US Recession Watch Overview:The US Treasury yield curve has steepened in latest weeks (long-end charges rising sooner than short

US Recession Watch Overview:

- The US Treasury yield curve has steepened in latest weeks (long-end charges rising sooner than short-end charges), however that may not imply that the US financial system is out of the woods from the coronavirus pandemic.

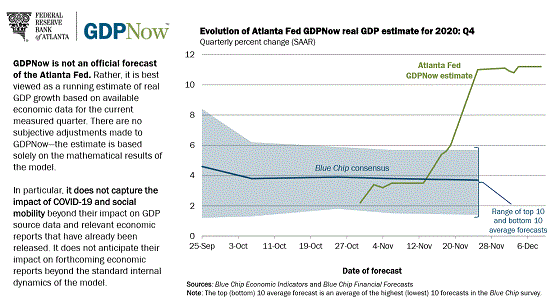

- This fall’20 Atlanta Fed GDPNow initiatives an +11.2% actual quarterly development charge, however knowledge momentum is slowing, and it’s attainable that failure by the US Congress to comply with fiscal stimulus will handicap the financial system in Q1’21.

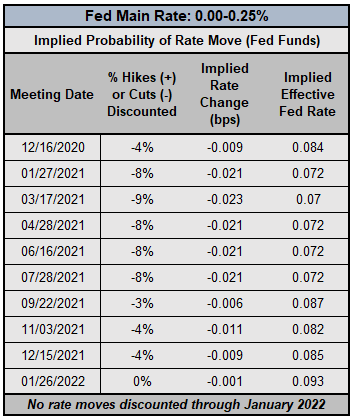

- Merchants proceed to anticipate no change in rates of interest by the Federal Reserve by means of January 2022; the Fed has promised to maintain charges low by means of 2023.

Making Sense of US Financial Information

The US financial system is within the midst of a record-setting restoration, or is about to fall again into recession – relying upon who you ask. Timeframe issues. With only some weeks left in This fall’20, it seems that one other sturdy quarter is within the books: the Atlanta Fed GDPNow development tracker is suggesting that we might see an actual quarterly development charge round +11.2%, per obtainable knowledge by means of December 9. Amid the preliminary coronavirus vaccine deployments, the US Treasury yield curve is at its steepest place in weeks.

And but, one thing is amiss. US financial knowledge is transferring within the flawed course. The Citi Financial Shock Index, a gauge of financial knowledge momentum, is at present sitting at +75.8, down by greater than -72% from its excessive set in July at +270.8. For the primary time since early-October, US preliminary jobless claims are again above 800Okay per week. The November US jobs report was a lot weaker than anticipated.

Atlanta Fed GDPNow This fall’20 US GDP Estimate (December 14, 2020) (Chart 1)

The trope “winter is coming” could also be overused, however its an apt flip of phrase right here. The window with which to positively affect Q1’21 GDP is slowly closing as US political leaders stay caught in gridlock in Washington, D.C. Hopes of a ‘blue wave’ have floundered, and together with them, religion in a signficant fiscal stimulus bundle through the interregnum.

As an alternative, the US Congress can barely move a finances to maintain the lights on for greater than per week. The fiscal spending bundle, if it comes collectively, seems to be like it’ll clock in round $900 billion on the excessive finish, a far cry from the $2 trillion that President-elect Joe Biden was promising on the marketing campaign path (though, if Senate Democrats pull out a miracle in Georgia, that large stimulus push could come in spite of everything; keep tuned).

Fed Might Be Influencing Worth Motion

The December Fed coverage assembly set to conclude on December 16 brings concerning the potential for an additional adjustment to their stimulus program, given that we are going to see the quarterly Abstract of Financial Projections. Whereas a coronavirus vaccine deployment could also be decreasing threat over the long-run, the upfront financial outlook has soured. However that doesn’t essentially imply that the Fed will act once more.

Federal Reserve Curiosity Charge Expectations (December 14, 2020) (Desk 1)

With no detrimental charges on the horizon and a FOMC that has mentioned explicitly that rates of interest will likely be low by means of 2023, it might be the case that merchants have pushed up US yields – steepening the yield curve – in anticipation over forthcoming disappointment on the coverage entrance. Expectations for an enhancement to the Fed’s QE program have subsided; it was beforehand anticipated {that a} shift to purchasing extra long-dated bonds may happen in December. As this expectation of a serious purchaser in bond markets has subsided, costs have fallen, and yields have risen.

