By Jared Dillian

Faculty’s in session. Let’s speak about math.

Return to your calculus class senior 12 months in highschool. You’re taking the spinoff of y with respect to x. You might be discovering the sensitivity to the change within the perform with respect to a change within the argument. In sensible phrases, that is the slope of a line or the speed of an object.

Then, take the spinoff of the spinoff—the second spinoff. In sensible phrases, this measures the curvature of a line or the acceleration of an object. Because it seems, individuals have a really troublesome time with the second spinoff.

The second spinoff is in every single place in finance. It’s convexity in bonds or gamma in choices. When somebody blows up within the monetary world, it’s often a failure to grasp the second spinoff. Human beings suppose linearly and statically. It’s possible you’ll know your publicity right here, however you could not understand it over there.

Some second derivatives, like convexity and gamma, are measurable and identified. A few of them are hidden and unknown. I’ve talked about hidden gamma earlier than in The 10th Man, which we noticed in March 2020—the purpose the place individuals liquidate their positions and promoting accelerates.

When you see the second spinoff, you possibly can’t unsee it. It’s in every single place you go. And then you definately’re looking out for it.

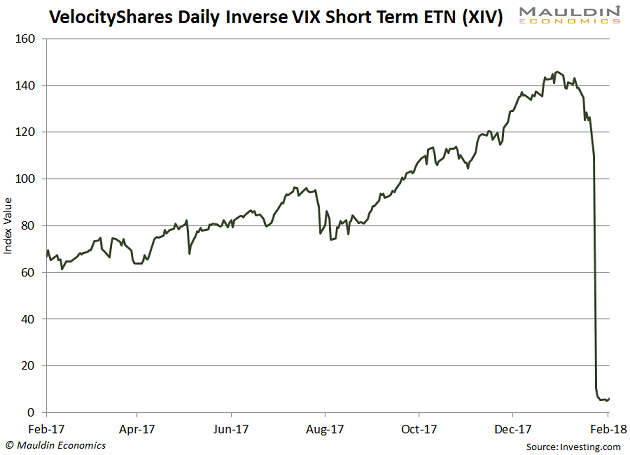

The second spinoff produces charts like this:

After which individuals marvel what the hell occurred.

Shares Have Convexity

The very first thing to grasp is that shares have convexity. Some shares are positively convex, and different shares are negatively convex.

If that seems like Greek to you, right here’s a less complicated method to consider it…

- A positively convex inventory goes up quicker than it comes down.

- A negatively convex inventory goes down quicker than it goes up.

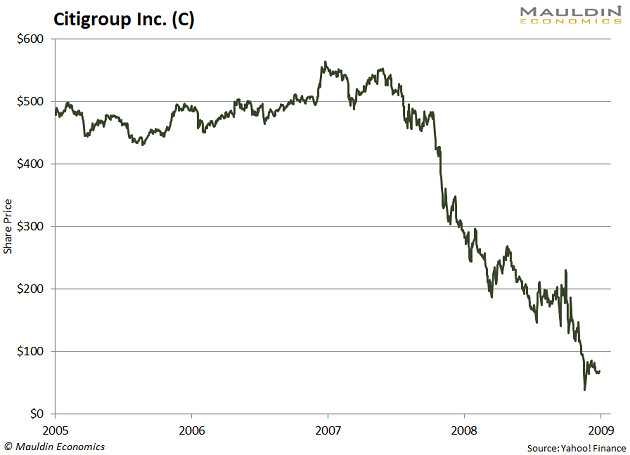

Loads of shares, just like the banks, have been negatively convex in 2007. The banks had offered quite a lot of optionality, which turned them into engines of damaging convexity. They went up slowly and got here down quick, which is roughly the payoff of a brief choice.

You may see this with Citigroup Inc. (C) within the subsequent chart.

Normally, tech shares and biotech shares are positively convex. However there are exceptions. And there are positively convex shares in loads of different industries, together with retail, power, and mining.

This doesn’t imply which you could’t have a negatively convex inventory in your portfolio, however on stability, your portfolio must be positively convex. If dangerous issues occur to the market, you need good issues to occur to you.

Lots of people don’t understand that shares have embedded convexity—they have a look at the chart and it appears fairly simple. Shares go up and down. However generally they go up or down very quickly.

A lot of the evaluation I do on shares shouldn’t be static monetary statements. It’s how the underlying enterprise can change in a convex trend.

Convexity finally ends up fooling most individuals—they purchase one thing that’s linear that finally ends up being nonlinear in a malignant method. It’s a troublesome idea to grasp.

Many individuals dismiss the meme shares like GameStop Corp. (GME) and AMC Leisure Holdings, Inc., however there may be plenty of convexity there, and gigantic alternatives. Convexity actually fooled the individuals who have been brief GME.

Convexity can be created by liquidity, which is one thing I perceive properly, having labored on a program buying and selling desk. In case you personal a inventory that trades 500,000 shares a day, attempt to think about what would occur if it traded 50,000,000 shares in a day. There isn’t a place for it to go however up, or down.

Bonds

I had positions in most well-liked inventory and high-yield bond funds up till not too long ago. I offered them due to the huge damaging convexity.

I attempt to maintain issues so simple as attainable—excessive yield can’t go up far more, however it will possibly go down lots. One option to win, some ways to lose.

The coupon you get off high-yield bonds is just like the premium you get from promoting choices. Generally (when the Fed isn’t concerned), that premium is massive and bonds turn out to be extra enticing. Individuals who perceive earnings investing know intuitively in regards to the damaging convexity current in these methods.

One of many tragedies of Zero Curiosity Price Coverage is that it has compelled retirees to load up on damaging convexity in quest of earnings, often within the type of company bonds and excessive dividend shares.

Within the previous days, you could possibly depart cash within the financial institution, which was primarily zero convexity. In case you have a look at a chart of the typical retiree’s portfolio, it’s a collection of gradual climbs with breathtaking drops. The Federal Reserve, of all individuals, doesn’t perceive convexity.

When you begin fascinated about your portfolio by way of convexity, your outcomes will enhance. And I don’t imply simply returns—I imply risk-adjusted returns.

After all, the easiest way so as to add constructive convexity to a portfolio is to simply purchase choices. However for most individuals, that’s higher left to the consultants.

Initially revealed by Mauldin Economics, 6/10/21

Learn extra on ETFtrends.com.

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.