S&P 500, FOMC, Dollar, EURUSD and USDJPY Talking Points:The Market Perspective: USDJPY Bearish Below 146; EURUSD Bullish Above 1.0000; Gold Beari

S&P 500, FOMC, Dollar, EURUSD and USDJPY Talking Points:

- The Market Perspective: USDJPY Bearish Below 146; EURUSD Bullish Above 1.0000; Gold Bearish Below 1,680

- The FOMC rate decision is this week’s top scheduled event risk and it is arguably the most important Fed meeting since the first 75bp hike

- Whether the Fed starts to taper its hawkish regime now or in then near future, the market is fully tuned into the guidance…as well as the evidence of underlying risks developing in the meantime

Recommended by John Kicklighter

Get Your Free Top Trading Opportunities Forecast

S&P 500 Exhibits FOMC Anticipation So Let’s Discuss the Scenario Table

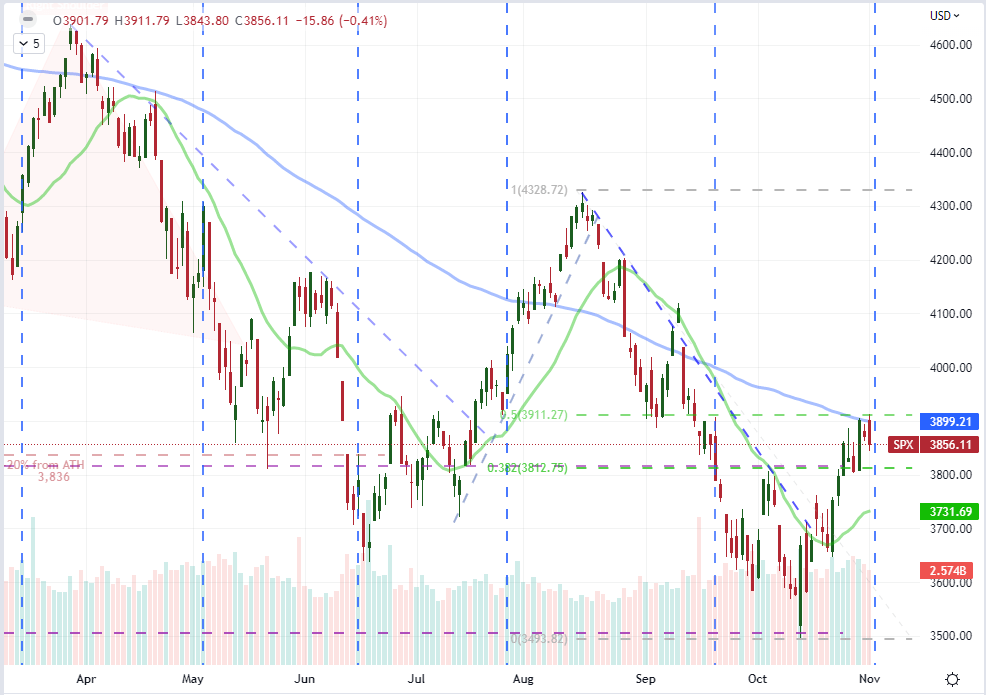

I’ve been following the track of risk assets for a long time, but the past week has been particularly informative. Speculative appetite against a backdrop of serious systemic risks moving forward has nonetheless managed to gain traction with the Dow Jones Industrial Average’s near-14 percent rally through October’s close notching the biggest statistical rally since 1976. That said, that same scale of enthusiasm does not seem to be a universal. There are certain assets that are severely behind the speculative curve, but the more closely related major US indices offer enough discrepancy to raise concern. The S&P 500’s ‘engulfing candle’ this past session shouldn’t be read into, but the proximity of the midpoint (’50 percent Fib’) to the August to October bear leg at 3910 should be monitored for technical influence. While the outcome of the US central bank’s policy decision requires the actual policy announcement to establish market reaction, the curb in activity leading into the event has held true to form.

