Financial Overview November 1, 2020

Financial Overview

November 1, 2020

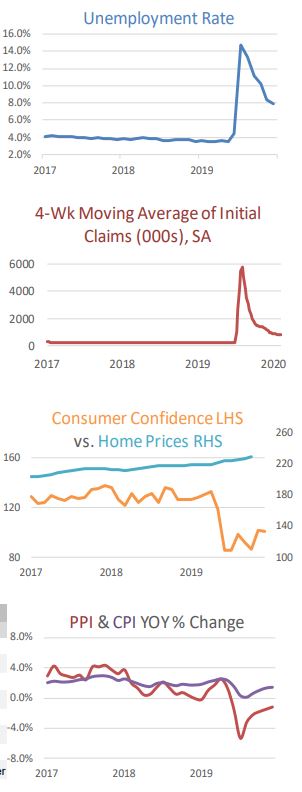

As anticipated, the Advance Estimate for third quarter US Gross Home Product confirmed an enormous rebound from Q2’s Covidinduced collapse. GDP rose at a 33.1% annual fee, on the heals of Q2’s beautiful -31.4% annualized decline. The information would appear to point the US is poised for extra of a V-shaped financial restoration, though the divide between winners (tech) and losers (journey & leisure) continues to widen.

On the eve of a doubtlessly historic political election day, the US financial system continues to grapple with pandemic-related challenges, with no clear resolution in sight, wanting a broadly accessible and efficient vaccine. Regardless of the obstacles to a easily operating financial system, large fiscal and financial stimulus has prompted a faster than anticipated restoration in housing and manufacturing, and almost all issues tech.

Regardless of a small MoM drop in New Residence Gross sales in September, Present Residence Gross sales rose a greater than anticipated +9.4% whereas Constructing Permits surged +5.2% MoM and Mortgage Purposes continued to rise. Mortgage charges remained close to traditionally low ranges and the burgeoning millennial cohort is popping in direction of single-family housing, spurred on by the pandemic.

Inflation, as measured by the Shopper Value Index, remained tame, with the September CPI rising +0.2% MoM (+1.4% YoY), whereas producer costs gained +0.4% MoM (and solely +0.4% YoY). Declines in vitality costs, in addition to rents, helped maintain total inflation ranges in examine.

The Federal Reserve’s FOMC meets this week and it’s broadly anticipated they’ll maintain the Fed Funds fee on the zero-bound. Buyers might be searching for any trace of potential coverage change following the election outcomes, ought to they be identified by the point of the assembly. All bets are at the moment for a spike in volatility as we grind our method by way of this week.

[wce_code id=192]

Home Fairness

November 1, 2020

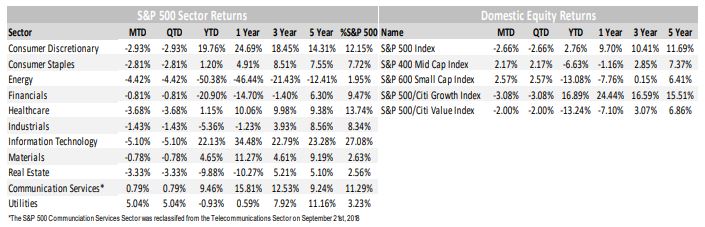

U.S. equities fell sharply final week, with the benchmark S&P 500 Index dropping -5.6% to shut the month at 3,269. For the month, Giant-Caps posted a -2.66% decline and now are barely in optimistic territory for the yr, up a scant +1.2%; nonetheless, given the uncertainties 2020 has offered, and on the eve of one of the vital consequential elections in latest reminiscence, the truth that the S&P 500 is in optimistic territory might be seen as stunning by itself.

Mid- and Small-Caps then again fared significantly better in October, with the S&P MidCap 400 Index gaining +2.17% and the S&P SmallCap 600 Index gaining +2.57%. Whereas smaller firms have largely been left behind this yr (Mid- and Small-Caps are down -6.63% and -13.08%, respectively), they’ve lately confirmed indicators of life as prospects for added financial stimulus come into focus.

