June Fed Assembly Preview:Forward of time, market contributors are performing as their typical pre-FOMC selves: there's a sturdy

June Fed Assembly Preview:

- Forward of time, market contributors are performing as their typical pre-FOMC selves: there’s a sturdy directional pull to the draw back for the US Greenback, whereas it’s in any other case pretty typical to see a drift in worth motion in the 24-hours main into the Fed assembly.

- Fed funds are pricing in an 2% probability of a 25-bps charge hike in June and a 12% probability of 25-bps charge reduce by the tip of the 12 months. As such, unfavourable rates of interest stay unlikely for now.

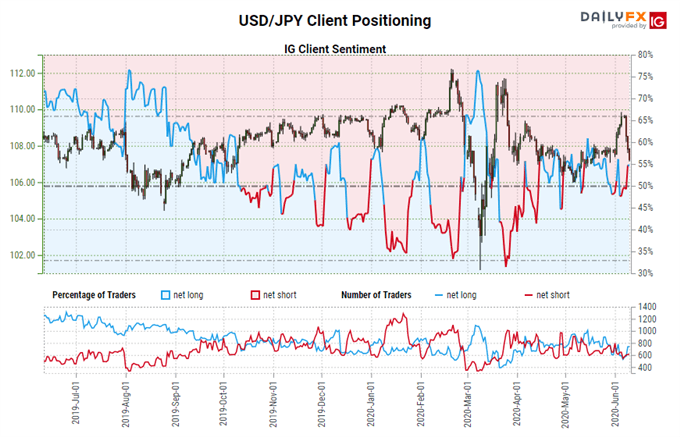

- Retail dealer positioningsuggests that the present USD/JPY worth development might proceed decrease.

Begins in:

Stay now:

Jun 15

( 11:06 GMT )

Beneficial by Christopher Vecchio, CFA

FX Week Forward: Technique for Main Occasion Danger

No Calm Earlier than the Storm

Market contributors are readying themselves for one more necessary Federal Reserve charge determination later right now. Forward of time, market contributors are performing as their typical pre-FOMC selves: there’s a sturdy directional pull to the draw back for the US Greenback, whereas it’s in any other case pretty typical to see a drift in worth motion within the 24-hours main into the Fed assembly.

The continued volatility in markets can partially be attributed to the voluminous circulate of financial headlines popping out of the USA, specifically, particular person states because it pertains to the re-opening from the coronavirus pandemic. And so whereas there was extra exercise in FX markets than regular, we nonetheless do anticipate that extra volatility is coming. And to this finish, there have been shifts in US Treasury yields and the US Greenback (by way of the DXY Index) as market contributors place themselves for the June Fed assembly.

US Treasury Yield Curve Inversion Slowly Abating

Whereas the US Treasury yield curve stays normalized on the very front-end – 1-month payments are now not yielding greater than their equivalents out to 2-year notes –this normalization is a direct end result the extraordinary coverage steps taken by the Federal Reserve.

In any case, as we realized from The Nice Recession, corporations which can be going through liquidity points within the short-term can simply be swept up within the tides of insolvency if aggressive, heavy handed measures are usually not taken swiftly and upfront; the coverage response can’t be a sluggish drip.

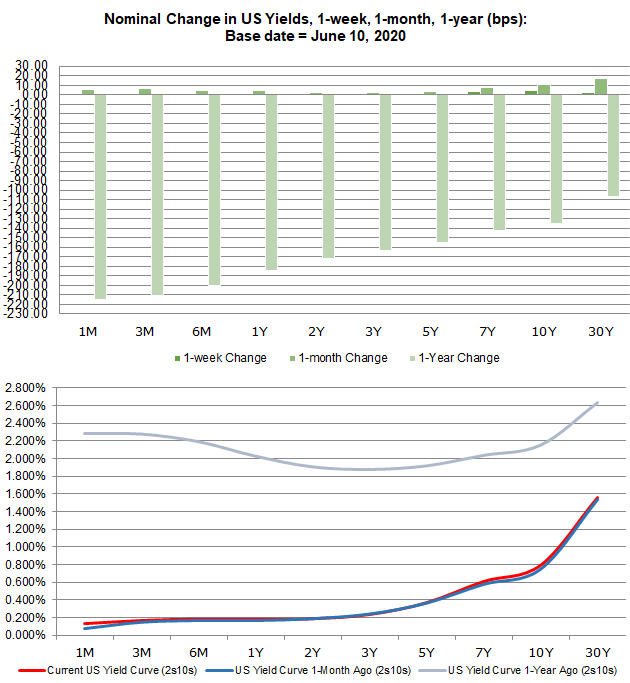

US Treasury Yield Curve: 1-month to 30-years (June 10, 2020) (Chart 1)