Chart of S&P 500 with 20 and 100-Day SMAs as Well as Volume (Daily)

Chart Created on Tradingview Platform

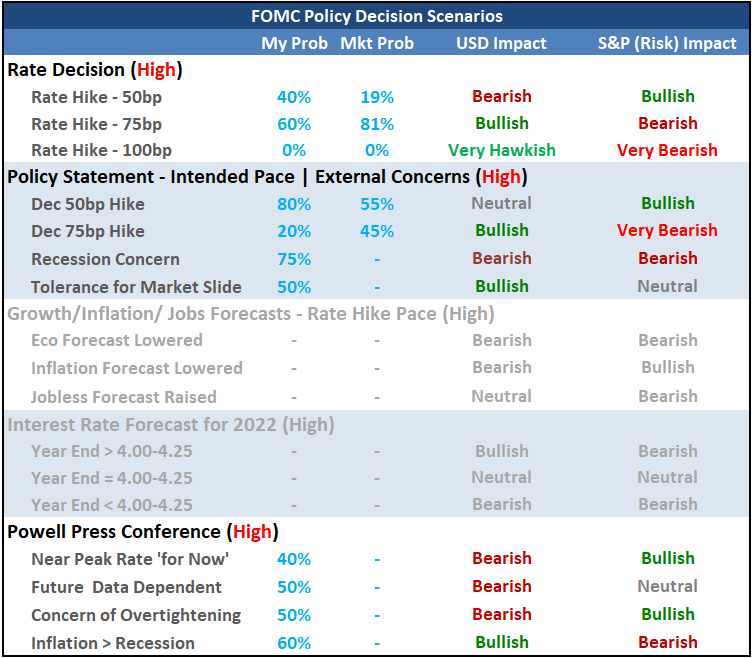

Whether or not the market commits to a trend waffles or it translates to ‘risk on’ or ‘risk off’ may depend heavily on the FOMC rate decision. The world’s largest central bank is due to announce its decision on contentious monetary policy at 18:00 GMT and the markets are clearly tuned in. With speculation, via Fed Fund futures and other outlets, pushing near certainty of yet another 75 basis point rate hike from group, the market’s response may be skewed. It is important not to take one element of this high-profile event as a definitive cue for speculative development. For example, a 75 bp rate hike is seen as the consensus in the market and among economists, therefore, such a large increase in monetary policy is unlikely to the secure the lift for the US currency and send US indices into a spiral. Sentiment will then need to draw upon the forecast for terminal rates and outlook for growth that will need to draw form the policy statement and Fed Chairman’s press conference remarks instead of the more black-and-white Summary of Economic Projections (SEP) that will need to wait until December for the next update.

Table of FOMC Scenarios with General Influence on the Dollar and S&P 500

Table Created by John Kicklighter

Event Risk Benchmark is the Fed but Themes Run Deeper

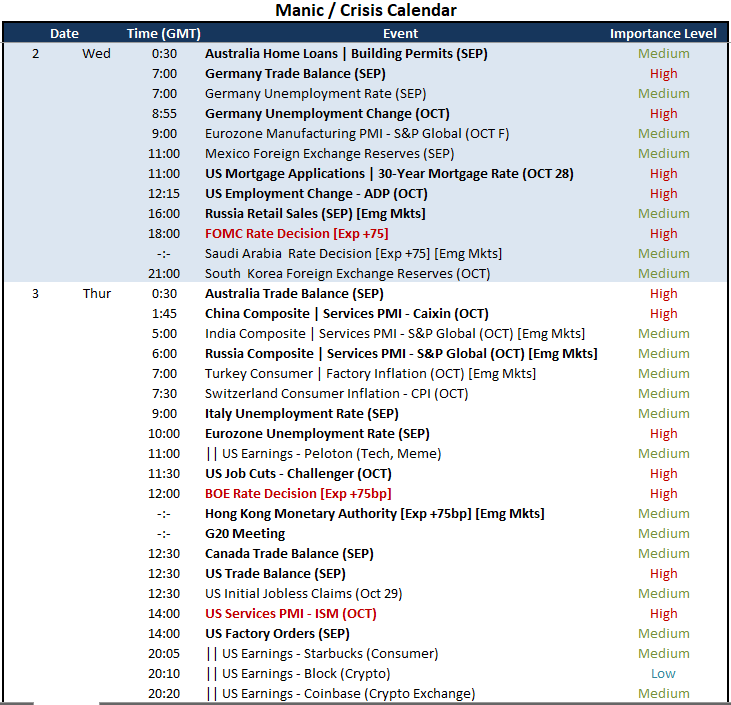

Looking over the next 48 hours of scheduled (and likely) event risk, it isn’t a stretch to suggest the Fed rate decisions Wednesday afternoon will capture most of the market’s attention. Whether the world’s largest central bank decided to extend its incredible tempo of 75bp rate hikes to a fourth consecutive meeting or not could seriously inform the global assessment of monetary policy that has already seen ‘disappointments’ (relative to market forecasts) from the Bank of England, Bank of Canada and Reserve Bank of Australia. This seems to frequent an occurrence of late to truly dispute the likelihood that central banks are throttling back on their ‘combat inflation at any cost’ attitude. However, I don’t think that rate potential is where the speculative conversation stops. The probability of recession remains the most important question on my macro list of question, and the FOMC minutes and Powell presser remarks should be monitored for such reference. Outside of that possibility, the ISM service sector activity report on Thursday is a more timely measure of US economic health…and the manufacturing report surprised by holding its head above the growth line.

