Central Financial institution Watch Overview:Federal Reserve policymakers have been energetic within the information for the pre

Central Financial institution Watch Overview:

- Federal Reserve policymakers have been energetic within the information for the previous week, with almost on a regular basis marked by feedback from a Board Member, a President, or the Chair himself. The drumbeat continues: rising US Treasury yields are an indication of the market’s confidence within the restoration, not an indication that inflation will run larger and warmer than anticipated.

- In the meantime, no feedback have been made about whether or not or not the $20 billion+ implosion of Archegos Capital Administration will influence the Fed’s resolution to finish the SLR.

- Total, the final week of March (and of 1Q’21) coinciding with the beginning of April (and of 2Q’21) sees little by the use of central financial institution price choices on the financial calendar.

Fed Getting into Talkative Stretch

On this version of Central Financial institution Watch, we’ll assessment the speeches revamped the previous week by varied Federal Reserve policymakers, together with the Fed Chair himself. Now in an prolonged interval between conferences – the following Fed price resolution is due out on April 28, then not once more till June 16 – we’re possible coming into a a number of month stretch whereby Fed policymakers are extra current within the day-to-day machinations of monetary markets.

For extra data on central banks, please go to the DailyFX Central Financial institution Launch Calendar.

Federal Reserve Continues Trying Previous Rising US Treasury Yields

Following the Fed’s March 17 assembly, US Treasury yields have calmed down – even when they continue to be considerably elevated relative to the beginning of this yr. However the drumbeat has continued amongst all of the policymakers heard over the previous week: rising US Treasury yields are an indication of the market’s confidence within the restoration, not an indication that inflation will run larger and warmer than anticipated. In actual fact, it might be the Fed’s resolute insistence on not bucking to bond vigilantes that finally caps bond market volatility.

So far, no feedback have been made about whether or not or not the $20 billion+ implosion of Archegos Capital Administration will influence the Fed’s resolution to finish the SLR; earlier on Tuesday, the NY Fed accepted $107.725 billion in its reverse repo operation throughout 35 bidders, up from $40.354 billion throughout 22 bidders.

March 23 – Powell (Fed Chair) says that “we have been dwelling in a world of robust disinflationary pressures — world wide actually — for 1 / 4 of a century,” so “we don’t suppose a one-time surge in spending resulting in momentary value will increase would disrupt that.”

Brainard (Fed governor) says that she sees “a affected person method primarily based on outcomes moderately than a preemptive method primarily based on the outlook” as being simpler for attaining Fed’s objectives.

Kaplan (Dallas Fed president) says “tright here had been some dots beginning will increase in 2022. And, you recognize, I’m a type of dots. Sure, completely.”

March 24– Powell (Fed Chair) notes that the Fed’s static forecast for decrease unemployment is definitely disguising “extremely fascinating” labor market positive aspects, saying that “we see participation increasing.”

Williams (NY Fed president) says “we’re nonetheless about 9 million jobs decrease than we had been a yr in the past within the U.S. financial system, so I feel that that’s going to maintain inflation pressures fairly low for a while.”

Bostic (Atlanta Fed president) says “2023 is the time we’re going to begin to be within the liftoff vary, and that basically hasn’t modified for me, even from December.” Moreover, he famous “my fashions actually have inflation above the two% stage for some time, such that at first of 2023 — within the early half and first half of it — nicely, I feel we’ll be positioned to maneuver coverage.”

March 25 – Powell (Fed Chair) says “As we make substantial additional progress towards our objectives, we’ll regularly roll again the quantity of Treasury and mortgage-backed securities we’re shopping for. After which within the longer run, we’ve set out a take a look at that can allow us to lift rates of interest.” Moreover, he famous that “we’ll — very, very regularly, over time, and with nice transparency, when the financial system has all however absolutely recovered — we can be pulling again the help that we supplied throughout emergency occasions.”

Bostic (Atlanta Fed president) says “let me say unambiguously that I’m not in the mean time considering we might want to take away coverage lodging quickly.”

