Dollar, EURUSD, GBPUSD, USDJPY, FOMC and CPI Talking Points:The Market Perspective: USDJPY Bearish Below 137; GBPUSD Bullish Above 1.2300; EURUSD Bull

Dollar, EURUSD, GBPUSD, USDJPY, FOMC and CPI Talking Points:

- The Market Perspective: USDJPY Bearish Below 137; GBPUSD Bullish Above 1.2300; EURUSD Bullish Above 1.0700

- US CPI came in notably softer than was expected by economists, generating the same kind of market response as the November update but still not a substantial rate forecast change

- While EURUSD, GBPUSD and USDJPY have registered varying degrees of technical break against the Greenback, the FOMC decision ahead is still a critical consideration for trend

Recommended by John Kicklighter

Trading Forex News: The Strategy

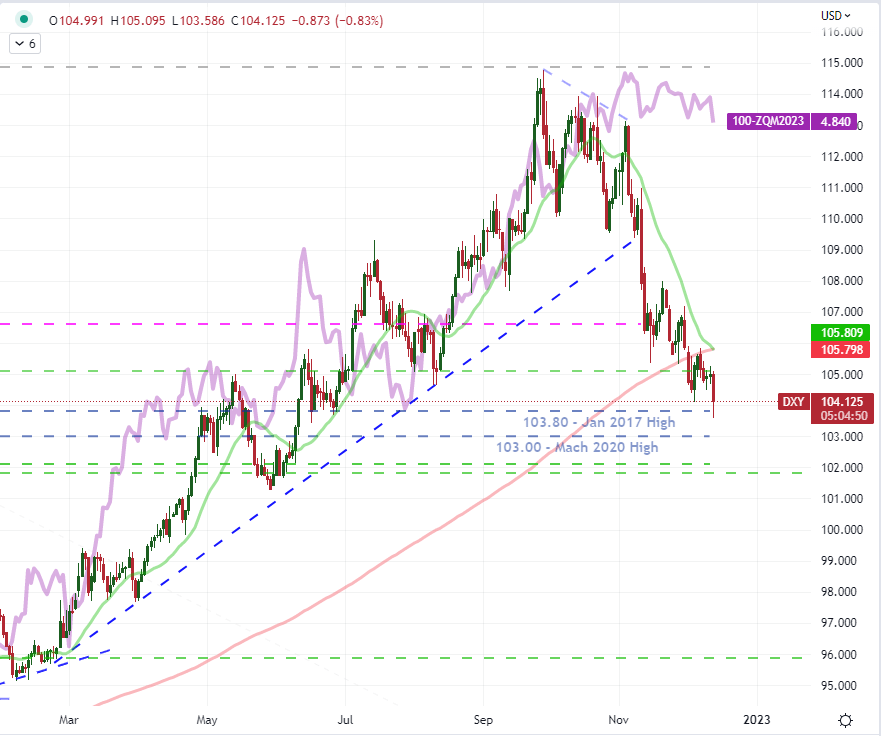

The US consumer price index (CPI) update for November has proven its stripes as a major market mover, echoing the kind of impact that we witnessed back on November 10th following the previous release. With last month’s inflation report, the impact on the Dollar was significant – at least technically. The break below the 2022 trendline support to that point significantly altered the market’s course. That said the market’s forecast for the ‘peak’ Fed Funds rate in 2023 didn’t come down all that much. Nevertheless, the wind was drawn from the Dollar’s bullish sails and a choppy retreat followed from there. With today’s data print, the same initial reaction was present. The DXY Dollar Index showed another sharp decline, but this time the aggregate index wouldn’t experience the same dramatic technical breach. A fresh six month low was tagged, but there weren’t any prominent technical support levels to tear down in the vicinity. What is interesting is that the same reticence was present in translating the cooler inflation reading into a meaningful downgrade in rate forecasts. According to Fed Fund futures, the benchmark rate come June 2023 (around the ‘terminal’ point) will be 4.84 percent, but that isn’t a dramatic turn from the 5.13 percent peak in early November.

