The fate of Asian FX in 2023 was largely a function of US dollar strength, overlaid with a myriad of local economic factors, which saw some currencies perform better than others at different times, though the broad theme was Asian FX losses against the USD. The Malaysian Ringgit came bottom of the pack, losing more than 5.5%, while Indonesia’s rupiah, India’s rupee and the Phillippine peso all made smaller losses, weakening by around 0.5%. All currencies have nevertheless lost ground to the US dollar in 2023 year-to-date, and we would anticipate all of them making up some, though probably not all of this lost ground in 2024.

Within the FX pack, some currencies were essentially propped up by the local central bank, which stepped in to manage volatility. That sums up the Chinese yuan and Indian rupee and likely means that they will underperform their peers when broad trends call for some appreciation against the USD. Indonesia and the Philippines have taken a slightly different tack, using monetary policy tightening to support their currencies, and in turn, they too may see their 2024 upside capped, especially if they choose to remove some of this tightening.

China’s macro story is also likely to be a strong factor limiting the upside when (and indeed if) it eventually materialises. With the exception of India, China is the single largest trading partner of every country in the region. That could help to cap any upside in the North Asian currencies in 2024, as none are likely to totally shake off the drag from a more sluggish CNY in 2024 and our China outlook remains for only modest growth in 2024.

One factor that we shouldn’t discount in 2024 is the possibility that in removing Japan’s negative policy rates in mid-2024, a seismic shift in the JPY could occur that pulls other Asian FX along for the ride. We’d put this out as a risk case rather than a base case, though we do seem to be making glacial progress in this direction. As an isolated event risk, this is one we will be keeping firmly on our radar, even if it is not a central view.

{kind=link}

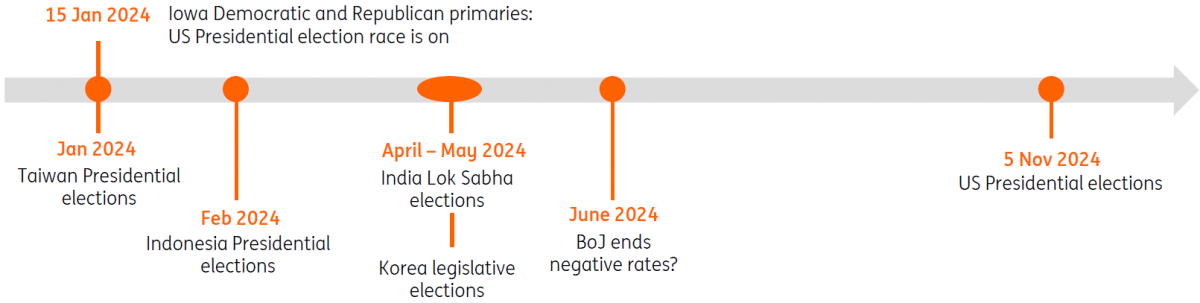

The other factors that are likely to feature heavily are geopolitics and external demand. On the geopolitical front, we start the year with Taiwan’s presidential elections. Historical precedent leads us to expect that Mainland China will respond with military confrontations across the Straits of Taiwan, which are likely to manifest through weaker Taiwanese stocks and a weaker Taiwan dollar. The extent to which this happens will be heavily dependent on which candidate is leading the polls.

Presidential elections in Indonesia next year are also worth watching, though continuity seems to be the approach of most candidates – so this may be less of an event risk. And we also have elections in India next year. Also, don’t rule out the impact of the US presidential election race, especially if Donald Trump is a candidate. Anti-China rhetoric is not a vote loser for either party in the run-up to the next US election and could add further volatility.

On the external front, with the region’s fortunes highly attuned to global trade flows, the continued stagnation in Europe, likely recession in the US, and Mainland China’s ongoing struggles aren’t likely to lead to a substantially better export outlook, though the bulk of the decline looks as if it is already through the pipeline. 2024 could see some modest improvement in volumes.

The apparent upturn in the semiconductor cycle could also be important for a number of economies in the region, not just the North Asian ones, though we would make a distinction between legacy semiconductors that are the mainstay of most of South East Asia, and the high-end chips that are driving the upturn, which is mainly limited to Taiwan and South Korea and could see the high-beta Korean won outperform. And in the background, the steady ratcheting up of US sanctions on Chinese trade in hi-tech components could dampen this cycle’s upswing.

