By Patrick Watson

By Patrick Watson

The US Shopper Worth Index is up 5% since Could 2020, in accordance with information launched final week. This was the most important 12-month enhance since 2008.

Some Wall Road denizens act like Weimar Germany-style hyperinflation is right here. I feel not. I’m sufficiently old to recollect when 3–5% inflation was regular. Even when CPI stays in that vary, which I doubt, it could merely be a return to what everybody lived with within the 1990s. In some way we survived.

Supply: Wikimedia

On the identical time, even 3% inflation isn’t good. The Federal Reserve is meant to ship “value stability.” Fortunately, they’ve prevented hyperinflation. However even delicate inflation, compounded over years, is the reverse of value stability.

And for a lot of people, inflation isn’t delicate. Tried renting an condo these days?

Whether or not inflation is an issue relies on your private scenario. It varies so much, relying in your location and the way you spend your cash. It’s additionally simpler to tolerate if your revenue rises on the identical charge as your price of residing.

The inflation we’re seeing now comes largely from the COVID-19 pandemic… however not essentially within the methods you would possibly anticipate.

5 Culprits

CPI is an index, weighted to mirror the value change in a hypothetical basket of products and companies. It’s also topic to important statistical changes. It doesn’t mirror anybody’s actuality, however it’s the measure now we have.

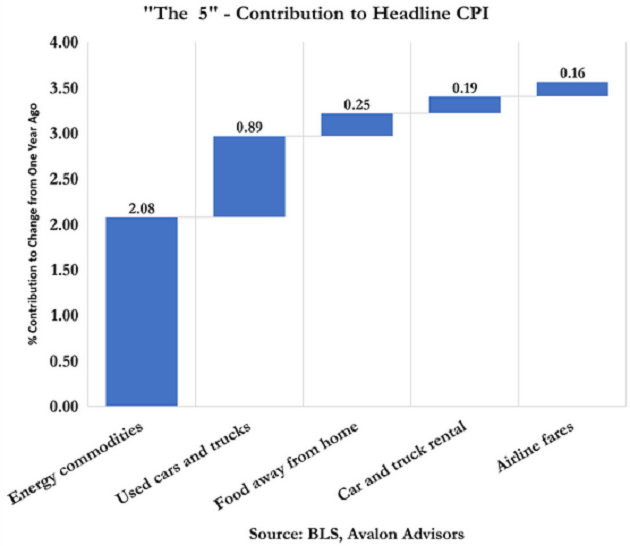

The yearly soar that has individuals so involved was extremely concentrated. Samuel Rines at Avalon Advisors calculates simply 5 objects accounted for 71% of the change in headline CPI.

Supply: Avalon Advisors

The 5 main culprits have been:

What do all these have in frequent?

For one factor, all their costs have been severely depressed in Could 2020, the start of the interval in query. Many US companies have been closed, staff laid off, and fearful customers staying house. Eating places, if open in any respect, have been doing solely take-out service. Few individuals have been shopping for airline tickets or renting vehicles.

Examine that to immediately. Vaccinated individuals are resuming their prior actions, enterprise is booming in lots of segments, and financial optimism abounds.

After all the costs that fell probably the most in that odd interval have rebounded probably the most. That ought to shock nobody. However there’s extra to this story.

Discover two of the classes are vehicle-related. That’s not coincidence.

- When the pandemic struck, automobile rental firms discovered themselves holding some very costly, idle property. They moved rapidly to promote their fleets, pushing used automobile costs down.

- On the identical time, automobile producers misplaced orders from these giant clients, and moved to cut back their very own output. This lowered the availability of recent vehicles on the market.

- Many People who used to depend on public transportation or ride-sharing companies determined they might fairly have their very own vehicles. Authorities stimulus applications gave them some additional money to spend, too.

All this occurred whereas microchips—a serious element in fashionable autos—have been briefly provide resulting from commerce and nationwide safety disputes between the US and China. This additional lowered new automobile provides, encouraging customers to search for used ones—and driving their costs greater.

As for automobile leases… it’s easy provide and demand. They’ll’t lease vehicles they don’t have. They bought the used ones and haven’t been in a position to purchase new replacements. In order that they’re charging extra for the few autos out there.

Now the query is whether or not these components will persist. In that case, we are able to anticipate used car costs to maintain rising, presumably boosting inflation additional. Will they?

They may. Taiwan, the world’s main microchip supply, had been comparatively spared from COVID harm. However now it’s experiencing a critical COVID outbreak, which appears to be centered on the overseas microchip staff who reside in crowded dormitories. That is additional limiting new car provide, and lots of different items, too.

However the different components are most likely fading. Individuals who want a automobile to get to work have most likely discovered one, or made different preparations. Public transit no less than appears safer.

Mobility information reveals individuals are shifting round virtually as a lot as they have been earlier than the pandemic. Meaning gas demand might be about again to regular. Costs might rise for different causes (we’re getting into hurricane season, for example) however vitality costs ought to start stabilizing. There’s little purpose to anticipate one other yr just like the final one.

Supply: WIkimedia

Hidden Inflation

Inflation doesn’t all the time present in costs. As an illustration, I’ve seen a pattern the place merchandise aren’t out there within the native retailer, however the identical retailer will fortunately ship it for supply subsequent week.

That’s a form of hidden value enhance: Making you wait as a substitute of taking your buy house instantly. CPI doesn’t seize this until the value rises, too.

Inflation is actual, and it’s painful for many individuals. Nonetheless, it’s not the form of inflation that may proceed boosting CPI. What we’re seeing now could be a brief consequence of the pandemic which, whereas not gone, is no less than receding as extra individuals get vaccinated.

Federal Reserve officers appear way more involved about employment. Earlier than they tighten coverage, they wish to see the thousands and thousands of still-unemployed individuals get jobs once more, and the thousands and thousands who left the labor power get again within the sport.

If that occurs, it’s going to take some time. So anticipate the Fed to remain accommodative for a very long time.

Initially revealed by Mauldin Economics, 6/15/21

Learn extra on ETFtrends.com.

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.