Chart of DXY Dollar Index Overlaid with the Implied Fed Funds Rate for June 2023 (Daily)

Chart Created on Tradingview Platform

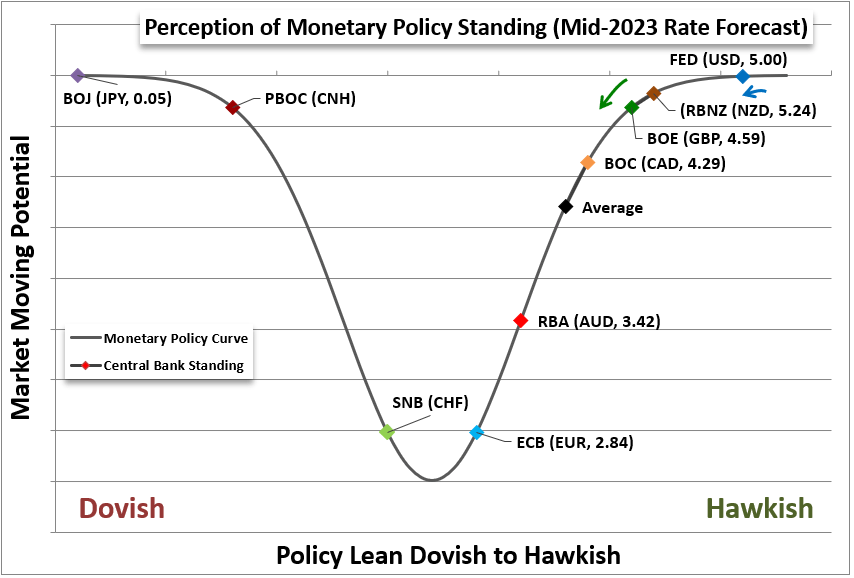

If inflation is cooling more quickly than economists – and from that the markets seem to extrapolating: the Fed – has expected, then why aren’t interest rates dropping more precipitously? This is worth asking as that seems to be a key driver in the Dollar’s bullish run through much this year. The answer may be a few fold. For one, a terminal rate of 4.85 percent is not that much higher than the current range of 3.75-4.00 percent; and it would represent very little tightening at all in 2023 if the Fed goes through with its December 50 basis point hike that the markets are still forecasting. Another consideration for the bleed in influence this theme is experiencing is the relative aspect of interest rates. The Dollar doesn’t respond to the Fed’s rate in a vacuum. The ‘carry’ is a consideration of yield differentials, and other major central banks are also cooling in their own hawkish paths. Perhaps most influential in the short-term, however, is the fact that the FOMC rate decision is due tomorrow at 19:00 GMT. The outlook for terminal rates can dramatically change with what the central bank decides to signal after its announcement.