Summing up the outlook then, it is a cautiously positive one, though the backdrop is far from trouble-free, with some substantial event risks along the way.

Capital flows: Balance of payments data for 3Q23 showed negative liabilities for Foreign Direct Investment – indicating actual outflows. This is a significant deterioration from the previous situation, where inflows had simply been slowing. It also suggests that the deterioration has further to run. In net terms, the flip to negative investment flows has been even more pronounced, which suggests that firms have used profit repatriation and intercompany transfers to take money out of China. There is a slightly more positive story for portfolio flows, which have reverted to something close to zero in 2023 after outflows in 2022. With global investor sentiment on China still challenging, this may be as good as it gets for a while.

Macro backdrop: The macro backdrop is extremely mixed. On a GDP basis, recent data has suggested that activity is firming slightly. Though the real GDP figures are flattered by an extremely negative deflator, the problems of the property sector are still weighing on the whole of the construction and manufacturing sectors while more timely PMI indices have recently worsened again, as has export data. The government seems to be becoming slowly more open to using a limited expansion of central government fiscal deficits to help cash-strapped local governments, which could include some targeted assistance for construction and infrastructure in early 2024. However, China’s property and fiscal issues are substantial and unlikely to be resolved in a year. So, although the 2023 GDP target of 5% looks like it will be achieved, we aren’t looking for anything more from GDP growth in 2024.

Central Bank and rates: The depreciation pressure that the CNY has experienced this year stopped the People’s Bank of China from undertaking any further policy rate cuts after the two mid-year cuts took the 7-day repo rate down to 1.80%, with the last cut coming in August. It is possible that if we see a broad-based turn in the USD, this frees up the PBoC to implement further rate cuts in 2024, but this is not our central view, and we expect rates to remain at 1.80% throughout 2024. Until such time as the USD does shift to a depreciation trend, we expect the central bank to support CNY at about a 7.30/USD rate. Like the INR, which has also been held at a stronger rate than regional peers, this will also likely limit the CNY appreciation once the USD turns.

Capital flows: In 2022, a strong pipeline of IPOs and overseas listings boosted capital inflows to India, which was helped in the second half of the year by a stronger equity backdrop. While this has not been such a strong story in 2023, the equity environment has again been supportive, and as we move into 2024, this is likely to remain the case and potentially even improve with the global and local rates environment becoming more supportive of risk assets. India’s financial account continues to be supported by strong portfolio inflows, direct investment and global and American depositary receipts stemming from overseas equity listings. 2024 brings a new feature as Indian government bonds are included in the JP Morgan Global bond index, EM (GBI-EM) for the first time. Fitch suggests that up to $24bn of passive inflows will occur between June 2024 and March 2025. At the margin, this should support the INR.

Macro backdrop: India has bucked global trends for a weakening economy and is on track to grow by about 7% in 2023 and should achieve a similar growth rate in 2024. Limited exposure to direct China trade and also to the downbeat semiconductor market have been helpful in 2023, though they also limit the upside to a recovery in 2024. The switch to cheaper Russian oil and gas supplies has shielded India from some of the worst of the fluctuations in inflation seen elsewhere in the region. Elections in 2024 could elicit some stronger government spending, though so far, India’s fiscal policy has remained firmly on track, and we don’t believe they will throw away their recently discovered credibility easily. Next year’s Union budget will likely continue the theme of modest deficit reduction and strong government spending on infrastructure and capital enhancements.

Central Bank and rates: At 6.5%, the Reserve Bank of India’s repo rate is not only one of the highest policy rates in the region, but it also has one of the widest spreads over the US Fed funds rate of any Asian central bank. This puts the RBI in a good position to begin to withdraw some of the tightening put in place once the global environment permits, and on the assumption that inflation continues to move in a benign range. The long-awaited turn in the USD should support the INR in 2024 but given how tightly the RBI has controlled the rupee since October 2022, the currency is already arguably stronger than justified relative to most of its peer currencies in the region, and we would anticipate a more modest appreciation during 2024 than its peers as a result. We suspect the RBI’s FX control is asymmetric, and that it won’t prevent the INR from appreciating slightly in the first half of 2024.

