Affect of Financial and Fiscal Coverage on FX Markets, Key Central Financial institution Charge Selections From ECB, BoC and Fed,

Affect of Financial and Fiscal Coverage on FX Markets, Key Central Financial institution Charge Selections From ECB, BoC and Fed, US Greenback, Euro, Canadian Greenback Evaluation – TALKING POINTS

- How do financial and monetary coverage measures impression forex markets?

- What’s the Mundell-Fleming mannequin and why does it matter for FX merchants?

- How has coverage from the Fed, ECB and BOC impacted USD, EUR and CAD?

MARKETS HAVE PASSED THE POLITICAL EVENT HORIZON

For international trade (“foreign exchange” or “FX”) merchants, the fixed background noise that politics represents is an inescapable blackhole. Conventional media drowns in punditry, whereas social media drowns in puns. It doesn’t matter what asset class you’re buying and selling both.In current years, even a single tweet from a politician has had the capability to maneuver not solely currencies but additionally bonds,commodities, and equities.

In an more and more fractious panorama, merchants want a framework by which to interpret info and perceive political developments as they occur. In any case, politics can turn out to be coverage after sufficient effort and time. To this finish, FX merchants want a method to interpret info and political developments within the context of how fiscal coverage may change and the way which may impression their portfolios.

Market individuals want to concentrate to greater than simply fiscal coverage, nonetheless. With central financial institution exercise having gained appreciable traction in the course of the Nice Recession and thereafter, financial coverageseems to be a strong lasting affect on markets. Subsequently, FX merchants want a viable framework to investigate each fiscal and financial coverage in tandem.

ECONOMISTS HAVE A SOLUTION BEYOND THE IS-LM MODEL

Luckily, one such framework exists: IS-LM-BP mannequin, or what’s recognized colloquially because the Mundell-Fleming mannequin. By way of this framework, FX merchants can analyze how directional adjustments in fiscal coverage (e.g. adjustments in taxes or authorities spending) and financial coverage (e.g. adjustments in rates of interest) work together to supply varied market outcomes.

Earlier than we delve into the framework, a little bit of background historical past on the Mundell-Fleming mannequin.

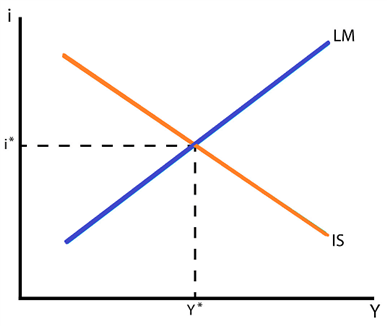

Mundell-Fleming is an extension of IS-LM, which itself is an equilibrium mannequin utilized by economists to have a look at the connection between rates of interest (the actual rate of interest, “i” on the vertical axis of the chart under) and financial development (actual gross home product, “Y” on the horizontal axis).

IS-LM Curve – Curiosity Charges and Financial Progress (Chart 1)

With out going too far down the tutorial rabbit gap, there are two takeaways of the IS-LM mannequin that carryover into understanding the Mundell-Fleming mannequin.

First, that the downward sloping IS curve demonstrates that as the extent of rates of interest fall, the extent of financial exercise rises. That is intuitive: the extra readily credit score is offered, the extra financial exercise will flourish.

Second, the upward sloping LM curve demonstrates that as financial exercise rises, the extent of rates of interest rise too. That is additionally intuitive: stronger financial exercise provokes inflation and better bond yields in response.

THE IS-LM MODEL IS INAPPROPRIATE FOR MODERN ECONOMIES

Why is the IS-LM mannequin inadequate for merchants? The IS-LM mannequin is a foundational idea that in the end results in the basic AS-AD supply-demand mannequin. However the IS-LM mannequin is relevant for self-sufficient and/or closed economies; such a framework just isn’t applicable for a globalized world the place open economies co-dependent on each other are the norm. We have to transfer past for a extra full framework.

Recommended by Christopher Vecchio, CFA

Forex for Beginners

THE MUNDELL-FLEMING MODEL WORKS BETTER FOR OPEN ECONOMIES

Within the early-1960s, economists Robert Mundell and J. Marcus Fleming every produced enchancments on the unfinished IS-LM mannequin. Developed independently from each other however finally synthesized into one unified thought, the IS-LM-BP mannequin incorporates capital movement into the equation.