Critical Macro Event Risk on Global Economic Calendar for Next 48 Hours

Calendar Created by John Kicklighter

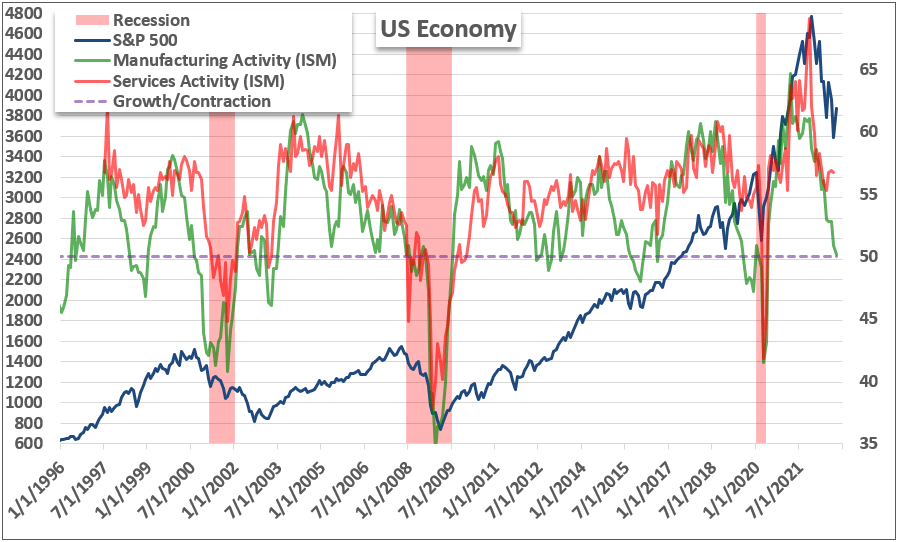

Monetary policy is an important contributor to our assessment of speculative enthusiasm – especially after fueling more than a decade of speculative reach on the basis that accommodative policy would supplement questionable fundamental backdrop – but there are more uncertain matters moving forward. The chances of a true recession remain a high probability but a surprisingly controlled influence on price action. As the course to economic consolidation becomes more explicit, the ability to navigate around the troubling reality will fall apart. It is for that reason that I hold the ISM service sector report in high regard. The cross section of the US economy accounts for approximately three-quarters of output (eg growth) and employment. Should the Thursday release look anything like the manufacturing survey’s slip to the cusp of the 50.0 growth/contraction boundary, the implications will be difficult to overlook.

Chart of the ISM Service and Manufacturing PMIs Overlaid with S&P 500 and US Recessions (Monthly)