Markets are beginning to really feel that danger to the US economic system is rising once more: comparatively talking, 1-month to 12-month/1-year yields are increased right now than they have been one week in the past, as are 7-year, 10-year, and 30-year yields; but the stomach of the yield curve has fallen.

This twisting of the yield curve is hidden throughout the bear steepening, suggesting that there stays some discomfort amongst buyers even supposing shares have rocketed in current weeks. For all the thrill in fairness markets over the previous month, credit score remains to be suggesting that we’re not out of the woods simply but. And that’s what the Federal Reserve will conclude as nicely.

The Fed Fee Lower Cycle Not What It As soon as Was

It nonetheless holds that, with the Federal Reserve already having enacted emergency rate of interest reduce measures, charge markets are roughly caught in a state of suspended animation. If the Fed goes to do something from right here on out, it’s going to return by way of extra QE, a repo facility, and so on. The most recent extraordinary effort, the Municipal Liquidity Facility, is an instance of this effort.

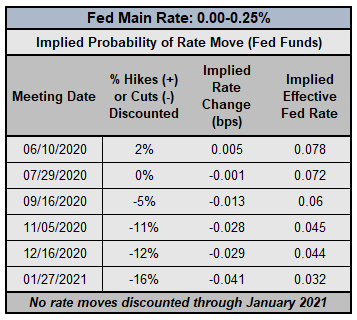

Federal Reserve Curiosity Fee Expectations (June 10, 2020) (Desk 1)

There’s been no indication that the Fed plans on transferring charges into unfavourable territory, and in consequence, we’ve reached the decrease sure in the intervening time. To this finish, any ideas by charges markets {that a} charge hike is coming anytime quickly is a pricing quirk to be ignored: rates of interest are usually not going anyplace increased, a minimum of by way of January 2021.

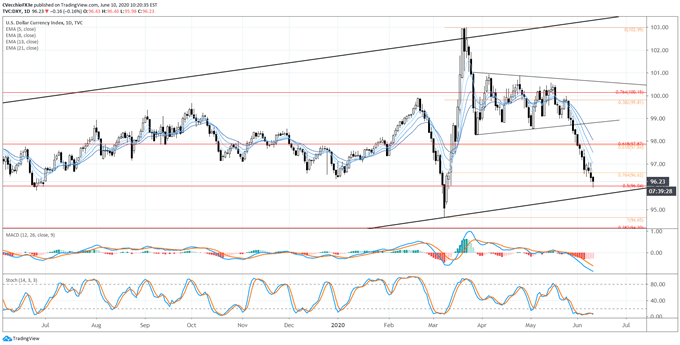

DXY PRICE INDEX TECHNICAL ANALYSIS: DAILY CHART (July 2019 to June 2020) (CHART 2)

The DXY Index’s lack of path in since late-March fashioned right into a symmetrical triangle on the every day timeframe, yielding a breakdown initially of June. Within the final US Greenback replace, it was famous that “extra losses seem probably within the near-term; the 76.4% retracement of the 2020 low/excessive vary is available in at 96.62.” In the course of the breakdown, whereas the DXY Index has moved under the 76.4% retracement of the 2020 low/excessive vary, falling under because the 50% retracement of the 2017 excessive/2018 low vary at 96.94. Bearish momentum has accelerated considerably, with worth remaining under the every day 5-, 8-, 13-, and 21-EMA envelope. Day by day MACD continues to say no whereas in bearish territory, whereas Sluggish Stochastics is holding in oversold territory. Extra losses can’t be dominated out, significantly if the rising trendline from the February 2018 and March 2020 lows is damaged under 95.80.