Worth outperformed Progress, with the S&P 500 Citi Worth Index dropping -2.00% in comparison with the S&P 500 Citi Progress Index which shed -3.08%. For the yr, Progress stays dominant, up +16.89% versus -13.24% for Worth.

From a sector standpoint, earnings from the world’s largest Expertise (and equally associated) firms dissatisfied final week, regardless of many income and earnings beats. The selloff is probably going extra of a operate of how inventory costs for Fb, Apple, Amazon, Microsoft and Google (collectively FAAMG) have soared in 2020 as beneficiaries of the present pandemic. For the month of October, the Expertise sector (Apple, Microsoft) shed -5.10% whereas Shopper Discretionary (Amazon) misplaced a extra modest -2.93%. Communication Providers (Fb, Google) was truly optimistic by +0.79% due to a positive response from traders in direction of Google, regardless of damaging sentiment in direction of Fb.

On a brighter notice, Utilities had been firmly within the black through the month, gaining +5.04%, handily outpacing the broad -2.66% decline available in the market. Curiously, Utilities nonetheless stay in damaging territory for the yr down -0.93%, regardless of their engaging valuation and yield relative to different elements of the market.

With the financial system persevering with to get well, a continued rotation into Worth, Small-Caps, and cyclical sectors could also be on the horizon.

Worldwide Fairness

November 1, 2020

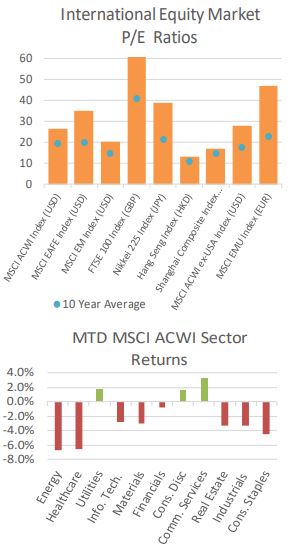

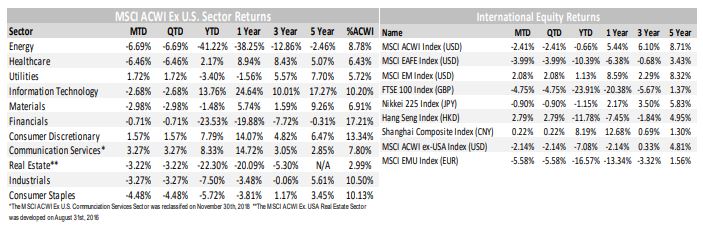

Worldwide equities had been a combined bag in October with Developed Markets (DM), as measured by the MSCI EAFE Index, down -3.99%. Then again, Rising Markets (EM), as measured by the MSCI EM Index rose +2.08% as continued financial power emanates from Asia. For the yr, EM (+1.13%) continues to outpace DM (-10.39%) by a large margin.

In Developed Markets, worries persist round latest Covid outbreaks in Europe, with newly imposed restrictions introduced prior to now week in France, Germany, and the UK. With lockdowns imposed in France and the U.Okay., Germany took a extra measured strategy and closed bars and eating places, amongst others. Regardless, the headlines and Covid associated information stay weak and worrisome for all of Europe.

In Rising Markets, China continues to rebound and energy financial development within the area. The upcoming preliminary public providing (IPO) of Alibaba affiliated Ant Group is predicted on November fifth and must be the most important IPO on document at greater than $34B. The IPO is slated as a twin itemizing in Hong Kong and Shenzhen (on the newly fashioned STAR board) which is akin to the NASDAQ within the U.S. Investor pleasure over Ant, in addition to bettering absolute and relative fundamentals proceed to energy Rising Markets and buoy their native currencies.

From a sector standpoint, MSCI ACWI ex US Communication Providers, Utilities, and Shopper Discretionary posted optimistic returns on the month, up +3.27%, +1.72%, and +1.57%, respectively. Laggards included Power, Healthcare, and Staples, down -6.69%, -6.46%, and -4.48%, respectively. For the yr, Expertise stays the highest performer up +13.76%, whereas Power stays the worst performer, down -41.22% YTD.