Utilizing the US Yield Curve to Predict Recessions

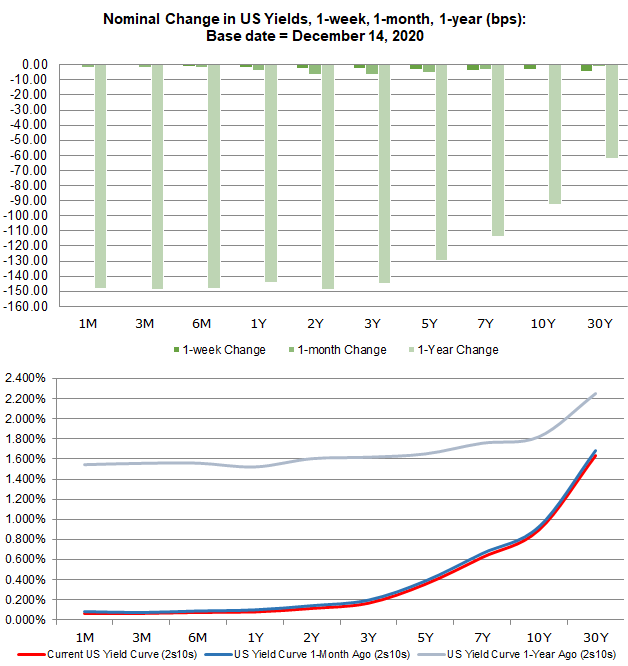

The US Treasury yield curve stays normalized – long-end yields are increased than short-end yields – however we keep that the yield curve shouldn’t be an correct reflection of the state of the US financial system. Traditionally, the comparatively sooner rise by long-end yields in comparison with short-end yields happens throughout instances of anticipated financial growth, so merchants could also be liable to interpret the yield curve actions as an indication that market individuals imagine that the worst interval of uncertainty across the coronavirus pandemic is over.

US Treasury Yield Curve: 1-month to 30-years (December 14, 2020) (Chart 2)

The Fed’s efforts to flood the market with liquidity have depressed short-end yields, serving to hold intact an artificially steep of the US yield curve. The degradation of US financial knowledge momentum coupled with the alarming surge in COVID-19 circumstances, in mixture of day by day checks, deaths, and hospitalizations, means that the US yield curve is mendacity, once more. That the US yield curve is steepening and the net-result is a weaker US Greenback is a serious crimson flag that one thing is amiss.

In any case, that sounds quite a bit like a sovereign debt drawback akin to what was seen through the top of the Eurozone disaster, no? The soundbites on the time had been, “Italian/Spanish/Portuguese yields spike, Euro falls.” Time will inform if the US yield curve shouldn’t be signaling increased development, however as an alternative threat of sovereign credit score stress.

A Refresher: Why Does the US Yield Curve Matter?

Market individuals use yield curves to gauge the connection between threat and time for debt at numerous maturities. Yield curves will be constructed utilizing any debt, be it AA-rated company bonds, German Bunds, or US Treasuries.

A “regular” yield curve is one wherein shorter-term debt devices have a decrease yield than longer-term debt devices. Why although? Put merely, it’s tougher to foretell occasions the additional out into the longer term you go; buyers should be compensated for this extra threat with increased yields. This relationship produces a constructive sloping yield curve.

When a authorities bond yield curve (like Bunds or Treasuries), numerous assessments concerning the state of the financial system will be made at any cut-off date. Are short-end charges rising quickly? This might imply that the Fed is signaling a charge hike is coming quickly. Or, that there are funding issues for the federal authorities. Have long-end charges dropped sharply? This might imply that development expectations are falling. Or, it might imply that sovereign credit score threat is receding. Context clearly issues.

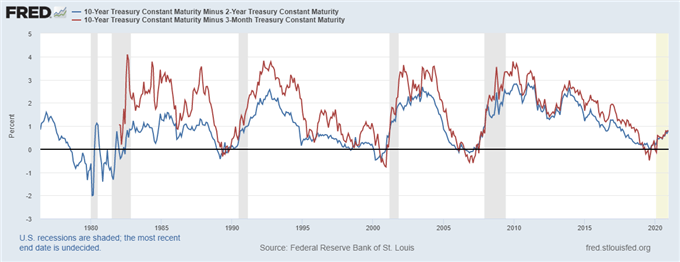

US Treasury Yield Curves: 3m10s and 2s10s (1975 to 2020) (Chart 3)

There may be an educational foundation for yield curve evaluation. In 1986, Duke College finance professor Campbell Harvey wrote his dissertation exploring the idea of utilizing the yield curve to forecast recessions. Professor Campbell’s analysis famous that the US yield curve must invert within the 3m10s for not less than one full quarter (or three months) with a view to give a real predictive sign (because the 1960s, a full quarter of inversion has predicted each recession accurately).

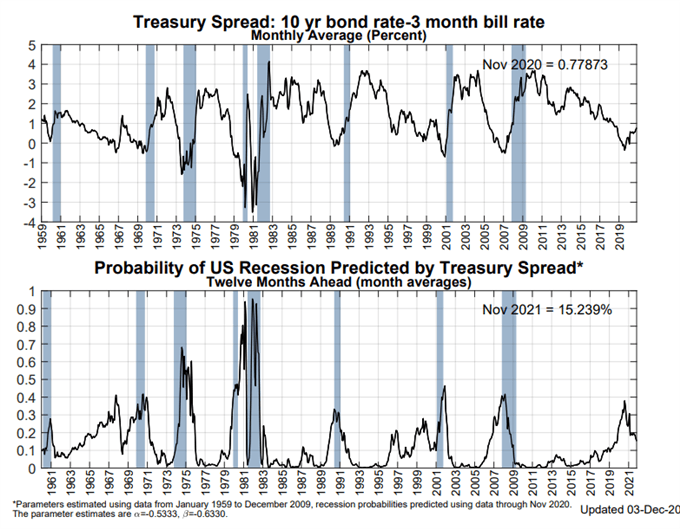

NY Fed Recession Chance Indicator (December 14, 2020) (Chart 4)

In mixture, there’s at present a 15.2% likelihood of a US recession within the subsequent 12-months, per the NY Fed Recession Chance Indicator. This tracker by no means eclipsed 40% through the spring, at the same time as Q2’20 GDP was actually the worst quarter in US financial exercise. As soon as extra, the US yield curve is hiding the reality, masking what’s going to possible be extra weak spot in Q2’21.

— Written by Christopher Vecchio, CFA, Senior Forex Strategist