Chart Created by John Kicklighter with Data from ISM

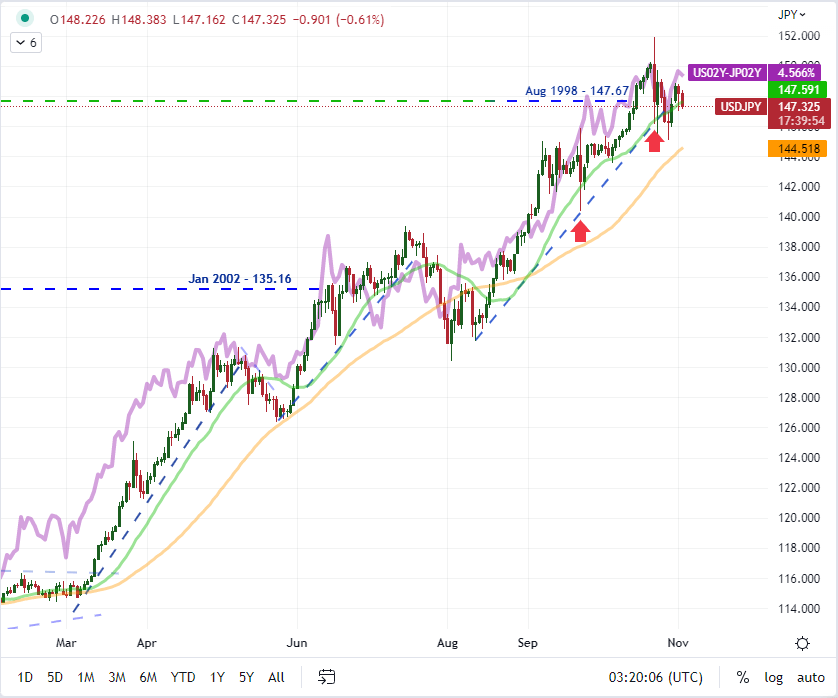

Dollar Pairs to Watch: USDJPY and EURUSD

Risk assets are top of my list for measures to watch at any given time as the reflection is a systemic one for the financial system. That said, the fundamental perspective from key Dollar pairs may be just as insightful moving forward. As we await the Fed’s decision on whether to hike 75 bps or not at this meeting and how far they intend to extend the regime beyond, there is perhaps no more uniformly aligned FX pair the Fed’s bearings than USDJPY. After the BOJ made clear that they would be keeping to their yield curve control policy, all of the onus of market determination seems to shift back onto the Dollar and its rate backdrop. Should the US 2-year yield soften because the Fed signals a lower plateau in the foreseeable future, it may offer the exchange rate relief that the Japanese Ministry of Finance failed to manufacturing this past month.

Recommended by John Kicklighter

How to Trade USD/JPY

Chart of USDJPY (Daily)

Chart Created on Tradingview Platform

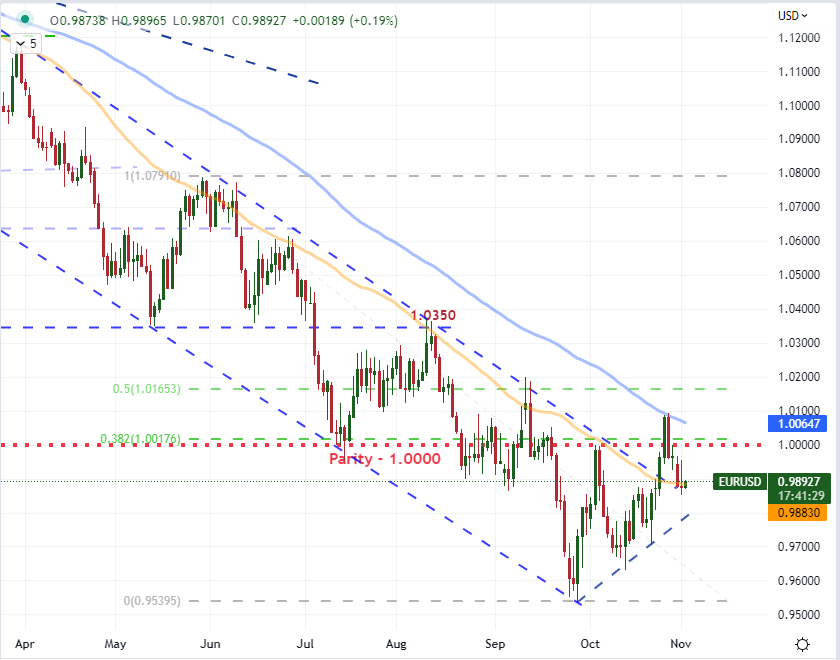

If we are talking about the bearing and health of the Dollar, it goes without saying that we should also be keeping tabs on the most liquid exchange rate in the market (recently reaffirmed by the Bank for International Settlements’ recently released triennial report). EURUSD crushed a recovery this past session following the mixed back of JOLTS and ISM manufacturing data. Perhaps it was enough to reassure Fed hikes moving forward without spurring genuine hope for growth potential. With the ECB still playing catch up in its fight against inflation, this is a pair that positions any Fed moderation in tempo against an ‘late comer’ counterpart.

Recommended by John Kicklighter

How to Trade EUR/USD

Chart of EURUSD Overlaid with Eurozone-US 2-Year Yield Spread (Daily)

Chart Created on Tradingview Platform

Trade Smarter – Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

Subscribe to Newsletter

element inside the

element. This is probably not what you meant to do!Load your application’s JavaScript bundle inside the element instead.

www.dailyfx.com