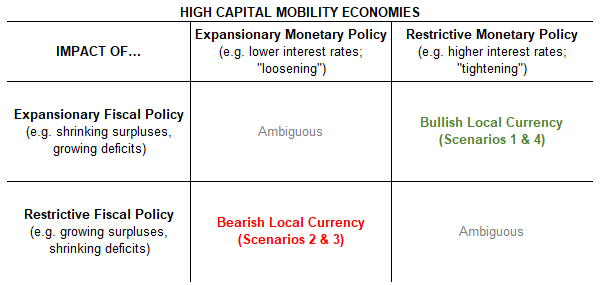

There are two totally different capital movement constraints inside the IS-LM-BP, or Mundell-Fleming mannequin. Nations both seeexcessive or lowcapital mobility. Relying upon which it’s, totally different coverage mixes result in divergent reactions in the markets.

As a rule of thumb, developed nations and their currencies (e.g. the US, UK, Eurozone, Japan, and so on.) have excessive capital mobility. Alternatively, rising markets and their currencies (e.g. Brazil, China, South Africa, Turkey, and so on.) have low capital mobility.

For the sake of this dialogue, we are going to take a look at the Mundell-Fleming mannequin via the lens of excessive capital mobility economies solely, and in consequence, try to set forth a framework to grasp how totally different fiscal and financial coverage mixes impression the most important currencies just like the US Greenback, Euro, British Pound and Japanese Yen.

In a follow-up report, we are going to present the implications of the Mundell-Fleming mannequin via the lens of low capital mobility economies and the ensuing impression of coverage adjustments for rising market currencies.

DIFFERENT POLICY MIXES LEAD TO DIVERGENT REACTIONS IN MARKETS

For top capital mobility economies, there are successfully 4 totally different units of coverage shifts that may provoke a response in FX markets. They’re:

- Situation 1: Fiscal coverage is already expansionary + financial coverage turns into extra restrictive (“tightening”) = Bullish for the native forex

- Situation 2: Fiscal coverage is already restrictive + financial coverage turns into extra expansionary (“loosening”) = Bearish for the native forex

- Situation 3: Financial coverage already expansionary (“loosening”) + fiscal coverage turns into extra restrictive = Bearish for the native forex

- Situation 4: Financial coverage is already restrictive (“tightening”) + fiscal coverage turns into extra expansionary = Bullish for the native forex

It is very important be aware that for an economic system like the US and a forex just like the US Greenback, every time fiscal coverage and financial coverage begin trending in the identical route, there may be typically an ambiguous impression on the forex.

In different phrases, when seen via the framework of the Mundell-Fleming mannequin, when each fiscal and financial coverage are expansionary, or when each fiscal and financial coverage are restrictive, that forex is unlikely to see a big directional transfer within the close tofuture.

As a substitute, armed with this perception, merchants anticipating a interval of trendless oscillation in a given forex might be inspired to put aside momentum- and trend-based methods to undertake an method optimized for range-bound situations.

Mundell-Fleming Mannequin Framework for Excessive Capital Mobility Economies (Desk 1)

Listed here are 4 examples in previously decade from varied excessive capital mobility economies from world wide that illustrate how utilizing the Mundell-Fleming mannequin as a framework for understanding politics and central banks would have given a dealer an analytical edge.

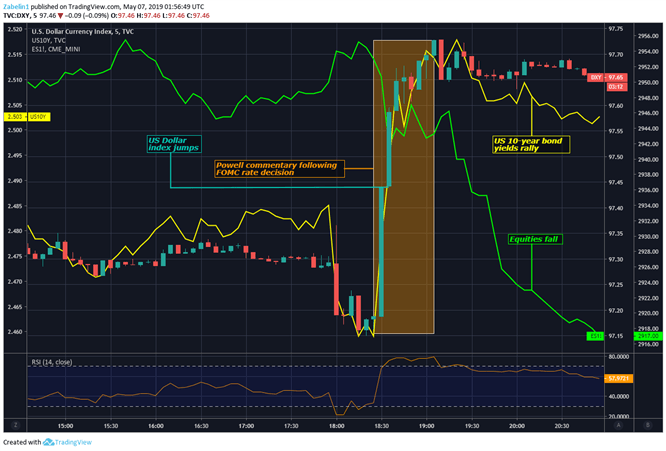

Situation 1 – FISCAL POLICY LOOSE; MONETARY POLICY BECOMES TIGHTER

On Might 2, 2019 – following the FOMC resolution to carry charges on the 2.25-2.50 vary – Fed Chairman Jerome Powell stated that the comparatively smooth inflationary stress within the economic system was “transitory”. The implication behind this was that whereas value development was under what central financial institution officers had been hoping for, it could quickly speed up.

