end; this bear steepening is commonly an indication of extra optimistic tendencies on behalf of buyers. Contemplating we’re now within the dwell petri dish of re-opening in maybe essentially the most aggressive method attainable in america, buyers could also be positioning themselves for a sharper rebound in US development in Q3’20.

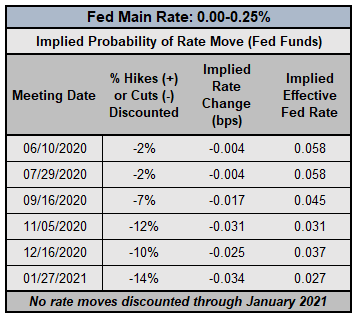

Fed Price Cuts Accomplished; New Measures Extra Possible

It nonetheless holds that, with the Federal Reserve already having enacted emergency rate of interest lower measures, fee markets are roughly caught in a state of suspended animation. If the Fed goes to do something from right here on out, it’s going to come back through extra QE, a repo facility, and so forth. The most recent extraordinary effort, the Municipal Liquidity Facility, is an instance of this effort, which has been expanded to cowl most metropolitan areas in america. Now, the Fed’s steadiness sheet is above $7 trillion.

Federal Reserve Curiosity Price Expectations (June 3, 2020) (Desk 1)

There’s been no indication that the Fed plans on shifting charges into destructive territory, and consequently, we’ve reached the decrease certain in the meanwhile. To this finish, any strategies by charges markets {that a} fee hike is coming anytime quickly is a pricing quirk to be ignored: rates of interest aren’t going anyplace greater, no less than by means of January 2021.

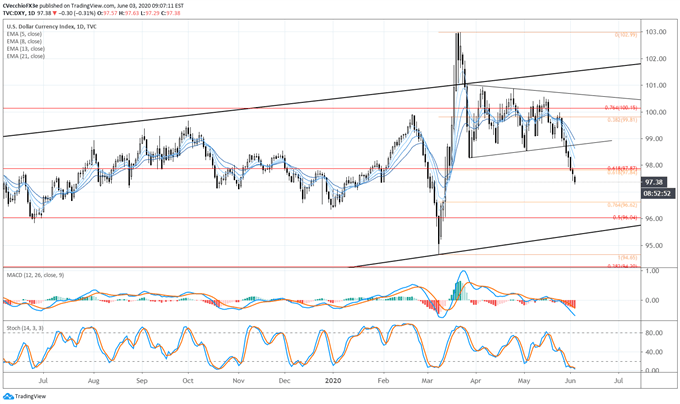

DXY PRICE INDEX TECHNICAL ANALYSIS: DAILY CHART (July 2019 to April 2020) (CHART 2)

The DXY Index’s lack of course in since late-March shaped right into a symmetrical triangle on the day by day timeframe, yielding a breakdown prior to now week. Through the breakdown, whereas the DXY Index has moved beneath the 61.8% retracement of the 2020 low/excessive vary, bearish momentum has accelerated considerably with worth now beneath the day by day 5-, 8-, 13-, and 21-EMA envelope. Every day MACD continues to say no whereas in bearish territory, whereas Sluggish Stochastics is holding in oversold territory. Extra losses seem seemingly within the near-term; the 76.4% retracement of the 2020 low/excessive vary is available in at 96.62.

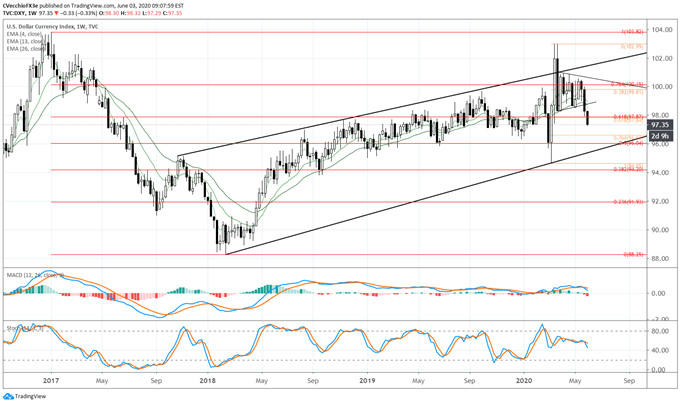

DXY PRICE INDEX TECHNICAL ANALYSIS: WEEKLY CHART (November 2016 to June 2020) (CHART 3)

A re-drawn weekly timeframe shifts our consideration from a possible bearish rising wedge from the 2018 low to a rising channel as a substitute, with help coming in on the March 2020 low. To this finish, the lack of the multi-month consolidation, in context of failure to climb by means of channel resistance, suggests {that a} deeper pullback in direction of channel help could also be within the works. Over the subsequent few weeks, merchants might look so far as the 50% retracement of the 2017 excessive/2018 low vary at 96.04 as important help.

