{kind=link}

After years touting the amazing transparency of blockchains, the crypto community has started to realize that privacy is actually essential for many traders, businesses and individuals.

Until now, balancing the right to privacy with the need to avoid jail time on money laundering charges has proven a difficult task, as the developers of Tornado Cash and Samourai Wallet have discovered.

But 2026 is the year that pragmatic privacy is poised to take off, with a slew of new projects tackling compliant forms of privacy for institutions and surging interest in existing privacy coins like Zcash — cheered on by Solana influencer Mert Mumtaz.

The Ethereum Foundation has formed a crack team of privacy experts to beef up protections in its ecosystem, while Coinbase is lobbying for updated regulations that don’t assume only bad actors want privacy.

Simon Seojoon Kim, CEO and founder of blockchain development firm Hashed, summed up the issues with blockchain transparency in a blog earlier this year:

“Web3 promised decentralization and privacy, but it actually created the most transparent surveillance system in history,” he wrote.

“Every transaction is permanently recorded, visible to everyone, and analyzed by AI. While there’s no rational reason to expose large leveraged positions, even hiding them in Web3 is nearly impossible.”

Once an address is connected to an individual, the game is up: real-time transaction history is exposed, position sizes are obvious and AI and bots can learn and analyze trading patterns.

The most famous example comes from May this year, when the entire crypto industry watched as anon trader James Wynn took out a $1.1 billion position with 40-times leverage on Hyperliquid. “Traders worldwide monitored this position in real-time, with blockchain analytics platforms transparently broadcasting every movement,” Kim said. Synthetix is relaunching this month as a perps DEX on Ethereum, talking up the fact trades are private by comparison.

Yuval Rooz, the co-founder and CEO of Digital Asset, the company that developed the tech behind Canton, the privacy focused blockchain network for financial institutions, says that the kind of tracking and exploitation of other traders’ positions, which is endemic in the crypto market, “would be considered to be a high, serious violation of market manipulation” in traditional financial markets.

For businesses the problem is even more acute, letting competitors see the inner workings of what a firm is buying and selling and from whom down to the last decimal place. It also tips off hackers to the location of a honeypot.

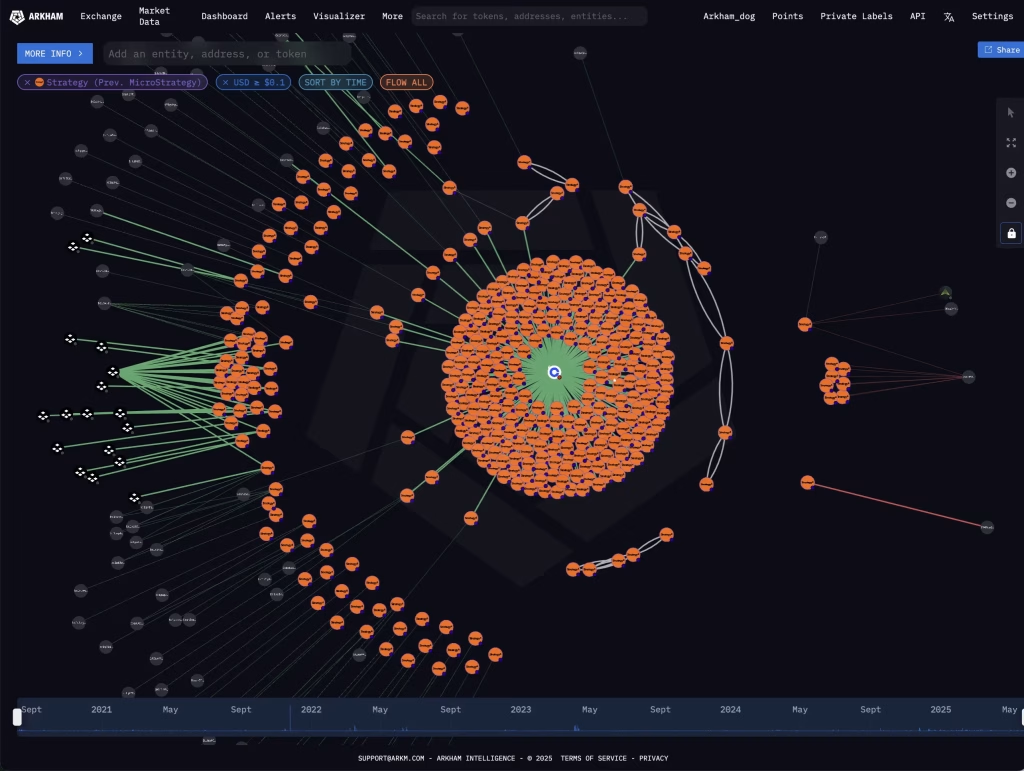

Michael Saylor, the chairman of Bitcoin reserve company Strategy, said he’d never reveal his company’s addresses, citing security concerns. But in May, blockchain analytics firm Arkham Intelligence announced they were confident they’d identified them.

Currently, those who wish to conceal trades are forced to employ advanced methods of hiding their addresses and identities using multiple wallets, dummy trades and proxy contracts. VPNs, separate trading-dedicated devices, and time-zone-distributed trading patterns are now standard for many.

But these methods are a poor facsimile of a genuinely private system, where identities and transactions are shared only on a need-to-know basis. But this begets another question: In an increasing regulated market, where adoption means compliance, how can regulators be comfortable with privacy?

Coinbase and Canton are getting regulators on board

One of the big issues with privacy is that financial regulators are often wary of it.

Privacy advocates maintain that regulators’ approaches to privacy and consumer protection are archaic, and need to be replaced in order to provide the security they really want.

Agata Ferreira, a board member for Blockchain for Europe and an assistant professor at the Warsaw University of Technology, argues that regulators’ “logic of shared observation” — that the more transparent something is — the safer it is, “is outdated and dangerous.”

“In a world where everyone is being watched, and where data is harvested on an unprecedented scale, bought, sold, leaked and exploited, the absence of privacy is the actual systemic risk.”

Posting about the EU’s Chat Control proposal, which would have required messaging platforms to let regulators scan encrypted messages, Vitalik Buterin said that privacy is not illegitimate.

“It is a minority (far from a majority!) in government and tech industry that is pursuing a type of absolutism, where they openly use phrases like ‘there should be no place to hide,’ seeking a kind of utopia (from their perspective) where they have the ability to see everything and nothing is out…

cointelegraph.com