Taking a look at particular nations, Japan has served as a protected haven inside DM, with the Nikkei 225 Index (in JPY) giving again solely -0.90% in November. For the yr, Japanese equities are down -1.15%, a pointy distinction to its DM friends. In EM, China stays firmly within the black, with the Shanghai Composite (in CNY) gaining +0.22% on the month, and +8.19% on the yr to outperform most different DM and EM nations alike.

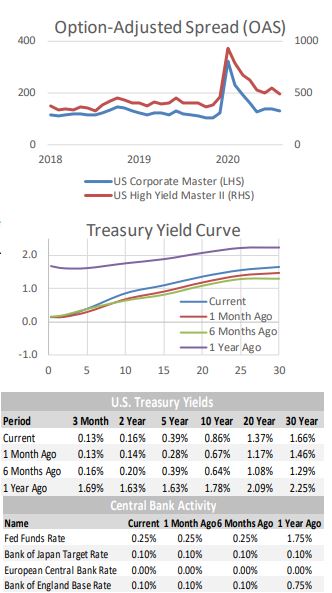

Mounted Earnings

November 1, 2020

Fed Chairperson Jerome Powell is prone to renew his name for added fiscal stimulus throughout this week’s assembly. Whereas he has mentioned there are further avenues of stimulus that the Fed may pursue, together with bigger asset purchases, he doesn’t at the moment really feel that it’s applicable to ramp up financial stimulus additional. This permits him to maintain some financial stimulus in reserve to battle potential future points.

Fiscal stimulus talks are on maintain because the nation awaits the Presidential election outcomes. Regardless of the consequence of the election, vital fiscal stimulus is predicted to be a high precedence. Excessive unemployment and concern about re-skilling those that have been impacted essentially the most by the pandemic recession ought to present help for an infrastructure invoice. Restore what now we have, assemble what we want, and develop our skilled-trades whereas we’re doing so.

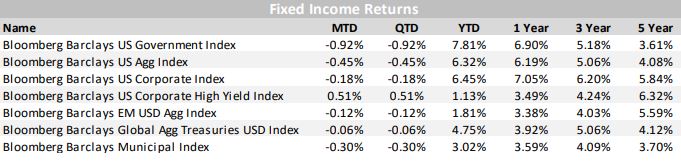

Treasury bond yields elevated throughout October. This transfer made the Authorities Index the worst performer of the month, and was a drag on the efficiency of the Combination Index. After a pair months of credit score spreads creeping wider, they reversed course in October. Funding Grade spreads fell by ~10 bps, offering a efficiency tailwind and offsetting a number of the impact of rising Treasury yields, netting close to breakeven efficiency. Excessive Yield spreads had been choppier, however ended up ~18 bps decrease. The extra yield supplied by Company bonds mixed with the unfold contraction in October resulted in engaging efficiency to kick off the fourth quarter.

Tax-free Municipal bond yields proceed to look engaging in comparison with related maturity Treasury bonds. As with Company bonds, sector exposures are vital to handle danger. Issuers which might be significantly affected by the pandemic skewed atmosphere must be underweighted. Longer maturity tax-free Munis at the moment provide yields in extra of Treasury bond yields, which is anomalous. Much more so contemplating the proposed tax will increase of the Biden marketing campaign. Whereas the election stays up within the air, proudly owning tax-free bonds gives a pleasant hedge in opposition to much less accommodative tax brackets sooner or later.

Various Investments

November 1, 2020

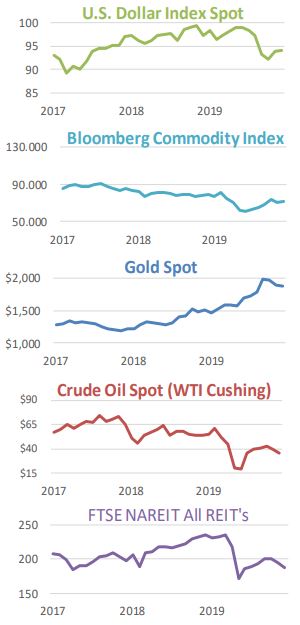

Various investments had been a combined bag throughout October. The Bloomberg Commodities Index was up +1.40% for the month regardless of the US Greenback having barely optimistic efficiency (ie, a stronger Greenback often hurts Commodities).