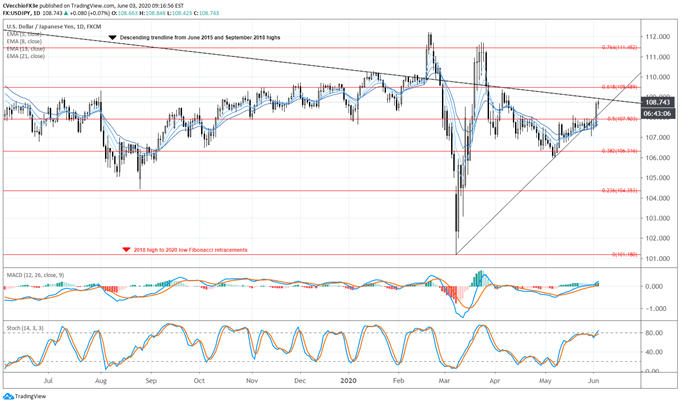

USD/JPY RATE TECHNICAL ANALYSIS: DAILY CHART (July 2019 to June 2020) (CHART 4)

USD/JPY’s features in latest days has seen the pair retake the rising trendline from the March and Could lows, in impact monitoring each the transfer greater by US fairness markets and the transfer decrease by gold costs. The swell in danger urge for food amid hopes that The Nice Lockdown has been sequestered to the historical past books has come on the detriment of each the US Greenback and the Japanese Yen.

The elemental context, with the Japanese financial system already in recession pre-coronavirus, there’s a robust likelihood that the Financial institution of Japan will likely be stepping up its easing efforts within the coming months, additional incentivizing merchants to cut back their holdings of the low yielding, protected haven foreign money.

To this finish, the momentum profile for USD/JPY charges is changing into extra bullish. USD/JPY charges are above the day by day 5-, 8-, 13-, and 21-EMA envelope, which has aligned in bullish sequential order. Every day MACD continues to glide above its sign line, whereas Sluggish Stochastics have risen into overbought territory. Positive aspects by means of 109.00 would see the descending trendline from the June 2015 and September 2018 highs damaged, a good improvement for USD/JPY bulls.

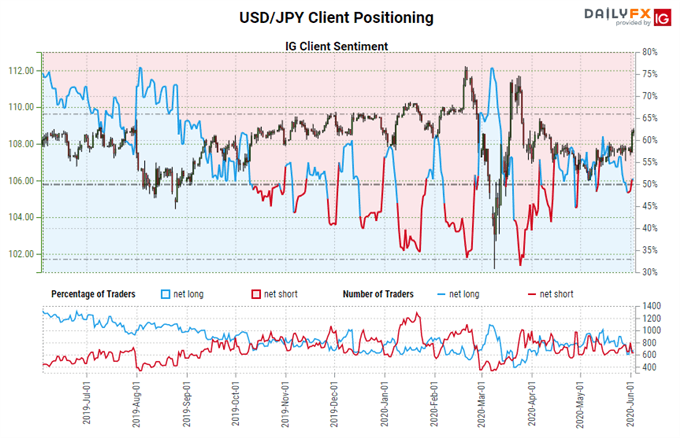

IG Shopper Sentiment Index: USD/JPY RATE Forecast (June 3, 2020) (Chart 5)

USD/JPY: Retail dealer knowledge exhibits 53.19% of merchants are net-long with the ratio of merchants lengthy to brief at 1.14 to 1. The variety of merchants net-long is 4.48% decrease than yesterday and 5.77% decrease from final week, whereas the variety of merchants net-short is 17.18% decrease than yesterday and 5.06% decrease from final week.

We sometimes take a contrarian view to crowd sentiment, and the very fact merchants are net-long suggests USD/JPY costs might proceed to fall.

Positioning is extra net-long than yesterday however much less net-long from final week. The mix of present sentiment and up to date adjustments provides us an extra combined USD/JPY buying and selling bias.

Beneficial by Christopher Vecchio, CFA

Traits of Profitable Merchants

— Written by Christopher Vecchio, CFA, Senior Forex Strategist