{kind=link}

The global atmosphere of ‘currency depreciation trades’ has become prominent, with low-debt currencies such as the Swedish krona and Swiss franc beginning to correlate with precious metals. The Bank of Japan’s interest rate hikes still fail to stop yen carry trades, making precious metals the biggest winner.

A strategist stated that gold’s record high proves the so-called “currency devaluation trade” has restarted.

Robin Brooks, senior economist at the Brookings Institution and former chief foreign exchange strategist at Goldman Sachs Group, made the comments as gold surpassed $4,400 per ounce.

Brooks noted in a Substack post that this rise in gold prices was a direct result of the Federal Reserve’s latest rate cut and market concerns over debt monetization, or central bank purchases of government-issued bonds.

Brooks noted in a Substack post that this rise in gold prices was a direct result of the Federal Reserve’s latest rate cut and market concerns over debt monetization, or central bank purchases of government-issued bonds.

Since 2025, the return on international spot gold has reached 68%; driven by many of the same factors, international spot silver also hit a record high on Monday, with year-to-date gains now approaching 140%. Escalating tensions in Venezuela and Ukraine’s attacks on Russian ports and shipping have further enhanced gold’s appeal as a safe-haven asset in recent days.

In Brooks’ view, the breakout in gold and broader precious metals was triggered by Fed Chair Powell’s dovish remarks at the Jackson Hole conference on August 22 and the 25-basis-point rate cut on December 10. Commodity traders are also anticipating further rate cuts from the Federal Reserve.

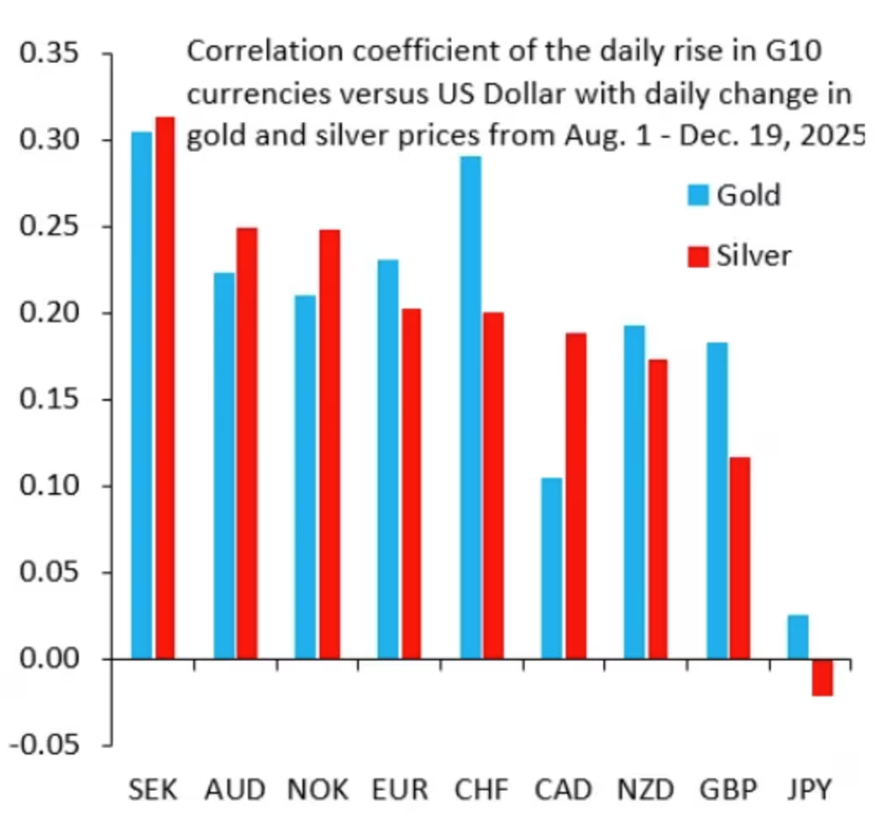

However, he pointed out that this “currency devaluation trade” is not limited to precious metals, emphasizing that even currencies with low debt levels, such as the Swedish krona and Swiss franc, have begun to show correlations with gold and silver.

He presented a chart illustrating the correlation between G10 currency performance against the US dollar and the performance of gold and silver.

He argued that the strengthening of the Swedish krona is a result of the “currency devaluation trade” – historically, the Swedish krona has been a volatile currency without safe-haven attributes.

Brooks also noted that while the US dollar appears relatively stable on the surface and unaffected by the “currency devaluation trade,” its strength against the extremely fragile yen has masked its broad weakness against a basket of currencies.

For Jeroen Blokland, economist and fund manager of the Blokland Smart Multi-Asset Fund, the surge in gold prices is partly driven by ongoing yen carry trades – where investors short the yen to finance long positions in higher-risk assets in other regions. Precious metals are currently the primary target for such investment choices.

Blokland wrote in a post on the X platform that last week’s interest rate hike by the Bank of Japan (raising the policy rate to 0.75%, the highest level since 1995) has not ended carry trades. He believes that inflation will remain structurally high, and the interest rate differential between Japan and the US remains sufficiently large to encourage traders to borrow yen for purchasing the US dollar or other high-yield/high-risk assets.

The yield on Japan’s 10-year government bonds has continued to soar, nearly doubling this year to reach 2.08%.

news.futunn.com