Capital flows: The KOSPI gained 8.9% year-to-date in 2023 despite several price corrections throughout the year. Foreigners came back to the market in the first half of the year but became net sellers in the third quarter. We are concerned that the recently announced ban on short selling may lower the investment appetite of foreign investors. However, Korean firms’ earnings expectations for 2024 are some of the highest among EM markets, so foreign inflows will likely be maintained. Korea has been added to the watch list for World Global Bond Index (WGBI) inclusion since last year and it may join the WGBI next year (at the earliest). Major initiatives, including extending trading hours and the gradual opening of onshore FX markets to improve accessibility to the KRW market will be executed from early next year. As we already argued in our recent research “KRW: the benefits of deliverability”, this is a positive factor providing support for the Korean won.

Macro backdrop: Korea’s economy will likely be caught in the crosscurrents of improving exports and softening domestic demand. The trade balance returned to surplus only recently, but the surplus will continue throughout next year mostly due to a solid bounce in semiconductor exports and a gradual recovery of China’s exports. We expect a turnaround in the semiconductor cycle. Korean chip makers, holding the largest market shares in the high-end chip market, will benefit the most from the continued US investment in the IT sector. Meanwhile, household consumption and construction investment will soften on the back of higher borrowing costs and likely weigh on growth.

BoK and rates: The Bank of Korea has paused its rate hike action since February 2023 and is expected to stay at the current level for policy rates of 3.5% for another couple of quarters. But the BoK is likely to enter an easing cycle from the second quarter of next year at the earliest, as inflation will drop back down into a 2% range again while consumption and investment will likely weaken due to prolonged tight credit conditions. However, considering the yield gap between the US and Korea, rate cuts will be quite limited and gradual.

2024 elections could boost growth but keep investors sidelined: Economic growth has been relatively robust, although momentum could be slowing as hinted by the 4.9% YoY 3Q GDP report. Lackluster global demand and falling commodity prices resulted in the export sector contracting in six out of the first nine months of the year. Meanwhile, government spending, which had been a key driver for growth since the pandemic, faded. Economic growth could rebound in the next few months with presidential elections scheduled for February 2024. However, foreign investors may opt to stay sidelined until Indonesia chooses a new president, which could translate into slower foreign investment flows.

Trade balance support faded as expected: With a key support for the rupiah less potent in 2023, the currency came under pressure, especially in the second half of the year. With the currency under pressure, Bank Indonesia (BI) implemented new foreign exchange rules geared towards supporting the currency, mandating exporters to deposit a portion of earnings domestically for a period of three months. Exports are likely to face another challenging year in 2024 with most major trading partners facing economic headwinds of their own. This could translate to sustained pressure on IDR well into 2024.

BI likely views rate hikes as a last resort: BI has been less aggressive in deploying rate hikes in 2023, opting to support the currency through other tools. The central bank rolled out regulations for exporters as well as various versions of bond purchases and issuance programmes (operation twist and SRBI) to steady the IDR with mixed results. Recent comments from BI Governor Perry Warjiyo suggest that BI prefers to refrain from further rate hikes, perhaps given concerns about growth momentum. With BI still maintaining a relatively tight interest rate differential over the Fed (75bp) the IDR could remain under pressure until the differential widens due to additional BI rate hikes or potential rate cuts from the Fed sometime in 2024.

Pent-up demand fading: Philippine economic growth remains robust although momentum appears to be slowing somewhat. Pent-up demand related to so-called “revenge spending” appears to have run its course with households focusing on rebuilding savings post-pandemic. Inflation remains a concern with headline inflation likely breaching the BSP’s inflation target of 2-4% for a third straight year in 2023. Stubbornly high inflation and elevated borrowing costs could translate to slower growth, which complicates the national government’s fiscal consolidation efforts with GDP growth expected to miss the 6-7% YoY growth target. Slow growth means the debt-to-GDP ratio will stay above 60%, which could limit foreign investment inflows.

Current account deficit narrows but remains a challenge. Recurring trade deficits have resulted in the Philippines running current account deficits for some time, indicating a fundamental depreciation trend for the PHP. A combination of weak exports and dependence on energy imports contribute towards making trade deficits chronic for the Philippines. Exports remain heavily dependent on electronics shipments and with global trade expected to remain subdued next year, we can expect the current account to remain in deep deficit. BSP expects the current account deficit to remain substantial for both 2023 ($11.1bn or 2.5% of GDP) and 2024 ($10.3bn or 2.1% of GDP). Thus, current account dynamics for the Philippines suggest that the PHP will be on the back foot unless foreign investment flows return to prop up the currency.