WTI Crude Oil was one of many worst performing alternate options for the month, returning -11.55% and shutting at $35.79/barrel on the NYMEX. Decrease vitality demand from renewed COVID-19 restrictions and pent-up provide have put strain on oil costs to stay low. Gold was down -0.37% for the month, however remains to be up +24.66% YTD. Low rates of interest, a weak greenback, and falling actual yields have helped the valuable metallic be one of many high performing asset courses in 2020.

Actual property, as measured by the FTSE NAREIT All REIT Index, fell -3.35% through the month and is down -15.21% YTD. Though the broad Actual Property market has been weak, sure subsectors such Cell Towers, Knowledge Facilities, and E-Commerce Logistics Warehouses have been standout winners. These growth-oriented segments of the market ought to stay beneficiaries of the continued rise of e-commerce, the 5G community buildout, elevated cellular information utilization, in addition to different elements.

Volatility, as measured by the CBOE VIX Index, elevated considerably all through October to shut the month at 38.02, nicely above its long-term common. Rising coronavirus instances, the upcoming election, and a scarcity of readability round extra stimulus have all performed in a task in creating excessive ranges of volatility.

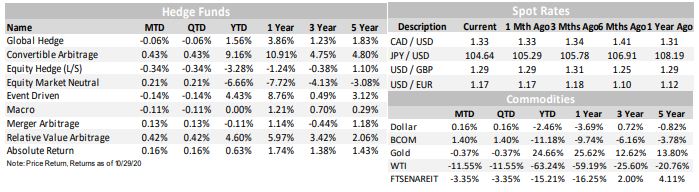

Hedge Fund methods posted combined outcomes through the month, with 5 of 9 methods tracked posting barely optimistic returns. Convertible Arbitrage was the highest performer for the month, and stays the highest performer YTD, being up +9.16%. Fairness Market Impartial is the worst performing technique for the yr, down -6.66% YTD. That is stunning on condition that market impartial funds are meant to mitigate market danger and supply optimistic efficiency no matter market circumstances.

ESG

November 1, 2020

The Division of Labor’s proposed crackdown on ESG investments inside ERISA retirement plans has been walked again considerably after the unimaginable pushback that was shared through the rule’s remark interval. A whopping 94% of all feedback submitted relating to the proposed rule had been in opposition to the generalized assault on investments that combine ESG issues and the danger & return implications of doing so.

It’s doubtless that the rule could also be additional watered down or scrapped altogether if the Presidential election goes Joe Biden’s method, as his marketing campaign has been very supportive of Inexperienced and Social funding objectives.

It isn’t obscure why the rule was weakened, as we see continued outperformance by the broad ESG indexes and ESG mangers. These methods have continued to see vital investor curiosity and obtain a big proportion of funding flows. By July of 2020, ESG fund inflows had already eclipsed their whole for all of 2019 and had been on their technique to one other record-breaking yr of asset gathering. In accordance with Jon Hale of Morningstar, in September, 24% of all U.S. inventory and bond fund inflows had been allotted to ESG methods.