The implicit message was then a decreased likelihood of a minimize sooner or later, on condition that the basic outlook was judged to be stable and the general trajectory of US financial exercise seen to be on a wholesome path. The impartial tone struck by the Fed was comparatively much less dovish than what markets had anticipated. This would possibly then clarify why in a single day index swaps for a Fed fee minimize by the top of the 12 months fell from 67.2 p.c all the way down to 50.9 p.c after Powell’s feedback.

In the meantime, the Congressional Price range Office (CBO) is forecasted a rise within the deficit over the following three years, overlapping the central financial institution’s tightening cycle. This additionally came towards the backdrop of hypothesis a few bipartisan fiscal stimulus plan. In late April, key policymakers introduced plans for a US$2 trillion infrastructure program.

Recommended by Christopher Vecchio, CFA

Improve your trading with IG Client Sentiment Data

The mixture of expansionary fiscal coverage and financial tightening made the case for a bullish outlook for the US Greenback. The fiscal package deal was anticipated create jobs and enhance inflation, thereby nudging the Fed to boost charges. Because it occurred, the Buck added 6.2 p.c towards a mean of its main forex counterparts over the following 4 months.

Situation 1: DXY, 10-Yr Bond Yields Rise, S&P500 Futures Fall (Chart 2)

Situation 2 – FISCAL POLICY TIGHT; MONETARY POLICY BECOMES LOOSER

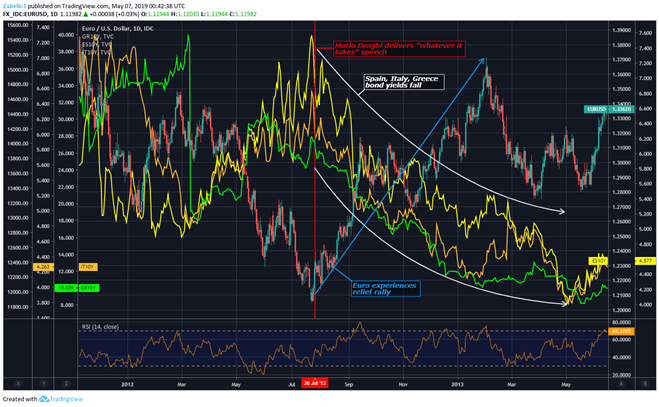

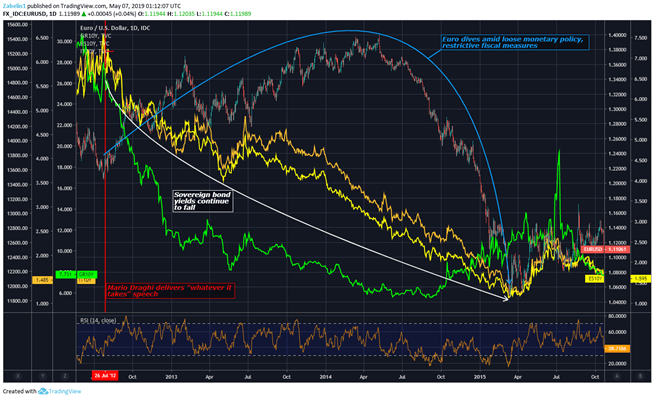

Theworld monetary disaster in 2008 and the Nice Recession that adopted rippled out worldwide and destabilized Mediterranean economies. This stoked worries about a region-wide sovereign debt disaster as bond yields in Italy, Spain and Greece climbed to alarming ranges.

Traders started to lose confidence within the potential of those governments to service their debt and demanded the next yield for incurring what seemed to be the next danger of default. The Euro was in ache amid the chaos and suffered as doubtsemerged about its very existence within the occasion that the disaster would power the unprecedented departure of a member state from the Eurozone.

