RLI Corp. RLI has been raising investor optimism on the back of rate increases, improved retention, and a solid liquidity position.

Growth Projections

The Zacks Consensus Estimate for RLI’s 2021 and 2022 earnings per share is pegged at $3.43 and $3.63, indicating a year-over-year increase of 32.4% and 5.8%, respectively.

Estimate Revision

The Zacks Consensus Estimate for 2021 and 2022 has moved 1.5% and 6.8% north, respectively, in the past 30 days. This should instill investors’ confidence in the stock.

Earnings Surprise History

RLI has a decent earnings surprise history. It beat estimates in each of the last four quarters, with the average being 39.84%.

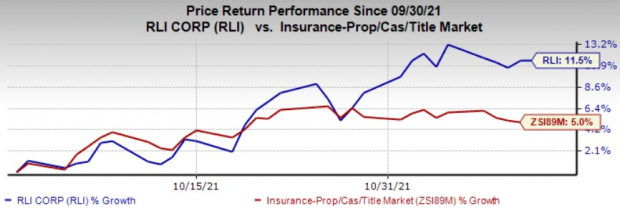

Zacks Rank & Price Performance

RLI currently carries a Zacks Rank #2 (Buy). Quarter to date, the stock has rallied 11.5%, compared with the industry’s increase of 5%.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Return on Equity (ROE)

The company’s ROE for the trailing 12 months is 12.8%, better than the industry average of 5.7%. This reflects the RLI’s efficiency in utilizing shareholders’ fund.

Business Tailwinds

RLI’s core business, Casualty, Property, and Surety witnessed significant growth in the first nine months of 2021 on the back of higher premiums from commercial excess and personal umbrella due to rate increases and expanded distribution. Rate increases and improved retention led to growth for the marine product. Growth within existing accounts and new business benefited Commercial surety while market disruption led to increased premium for miscellaneous surety.

Improvements in the current accident year loss ratio and a higher level of favorable development in 2021 are expected to lower the expense ratio, while growth in earned premium base and improved leverage on certain expenses should benefit the same.

RLI has maintained a combined ratio below 100 for 25 consecutive years, averaging 88.3, and below 90 for 13 straight years. In the first nine months of 2021, the combined ratio improved 450 basis points (bps) year over year to 88.9. It also maintains significant reinsurance protection against large losses.

Operating cash flows should continue to benefit from increased premium receipts. Its access to a revolving credit facility provides a borrowing capacity of $60 million that can be increased to $120 million if required.

RLI has a distinguished track record of success with 178 consecutive quarters of dividend increases and currently yields 0.9%, which is better than the industry average of 0.4%. In the fourth quarter of 2021, the insurer declared a special cash dividend in a bid to share the rewards of strong performance and return excess capital to shareholders.

Other Stocks to Consider

Some other top-ranked property and casualty insurers include First American Financial FAF, Cincinnati Financial Corporation CINF and Berkshire Hathaway (BRK.B). While First American sports a Zacks Rank #1 (Strong Buy), Cincinnati Financial and Berkshire carry a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

First American’s earnings surpassed estimates in each of the last four quarters, the average being 29.19%. In the past year the insurer has rallied 56.6%. The Zacks Consensus Estimate for 2021 and 2022 has moved 5.5% and 6.3% north, respectively, in the past 30 days.

Solid performance of the commercial market, improved direct premium and escrow fees and higher demand for title information products in data and analytics are likely to drive First American’s top-line growth.

Cincinnati Financial surpassed estimates in each of the last four quarters, the average earnings surprise being 40.05%. In the past year, CINF has rallied 55.8%. The Zacks Consensus Estimate for 2021 and 2022 has moved 2.8% and 5% north, respectively, in the past 30 days.

Cincinnati Financial is well poised to gain from premium growth initiatives, price increases and a higher level of insured exposures.

The bottom line of Berkshire Hathaway surpassed estimates in two of the last four quarters and missed in the other two, the average being 5.53%. In the past year, the insurer has rallied 25.2%. The Zacks Consensus Estimate for 2021 and 2022 has moved 0.08% and 1.5% north, respectively, in the past 30 days.

Berkshire Hathaway is expected to benefit from its growing Insurance business, Manufacturing, Service and Retailing, Finance and Financial Products segments, and strategic acquisitions.

Tech IPOs With Massive Profit Potential

In the past few years, many popular platforms and like Uber and Airbnb finally made their way to the public markets. But the biggest paydays came from lesser-known names.

For example, electric carmaker X Peng shot up +299.4% in just 2 months. Think of it this way…

If you had put $5,000 into XPEV at its IPO in September 2020, you could have cashed out with $19,970 in November.

With record amounts of cash flooding into IPOs and a record-setting stock market, this year’s lineup could be even more lucrative.

See Zacks Hottest Tech IPOs Now >>

Click to get this free report

RLI Corp. (RLI): Free Stock Analysis Report

Berkshire Hathaway Inc. (BRK.B): Free Stock Analysis Report

Cincinnati Financial Corporation (CINF): Free Stock Analysis Report

First American Financial Corporation (FAF): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

www.nasdaq.com