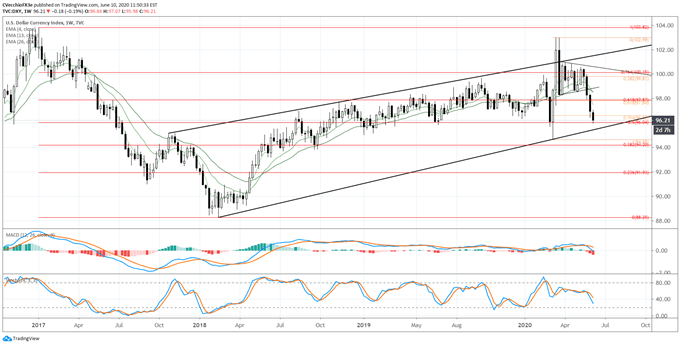

DXY PRICE INDEX TECHNICAL ANALYSIS: WEEKLY CHART (November 2016 to June 2020) (CHART 3)

A re-drawn weekly timeframe shifts our consideration from a possible bearish rising wedge from the 2018 low to a rising channel as a substitute, with help coming in on the March 2020 low. Within the final replace it was famous that “To this finish, the lack of the multi-month consolidation, in context of failure to climb by way of channel resistance, suggests {that a} deeper pullback in direction of channel help could also be within the works. Over the following few weeks, merchants might look so far as the 50% retracement of the 2017 excessive/2018 low vary at 96.04 as important help.” Now that the 50% retracement has been achieved, merchants must be on alert for a possible channel breakdown that might recommend extra important losses over the approaching months – maybe in direction of 88.00.

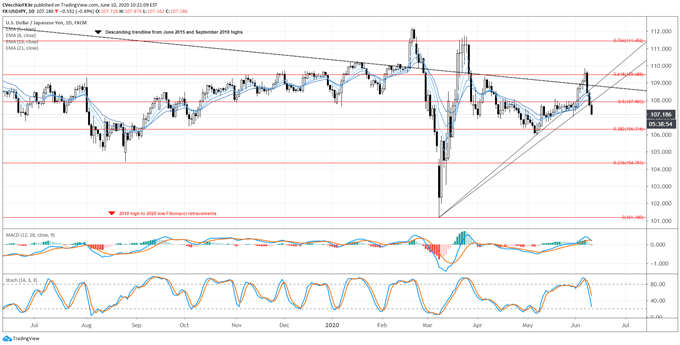

USD/JPY RATE TECHNICAL ANALYSIS: DAILY CHART (July 2019 to June 2020) (CHART 4)

USD/JPY’s losses in current days has seen the pair lose the rising trendline from the March and Could lows (from the beginning of Could or on the finish), breaking sharply from the rise in US fairness markets. However continued power in gold costs bodes nicely for the Japanese Yen, and amid considerations that the re-opening of developed economies has arrived too early has breathed life into the protected haven Japanese Yen. (To this finish, if danger urge for food sours, the US Greenback might quickly see life anew.)

On the technical entrance, the momentum profile for USD/JPY charges is changing into extra bearish, however extra work must be finished. USD/JPY charges are under the every day 5-, 8-, 13-, and 21-EMA envelope, which isn’t aligned in bearish sequential order but. Day by day MACD has turned decrease however stays above its sign line, whereas Sluggish Stochastics are simply dropping in direction of their impartial line. A lack of the late-Could swing low at 107.08 would sign a near-term high in place, with USD/JPY charges having failed to interrupt the descending trendline from the June 2015 and September 2018 highs for the third time this 12 months.

IG Shopper Sentiment Index: USD/JPY RATE Forecast (June 10, 2020) (Chart 5)

USD/JPY: Retail dealer knowledge reveals 50.57% of merchants are net-long with the ratio of merchants lengthy to quick at 1.02 to 1. The variety of merchants net-long is 16.50% increased than yesterday and a pair of.99% decrease from final week, whereas the variety of merchants net-short is 9.25% increased than yesterday and seven.40% increased from final week.

We usually take a contrarian view to crowd sentiment, and the very fact merchants are net-long suggests USD/JPY costs might proceed to fall.

Positioning is extra net-long than yesterday however much less net-long from final week. The mix of present sentiment and up to date modifications provides us an additional blended USD/JPY buying and selling bias.

Beneficial by Christopher Vecchio, CFA

Traits of Profitable Merchants

— Written by Christopher Vecchio, CFA, Senior Forex Strategist