Chart of Relative Monetary Policy Standings of Major Central Banks

Chart Created by John Kicklighter

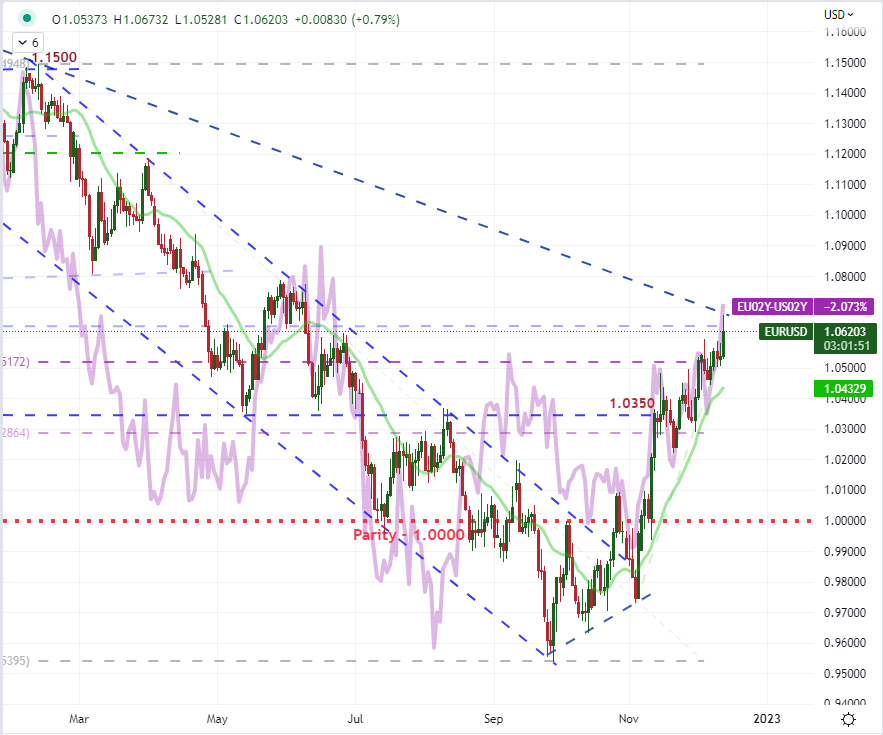

Considering the relative interest rates aspect of the FX market, a particularly interesting pair to watch will be EURUSD. The cross experienced the bullish charge that would be expected from a drop from the Dollar, but here there is technical resistance yet to consider above. While clearing the past week’s highs readily enough, there is still the 38.2% Fib retracement of the January 2021 to September 2022 bear wave and trendline resistance from the past 18 month’s series of lower highs. More interesting though is the fundamental consideration. While the ECB has one of the lower benchmark rates among its peers, there seems more potential for further tightening into 2023. That said, with recession risks remarkably high for Europe and the rest of the world combatting inflation more aggressively, the Eurozone’s policy authority may find it reasonable to tapering its efforts with a lower terminal rate. And given the ECB’s rate decision is on Thursday, that is a option that may be confirmed or denied soon.

| Change in | Longs | Shorts | OI |

| Daily | -18% | 1% | -7% |

| Weekly | -26% | 9% | -7% |

Chart of EURUSD Overlaid with EU – US 2-Year Government Bond Yield Differential (Daily)

Chart Created on Tradingview Platform

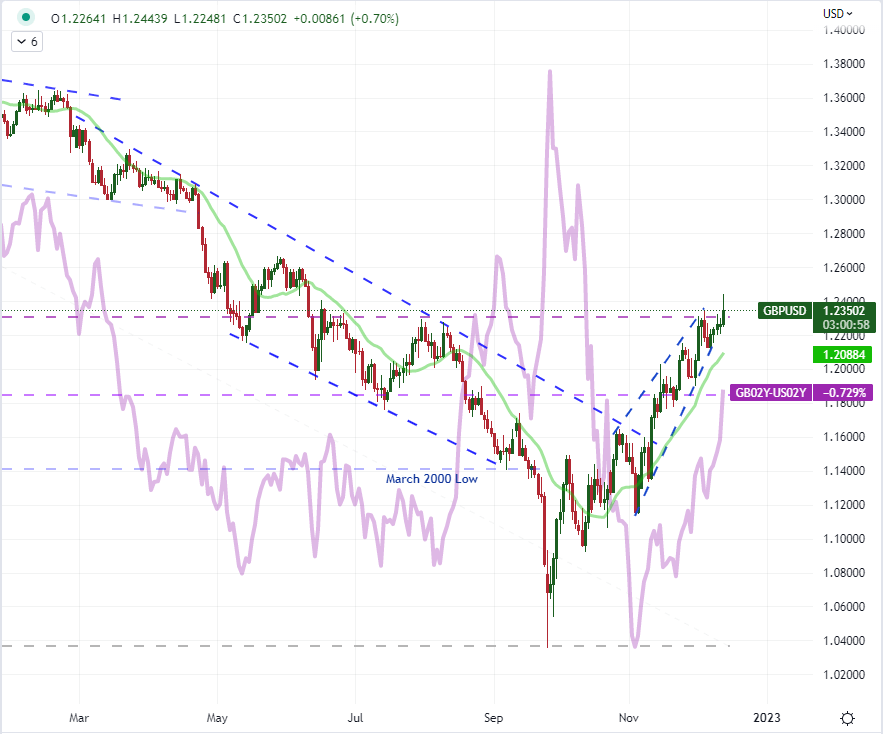

As far as competing central bank decisions go, the Bank of England is also on deck to announce its own monetary policy the day after the Fed. All three central banks are expected to hike 50bps, but the BOE is expected to have further to run before hitting its own terminal in 2023 compared to its US counterpart. Overnight swaps were pricing a June 2023 UK benchmark rate of 4.59 percent, but the rate currently sits at 3.00 percent. That can offer significant carry over potential on GBPUSD’s break above the midpoint of its post-pandemic range around 1.2300. This could make for a volatile back and forth for the ‘Cable’ considering there has been a bullish break today, then we will have the Fed’s decision and Dollar reaction followed by the BOE’s outcome and Sterling retort.

