{kind=link}

On Oct. 25, 2022 — about two weeks before the collapse of the world’s third-largest cryptocurrency exchange, FTX — prominent DeFi architect Andre Cronje published a foreboding article with a chilling warning on the state of centralized cryptocurrency exchanges:

“Remedies under the current regulatory regime are ineffective. Most investors sign away their rights to their crypto in voluminous terms and conditions of crypto-exchanges and many will (at best) rank as unsecured creditors should these exchange services be liquidated. Crypto exchange and crypto investment service providers are essentially operating as banks, but without the safeguards and regulation which banks are required to follow.”

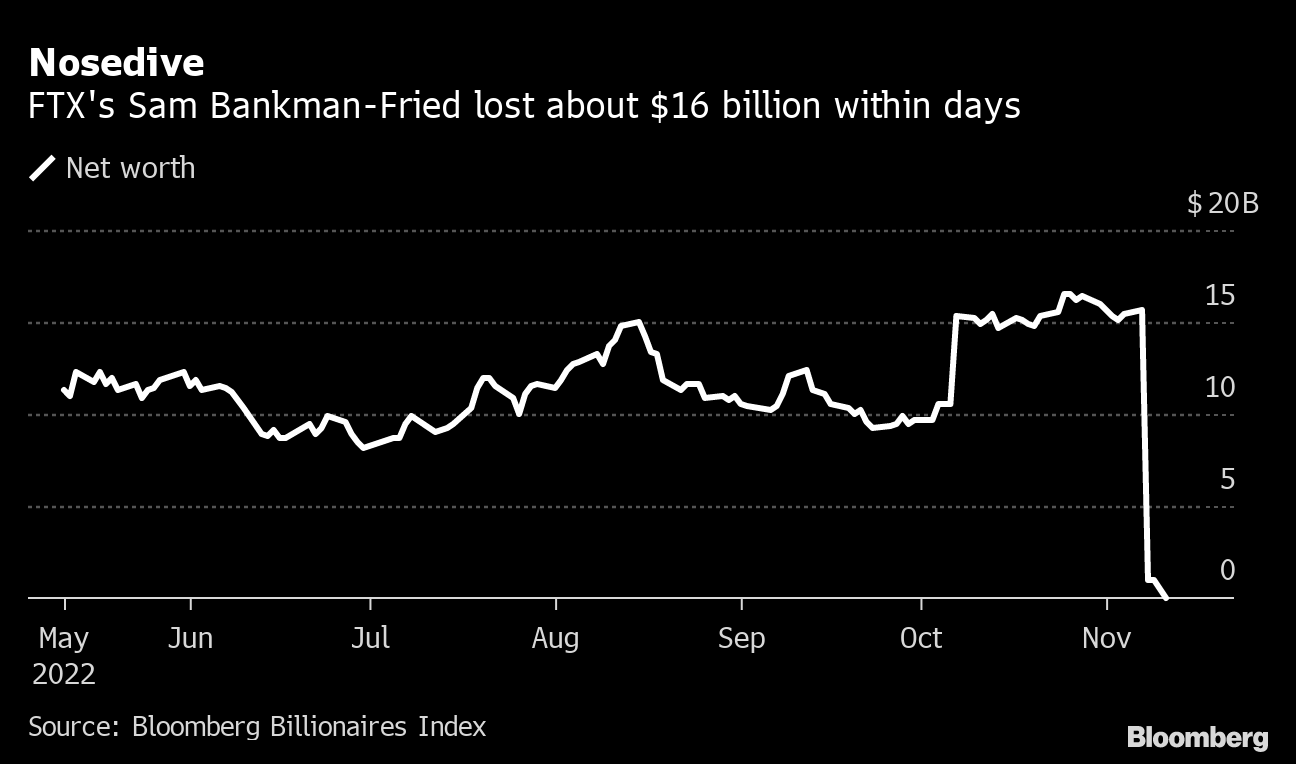

What happened afterward is history. With the abrupt downfall of FTX, customers suddenly discovered that despite all previous guarantees, their assets had been locked as the defunct exchange filed for bankruptcy amid an $8 billion shortfall — the consequence of senior executives siphoning customer assets to trade in related hedge fund Alameda Research. Even though the new management claims they have recovered some customer assets, clients’ funds still remain frozen in bankruptcy proceedings, with no end in sight and heavy legal fees to follow.

In the aftermath, the crypto community has raised serious concerns regarding the state of CEXs. Demands such as proof of assets and liabilities, segregation of customer funds, and voluntary registration as broker-dealers have echoed in the industry. That said, haven’t CEXs come this far by making an effort to legitimize their operations? Here’s why the issue is more complicated than meets the eye.

Why not just get regulated?

Jack Graves, a teaching professor at Syracuse University, tells Magazine, “To my knowledge, there is nobody acting as an exchange of cryptocurrencies and digital assets in the U.S. that is registered with the SEC. Instead, they simply stated that they don’t trade securities. And that’s a critical difference.”

Graves explains that while exchanges such as Coinbase are licensed money transmitters, they are not broker-dealers. “As soon as you talk about broker-dealers of securities, that triggers a bunch of disclosure and custody requirements,” Graves states. “I happen to use Fidelity as my brokerage company, and if Fidelity goes bankrupt, I’m not an unsecured creditor in bankruptcy. So, I have a claim to my assets before all the unsecured creditors.”

At least in the U.S., crypto exchanges cannot become broker-dealers because the digital assets they facilitate are not classified as securities by the SEC. Yet, there is also ample confusion on the matter.

“Gary Gensler has essentially said that everything except Bitcoin and maybe Ether is probably a security,” Graves says. “So, the exchanges are taking the view that until the SEC says it’s a security, they are going to trade it. And as soon as the SEC says crypto assets are securities, they are going to quit.”

The problem isn’t unique to the United States. Lennix Lai, managing director at Singaporean crypto exchange OKX, explains to Magazine that crypto exchanges cannot, as of now, be registered as broker-dealers due to a fundamental difference in their business model:

“By definition, a crypto exchange is actually a matching engine that matches orders from buyers and sellers. A broker-dealer license only governs the relationships that you, as the firm, have the capability to handle client orders and route them to a stock exchange. However, in the crypto world, most of the business models running are not the broker-dealer model but actually a ‘stock exchange’ model. So, that gives governments regulatory difficulty in that we don’t have an exchange license to apply for.”

Canada is one of the few jurisdictions that offer a clear regulatory pathway for exchanges to become registered broker-dealers — perhaps due to the sudden collapse of major Canadian crypto exchange QuadrigaCX in 2019.

In Canada, all prospective crypto exchanges must register with the Investment Industry Regulatory Organization of Canada and applicable provincial regulators to conduct business. On June 22, 2022, the Ontario Securities Commission announced it had issued an enforcement action against Bybit and KuCoin, alleging the two operated unregistered crypto asset trading platforms in the country.

After registration, crypto exchanges in Canada become broker-dealers just like their stock-trading counterparts, even though regulators ruled that the assets facilitated by the exchanges are not securities. As Katrina Prokopy, chief legal officer at Canadian exchange Coinsquare, explains to…

cointelegraph.com