Clarida (Fed Vice Chair) says “it will take a while for financial exercise and employment to return to ranges that prevailed on the enterprise cycle peak reached final February.” Moreover, he famous that “we are dedicated to utilizing our full vary of instruments to help the financial system till the job is nicely and actually carried out to assist be sure that the financial restoration can be as strong and fast as doable.”

March 26 – Harker (Philadelphia Fed president) says “our forecast is for inflation to creep as much as 2%, and our objective is to have it hit above 2% this yr. Our forecast is round 2.1%, however we don’t see it working uncontrolled.”

March 29 – Waller (Fed governor), when discussing monetizing the US debt, says “my objective at this time is to definitively put that narrative to relaxation. It’s merely improper. Financial coverage has not and won’t be carried out for these functions.”

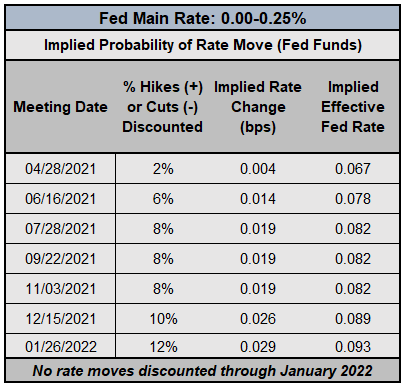

Federal Reserve Curiosity Charge Expectations (March 30, 2021) (Desk 1)

As such, following one other week of Fed officers downplaying inflation fears and suggesting that rising US Treasury yields mirror financial optimism, rate of interest expectations proceed to remain firmly anchored: Fed funds futures are pricing in a 88% likelihood of no change in Fed charges via January 2022. Whereas this can be a hawkish enchancment from the 93% likelihood in mid-March, it isn’t a cloth sufficient shift – but – to warrant a change in outlook.

Beneficial by Christopher Vecchio, CFA

Get Your Free USD Forecast

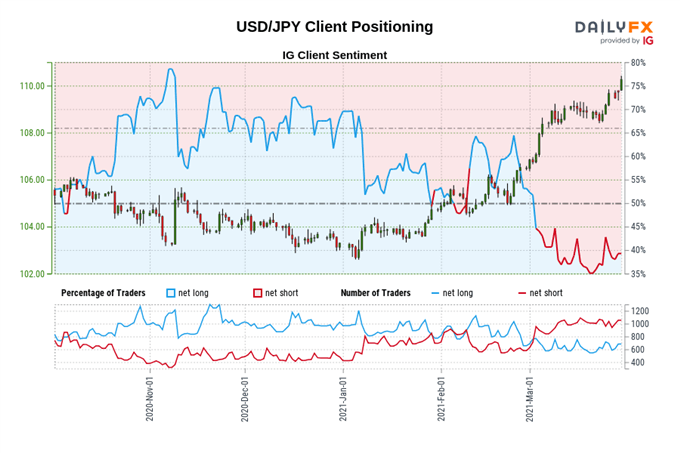

IG Shopper Sentiment Index: USD/JPY Charge Forecast (March 30, 2021) (Chart 1)

USD/JPY: Retail dealer knowledge exhibits 43.54% of merchants are net-long with the ratio of merchants brief to lengthy at 1.30 to 1. The variety of merchants net-long is 10.50% larger than yesterday and 21.28% larger from final week, whereas the variety of merchants net-short is 2.67% decrease than yesterday and 5.30% decrease from final week.

We sometimes take a contrarian view to crowd sentiment, and the very fact merchants are net-short suggests USD/JPY costs might proceed to rise.

But merchants are much less net-short than yesterday and in contrast with final week. Current adjustments in sentiment warn that the present USD/JPY value pattern might quickly reverse decrease regardless of the very fact merchants stay net-short.

Learn extra: FX Week Forward – Prime 5 Occasions: Biden Stimulus Speech; China Manufacturing PMI; UK GDP; US Manufacturing PMI; US NFP

— Written by Christopher Vecchio, CFA, Senior Foreign money Strategist

factor contained in the

factor. That is in all probability not what you meant to do!nn Load your utility’s JavaScript bundle contained in the factor as an alternative.www.dailyfx.com