| Change in | Longs | Shorts | OI |

| Daily | -14% | -4% | -8% |

| Weekly | -18% | 5% | -5% |

Chart of GBPUSD Overlaid with UK – US 2-Year Government Bond Yield Differential (Daily)

Chart Created on Tradingview Platform

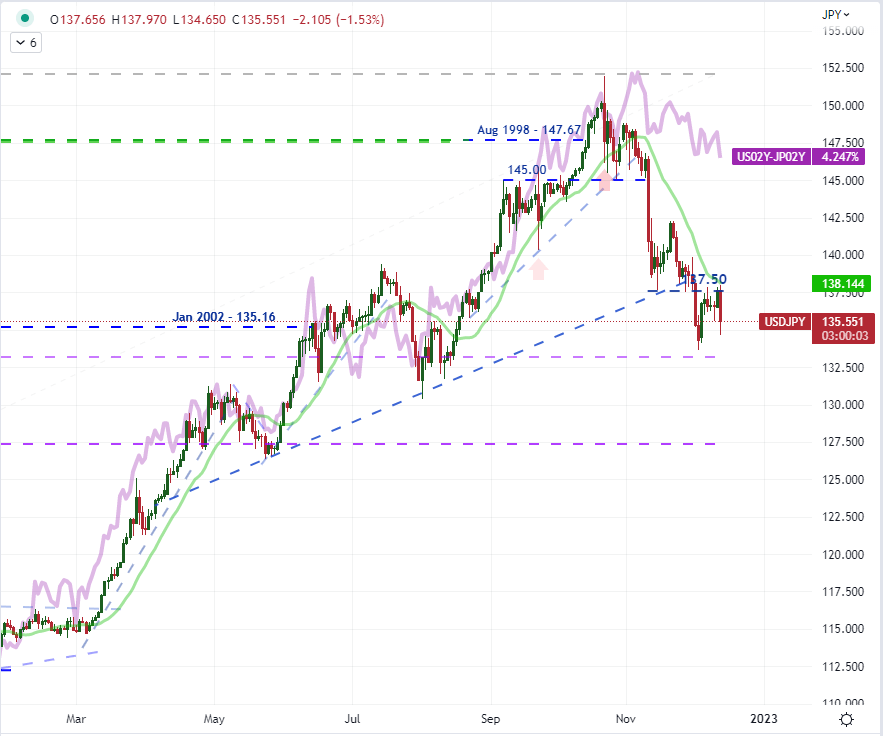

Another productive move among the Dollar-based majors has been USDJPY. This pair held its former support as resistance at 137.50. Technically, that is a productive progression type pattern; but we have yet to take out the next major low which would be 38.2 percent Fib of the 2021-2022 range around 133.20 – still some ways down. The interesting thing here is that relative monetary policy is not as much a factor considering Japan’s central bank is essentially anchored to zero rates. The Fed’s policy decisions therefore carry a lot more of the fundamental weight. That said, there is a ‘risk’ consideration that can complicate the pair’s trajectory. This is a significant carry trade among the Yen crosses, but how much premium is there to be unwound? If Fed forecasts are seen easing (bearish USDJPY) could it also raise risk appetite through assets like indices (bullish USDJPY)?

| Change in | Longs | Shorts | OI |

| Daily | 13% | -15% | -3% |

| Weekly | 6% | -9% | -2% |

Chart of USDJPY Overlaid with UK – US 2-Year Government Bond Yield Differential (Daily)

Chart Created on Tradingview Platform

element inside the

element. This is probably not what you meant to do!Load your application’s JavaScript bundle inside the element instead.

www.dailyfx.com