In what is taken into account to be probably the most well-known moments in monetary historical past, European Central Financial institution (ECB) President Mario Draghi delivered a speech in London on July 26, 2012 which many would come to see as the pivotal second that saved the single forex. He stated that the ECB is “able to do no matter it takes to protect the Euro. And imagine me,” he added,“it will likely be sufficient.” This speech calmed European bond markets and helped carry yields again down.

Recommended by Christopher Vecchio, CFA

Top Trading Lessons

The ECB additionallycreated a bond-buying program referred to as OMT (for “Outright Financial Transactions”). It was aimed at lowering stress in sovereign debt markets, providing reduction to distressed Eurozone governments. Whereas OMT was by no means used, its mere availability helped becalm jittery buyers.On the similar time, a lot of the troubled Euro space states adopted austerity measures to stabilize authorities funds.

Whereas the Euro initially rose as worries about its collapse receded, the European forex would depreciate considerably towards the US Greenback over the course of the next three years. By March 2015, it had misplaced over 13 p.c of its worth. When inspecting the financial and monetary arrange, it turns into fairly clear why.

Situation 2: Euro Sighs Reduction – Sovereign Bond Yields Fall as Insolvency Fears are Quelled (Chart 3)

Austerity measures in lots of Eurozone nations restricted their authoritiess’ potential to present fiscal stimulus that may need assisted create jobs and enhance inflation. On the similar time, the central financial institution was easing coverage as a method to alleviate the disaster. Consequently, this mixture pressured the Euro decrease towards most of its main counterparts.

Situation 2: Euro, Sovereign Bond Yields Fall (Chart 4)

Situation 3 – MONETARY POLICY LOOSE; FISCAL POLICY BECOMES TIGHTER

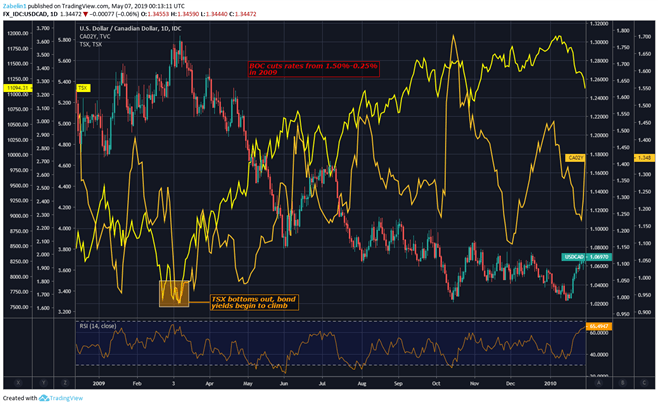

On the early phases of the Nice Recession, the Financial institution of Canada (BOC) minimize its benchmark rate of interest from 1.50 to 0.25 p.c as a method to ease credit score situations, restore confidence and revive financial development. Counter-intuitively, the yield on 10-year Canadian authorities bonds started to rise. This rally got here proper across the similar time as Canada’s benchmark TSX inventory index established a backside.

Situation 3: USD/CAD, TSX, Canadian 2-Yr Bond Yields (Chart 5)

The following restoration of confidence and restoration in share costs was mirrored buyers’ shifting desire for riskier, higher-returning investments (like shares)from comparatively safer different (like bonds). This reallocation of capital despatched yields greater regardless of the central financial institution’s financial easing. The BOC then started to boost charges anew and introduced them as much as 1.00 p.c, the place they remained for the following 5 years.

