By Mike Clark, Consulting Actuary, the Principal Monetary Group

By Mike Clark, Consulting Actuary, the Principal Monetary Group

A lot of my function as an actuarial blogger is explaining the habits of numbers by way of phrases, nevertheless it takes a number of phrases to clarify numerical habits typically which leads sadly to acronyms.

One of the vital important acronyms utilized in managing pension danger is “LDI” for “legal responsibility pushed investing”. LDI is commonly described as utilizing lengthy period bonds to cut back the chance of outlined profit (DB) plans. I’ve no objection to this definition (I exploit it myself often within the weblog) so long as all of us acknowledge it’s an oversimplification.

Actually studying the phrases behind LDI signifies investments are merely pushed by liabilities’ response to bond charges, however matching period is just not explicitly talked about. This implies LDI methods want solely take legal responsibility habits under consideration, which is sort of totally different from instantly matching asset and legal responsibility durations.

Yeah! One other Acronym!

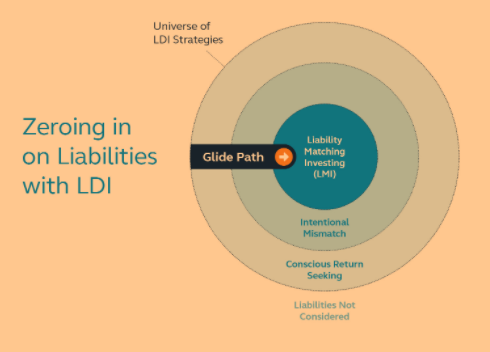

As a public service to right this semantical confusion, I wish to formally suggest a brand new acronym: “LMI” for “legal responsibility matching investing”. LMI is what many individuals imagine LDI to be, that’s the most hedging of a pension legal responsibility with bonds of matching period and high quality.

The excellence between LMI and LDI is essential nowadays, as a result of the misunderstanding is interfering with fiduciaries’ implementation of sound danger administration methods. I typically hear sponsors and advisors make feedback like, “We’re not able to do LDI now as a result of bond charges and our funding ratio are too low.”

Sadly, this can be a letter off. What they imply is that they don’t wish to implement LMI (catching on but?) as a result of it primarily locks of their underfunded place and forfeits potential advantages if charges rise sooner or later. I absolutely perceive the sentiment.

Nevertheless, the literal which means of the “not prepared” assertion is that funding selections mustn’t even take legal responsibility volatility under consideration, a remark no fiduciary this aspect of Y2K ought to ever make. The one funding technique that’s not LDI from a literal viewpoint is complete ignorance of plan liabilities, which I’m positive isn’t what the speaker supposed.

Everybody Wants LDI

So whereas not everybody is able to implement LMI as we speak, all pension sponsors want LDI in some kind. Funding and financial circumstances could range broadly throughout plans and sponsors, however every one ought to weigh their want and talent to take funding danger within the context of the liabilities of their plans.

Whether or not it’s understood or not, the acutely aware choice to not match period remains to be pushed by the liabilities and qualifies as LDI. A glide path growing period matching as funding ratios enhance and/or rates of interest rise can also be pushed by liabilities and counts as LDI. Truly hedging danger by matching period instantly is each LMI and LDI (since it’s each matched and pushed by liabilities.)

So LMI and LDI are associated, however totally different. (All LMI is LDI, however not all LDI is LMI.) Understanding this distinction is a vital first step to constructing an efficient danger administration technique, and serving to choice makers perceive when and if a transfer to LMI is acceptable.

So please be part of me in welcoming LMI to the crowded area of pension acronyms! Hopefully the advantages of creating the excellence outweigh including another to the checklist.

Mike Clark is a fellow of the Society of Actuaries (SOA) and a member of the American Academy of Actuaries (AAA), although he was nonetheless taking exams through the pre-Y2K complete return period.

Initially printed by Principal, 11/23/20

Affiliation Disclosure

The subject material on this communication is academic solely and supplied with the understanding that Principal® is just not rendering authorized, accounting, funding recommendation or tax recommendation. You need to seek the advice of with acceptable counsel or different professionals on all issues pertaining to authorized, tax, funding or accounting obligations and necessities.

Insurance coverage merchandise and plan administrative companies are offered by Principal Life Insurance coverage Firm, a member of the Principal Monetary Group® (Principal®), Des Moines, IA 50392.

1411957-112020

Learn extra on ETFtrends.com.

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.