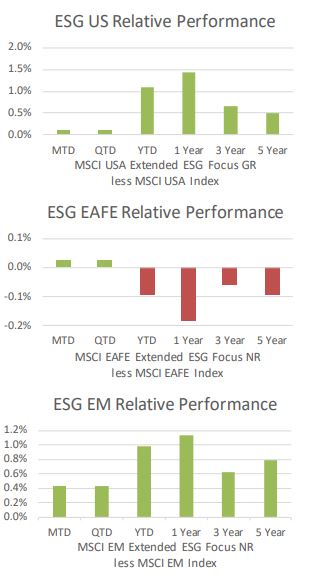

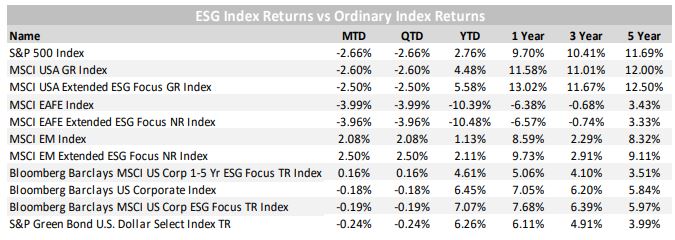

The MSCI USA Prolonged ESG Focus Index has continued to carry out nicely, outperforming the MSCI USA Index by 90 bps YTD. The MSCI EAFE Prolonged ESG Focus Index was up Four bps over the MSCI EAFE Index in October, though longer-term returns proceed to lag barely. MSCI EM Prolonged ESG Focus Index continues its streak of robust efficiency over the MSCI EM Index, extremely additive throughout all time durations.

If in case you have any questions or feedback, please be happy to contact any member of our funding group:

Tom Quealy, Chief Government Officer – [email protected]

Larry Whistler, CFA, President/Chief Funding Officer – [email protected]

Nick Verbanic, CFP® V.P./Portfolio Supervisor – [email protected]

Matthew Krajna, CFA, Senior Portfolio Supervisor, Director of Fairness Analysis –

[email protected]

Tim Calkins, CFA, Senior Portfolio Supervisor, Director of Mounted Earnings – [email protected]

Nick DiRienzo, CFA, Director of Operations – [email protected]

Mike Skrzypczyk, Senior Dealer/Affiliate Portfolio Supervisor – [email protected]

Angila Snediker, Buying and selling Affiliate – [email protected]

Nottingham Advisors, Inc. (“Nottingham”) is an SEC registered funding adviser with its principal office within the State of New York. Nottingham and its representatives are in compliance with the present registration necessities imposed upon registered funding advisers by these states through which Nottingham maintains purchasers. Nottingham might solely transact enterprise in these states through which it’s registered, or qualifies for an exemption or exclusion from registration necessities. This materials is proscribed to the dissemination of common info pertaining to Nottingham’s funding advisory/administration providers. Any subsequent, direct

communication by Nottingham with a potential consumer shall be performed by a consultant that’s both registered or qualifies for an exemption or exclusion from registration within the state the place the potential consumer resides.

The data contained herein shouldn’t be construed as personalised funding recommendation. Previous efficiency is not any assure of future outcomes. Data contained herein shouldn’t be thought of as a solicitation to purchase or promote any safety. Investing within the inventory market includes the danger of loss, together with lack of principal invested, and is probably not appropriate for all traders. This materials accommodates sure forward-looking statements which point out future potentialities. Precise outcomes might differ materially from the expectations portrayed in such forward-looking statements. As such, there isn’t a assure that any views and opinions expressed on this letter will come to move. Moreover, this materials accommodates info derived from third social gathering sources. Though we imagine these sources to be dependable, we make no representations as to the accuracy of any info ready by any unaffiliated third social gathering included herein, and take no accountability subsequently. All expressions of opinion mirror the judgment of the authors as of the date of publication and are topic to vary with out prior discover. Previous efficiency is just not a sign of future outcomes.

The indices referenced within the Nottingham Month-to-month Market Wrap are unmanaged and can’t be invested in instantly. The returns of those indices don’t mirror any funding administration charges or transaction bills. Had these further charges and bills been mirrored, the returns of those indices would have been decrease. Data herein has been obtained from third social gathering sources which might be believed to be dependable; nonetheless, the accuracy of the info is just not assured by Nottingham Advisors. The content material of this report is as present as of the date indicated and is topic to vary with out discover.

For info pertaining to the registration standing of Nottingham, please contact Nottingham or discuss with the Funding Adviser Public Disclosure site (www.adviserinfo.sec.gov). For added details about Nottingham, together with charges and providers, ship for our disclosure assertion as set forth on Type ADV from Nottingham utilizing the contact info herein. Please learn the disclosure assertion fastidiously earlier than you make investments or ship cash.

Learn extra on ETFtrends.com.

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.