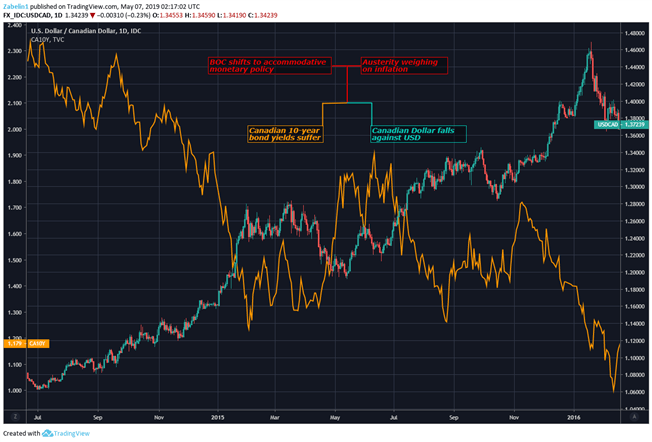

Throughout this time, Prime Minister Stephen Harper applied austerity measures to stabilize the federal government’s funds amid the world monetary disaster. The central financial institution then reversed course and minimize charges again to 0.50 p.c by July 2015. Each CAD and native bond yields suffered as financial coverage was loosened whereas the capability for fiscal coverage help was constrained. Because it occurs, chopping again authorities spending at this tough time ended up costing Mr Harper his job. Justin Trudeau replaced him as Prime Minister following a victory within the 2015 normal election.

Situation 3: USD/CAD, Canada 2-Yr Bond Yields (Chart 6)

Situation 4 – MONETARY POLICY TIGHT; FISCAL POLICY BECOMES LOOSER

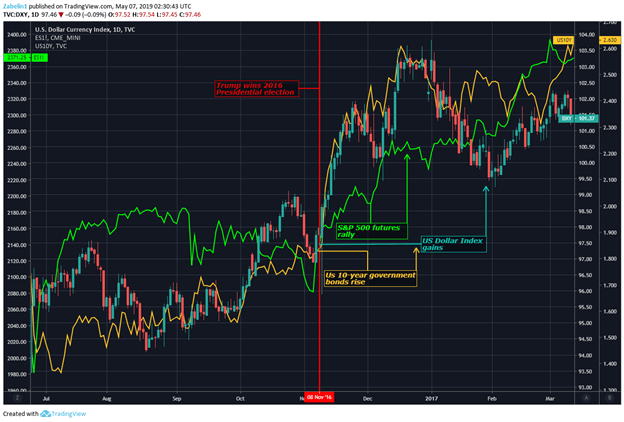

After Donald Trump was proclaimed the victor within the 2016 USpresidential election, the political panorama and financial backdrop favored a bullish outlook for the US Greenback. With the the Oval Workplace and each homes of Congress thus managed by the Republican Social gathering, the markets appeared to conclude that scope for political volatility had was considerably decreased.

This made the market-friendly fiscal measures proposed by candidate Trump in the course of the electionseem extra prone to be applied. These included tax cuts, deregulation and infrastructure constructing. Traders appeared to miss threats to launch commerce wars towards high buying and selling companions akin to China and the Eurozone, at the least for the time. On the financial facet, central financial institution officers raised charges on the tail finish of 2016 and had been seeking to hike once more by at the least 75 foundation factors via 2017.

With scope for fiscal growth and financial tightening in sight, the US Greenback rallied alongside native bond yields and equities. This got here as company earnings expectations strengthened alongside the outlook for broader financial efficiency, which likewise stoked finest on firmer inflation and thereby on a hawkish response from the central financial institution.

Situation 4) US Greenback Index (DXY), S&P 500 Futures, 10-Yr Bond Yields (Chart 7)

LIMITATIONS OF THE MUNDELL-FLEMING MODEL

For a few years, the IS-LM-BP or Mundell-Fleming mannequin was a method to measure the impression of adjustments in coverage for small open economies. In flip, many economists counsel that economies with important sufficient scale might not adhere to the “guidelines” that “regular” economies should take care of, and in consequence, the IS-LM mannequin was deemed preferable.

However previously decade, new analysis has confirmed that the framework introduced in IS-LM-BP the truth is captures the state of the modern globalized economic system higher than the IS-LM mannequin alone. Evidently, opinions on the topic abound throughout the spectrum of economists.

Finally, there is no such thing as a ‘Holy Grail’ analytical framework that may yield the right perception each single time, whatever the political context or the standing of the financial system. There could also be occasions that occasions produce market reactions that may’t be readily understood or defined.

And but, not having a framework for the right way to interpret how politics and central banks are transferring FX markets could be irresponsible. Utilizing the Mundell-Fleming mannequin as a information might assist merchants filter out the noise of the day-to-day information cycle, serving to them higher perceive and virtually react to info shaping FX market value tendencies.

— Written by Christopher Vecchio, CFA, Senior Foreign money Strategist and Dimitri Zabelin, Foreign money Analyst