BSP hikes aggressively, signals more to come: The Bangko Sentral ng Pilipinas (BSP) has been aggressively hiking rates to deal with stubborn inflation. BSP has hiked a cumulative 450bp since mid-2022 and Governor Eli Remolona, who took over in July, signalled his openness to hiking rates further next year. Remolona has suggested that there might need to be additional tightening, hiking at an off-cycle meeting in a bid to safeguard the 2024 inflation target. BSP expects inflation to breach their 2-4% target and average 4.5% and thus we expect Remolona to hike further in the coming months given his hawkish tone.

Macro outlook: Growth momentum has been challenging in 2023. Soft global demand hit the export sector with non-oil domestic exports (NODX) in contraction throughout the year. Stalling NODX, in turn, impacted industrial output which has likewise been falling for all of 2023. One of the few bright spots for growth has been retail sales, bolstered in part by the pickup in visitor arrivals with global travel normalising. Some improvement in global demand coupled with the sustained recovery in visitor arrivals could help support growth next year. Singapore’s Tourism Board indicated that visitors from China recovered but are only 30% of pre-Covid levels, suggesting that there is room for further recovery for the tourism sector.

Inflation slows but remains elevated: Headline inflation has slowed from the peak of 7.5% in mid-2022 to settle at 4.1% YoY as of September. Despite the slowdown, headline inflation remains elevated and is likely weighing on domestic demand conditions. Core inflation, which is MAS’s preferred measure of inflation, tracked headline inflation’s decline, slipping to 3.0% YoY. Inflation could head closer to the MAS’s target of about 2%, however, the recent spike in volatility and uptick in global energy prices could mean that the decline back to target may stretch out into mid-2024.

MAS to meet more frequently beginning 2024: The MAS carried out two off-cycle meetings in 2022 on top of the two scheduled meetings to adjust its policy stance amidst accelerating inflation. The central bank recently announced it would be meeting more often beginning in 2024 to give them more flexibility with regard to policy decisions. MAS recently left settings untouched at the October 2023 meeting and we expect them to maintain their stance until core inflation is closer to their target of roughly 2%.

Capital flows: The second half of 2023 has been characterised by a run of negative net foreign investor position changes in Taiwanese equities. The TAIEX index remains up by 18.2% YTD in TWD but less than 13% in USD terms, and most of that gain came in the first half of 2023 with equities sliding slowly in the second half of 2023. The outlook for 2024 is brighter. There is clear evidence of a turn in the semiconductor cycle which underpins much of Taiwan’s economy and stock market. But near-term, there is also the presidential election in January, and this could be a period of strong volatility, perhaps exacerbated by Mainland Chinese threats, depending on which candidate appears to be leading the running. Heightened geopolitical tensions will likely weigh on risk assets at the beginning of the year and drive further capital outflows, but this could give way to a more favourable trend once this is out of the way.

Macro backdrop: Taiwan’s GDP started 2023 underwater as activity in the fourth quarter of 2022 contracted ahead of a further contraction in 1Q23. The rest of the year has been about clawing the economy back above zero, which it managed in 2Q23, though by 3Q23, GDP was only 2.3% higher than the same quarter a year ago and it has been slow-going. At least things no longer appear to be getting incrementally worse. On the export side, total USD exports now look to have stopped falling and year-on-year rates broke above zero in September, only to drop marginally below again in October. Exports of integrated circuits to mainland China have picked up strongly in recent months and the outlook for 2024 is looking slightly better, though with Europe skirting recession, the bulk of the US slowdown still to come, and Mainland China still struggling, any improvement in the macro story is likely to be modest, even with renewed appetite for high-end chips picking up.

Central Bank and rates: One positive note is that Taiwan’s inflation didn’t suffer anything like as big a spike as has been seen elsewhere in the region and is hovering at only around 3% YoY currently. As a result, Taiwan’s central bank has not needed to raise rates very far. From the pandemic trough of the discount rate at 1.125%, CBC-Taiwan has raised policy rates to just 1.875%, with the last hike coming back in March this year. This isn’t much higher than the prevailing rate pre-pandemic, though this also means that the prospects for easier monetary policy in 2024 are also therefore quite small. We look for rates to drop only to 1.7% by the end of 2024.

Source: ING

www.hellenicshippingnews.com